KR Choksey on Pitti Engineering Q3 FY 24 results

Posts in category Value Pickr

The Anti-Portfolio (01-03-2024)

Yes, you make valid points ![]() Diversification, if done right ofcourse, is meant to cut down on volatility and risk. Indeed, I think I see better options to invest hence the alternate buys, though I might have made a mistake or two.

Diversification, if done right ofcourse, is meant to cut down on volatility and risk. Indeed, I think I see better options to invest hence the alternate buys, though I might have made a mistake or two.

I have only sold off two banks, Ujjivan and RBL, since I wasn’t paying attention while making 36% of folio weight in financials, with 6 companies. So, sectoral rotation happens, they gained lots rapidly, and financial sector can be bit complicated to understand. Now it’s just 12%.

No company or sector should be more than 15% roughly for a balanced folio, they say. Ujjivan and KPI green had exceeded to about 20% weight each.

The major reduced one is KPI green, to about half. Ceinsys, Shilchar and E2E networks have matched the growth, almost double since past 2 months, where the money was deployed.

Sharda motors, Phantom digital, Sanghvi movers, All E tech, Caplin point have all done well. Most others are doing ok too.

I think a small mutual fund kind of folio will also do ok, given bit less expectations. Overall market conditions are also not giving valuation comfort to go big on concentrated buying.

DCX Systems Ltd (01-03-2024)

Successfully raised 500 crores through QIP in January 2024.

209cr out of 500cr going to fund NIART Systems.

Solution developed – Radar and obstacle based deduction system can predict it up to the 1 kilometer plus on the range what is there in the track you can see.

Production from NIART is going to start from next year.

Second 200 crore investment, to invest on JV’s and technology of transfer for Make in India program.

Read full concall insights at:

https://twitter.com/Bornwinner_VJ/status/1760219587038282078

Narayana Hrudayalaya Ltd (01-03-2024)

Whats the potential impact of Supreme Court order on price cap for medical treatments? Narayana mostly does specialist treatments/complex heart surgeries, any impact on business performance or just an overhang?

If not much impact, then this correction in NH share on the back of this development offers good margin of safety, given the company is consistently growing at 20% EPS and valuation (EV/EBITDA) appears reasonable vs peers.

Any thoughts?

PayTM (One 97 Communications Ltd) (01-03-2024)

Financial Intelligence Unit-India (FIU-IND) imposes penalty of Rs 5,49,00,000 on Paytm Payments Bank Ltd with reference to violations of its obligations under PMLA. I don’t know the details. Can anyone educate about seriousness of the issue, if any.

ADF FOOD LTD – FMCG Company for Next Decade (01-03-2024)

The court order and price jump of 17%. What so interesting does market see from this order? can anyone brief

The Anti-Portfolio (01-03-2024)

Hello Vikas sir, been following your thread for some time. Just curious, why so much diversification suddenly 12 to 25? Is it to preserve gains already made or you see the new positions as better opportunities?

Sejal Glass – Turnaround (01-03-2024)

Earnings transcript – Q3 FY24

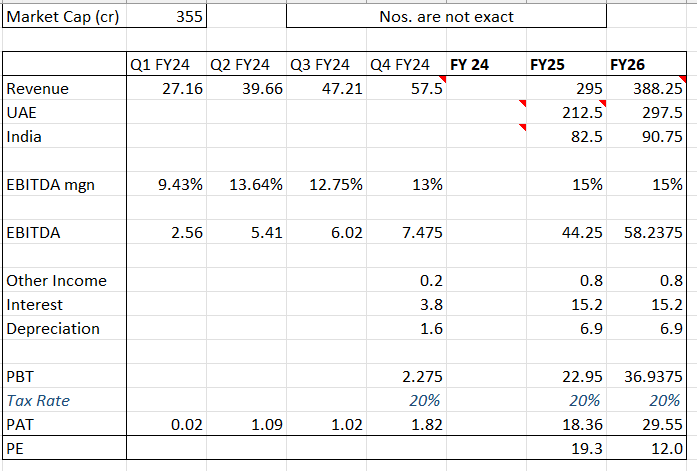

Sejal Glass – Turnaround (01-03-2024)

Positives:-

-

Aarti Industries Promoter – Chandrakant Vallabhaji Gogri has the major stake in the company. He invested to turnaround the company.

-

Expectations of turnaround look good with the majority exposure in Middle East and India – both high growth economies.

UAE – UAE seven states at Dubai, Sharjah, Abu Dhabi, Ajman, Ras AlKhaimah; then we have GCC Qatar, Bahrain, Oman; and certain 1 or 2 customers in Pakistan; then some 3 customers in Africa right now we have.

India -We are mostly right now 75% to 80% in the western India and particularly Mumbai, Pune, and a little part of that Vapi, Daman, Valsad, and Surat. -

Strong Player in its segment.

-

Outlook as per the company –

“I will just give you the forward projections for the Q4. Consolidated, we will be around Rs. 55 crores to Rs. 60 crores for the Q4. And for financial year FY25, India operations will be around Rs. 80 crores to Rs. 85 crores and Dubai will be around Rs. 200 crores to Rs. 225 crores. “

It is confident of increasing revenue well beyond FY25 at a similar pace. (can expect 40% to be conservative.)

Risks:-

- Cash flow issues due to working capital increases, bad creditors and debt servicing.

- Inability to crack the middle east market on which the company is counting on.