Hi, Did you sell Emkay taps? If not, can you please share your thesis?

Posts in category Value Pickr

Page industries (28-02-2024)

It’s going through PE derating. Since earnings have collapsed due to weak consumer demand. Hence we see the high PE and price may go further down as it starts derating more. Hopefully demand kicks in soon. They’ve launched athleisure, etc and i see a lot of reviews (mostly positive) on their products even when they are priced very high (aka more buyers)

Disclaimer: Invested during my learning stage.

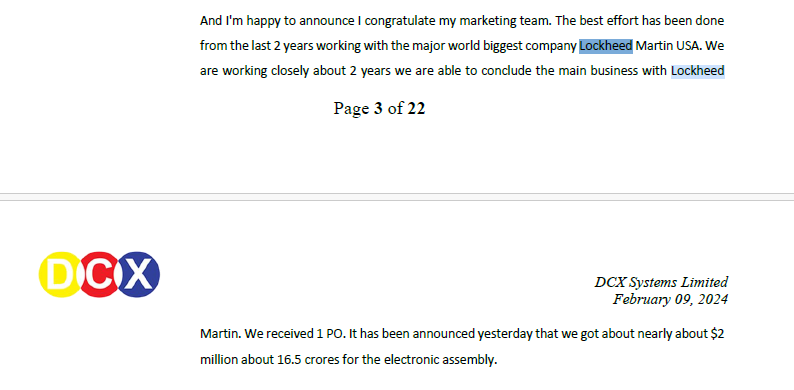

DCX Systems Ltd (28-02-2024)

The attached extract from DCX System transcript Q3 2024, the management said that they had received an order for US$ 2Million. See the attached screenshot.

Piramal Enterprises Ltd (28-02-2024)

Q3-FY 24 Con call notes and some other notes

Although a major portion of the notes is from the Q3 call, I have added some more references to understand things better, for example, Deferred Tax asset or Andheri land.

General

-

Added 93 Branches in the last 12 months

-

Productivity of branches in 1 to 2-year vintage is 2X 6-12 months vintage

-

Target Openex to Asset ratio of 3.5 to 4.0%

-

Today, its Opex to asset ratio is 5.6 (5.8 last quarter)

-

Wholesale AUM (excluding non-yielding assets, SR, Land Receivable assets, DHFL Book) 11,197 cr. Aiming to bring this down to zero in next few quarters

-

Wholesale SR reduced due to cash realisation of 909 cr since Q1-24

-

Shriram’s life (14.9% stake) and general insurance (13.3% stake) business is on the book at 1709 cr

-

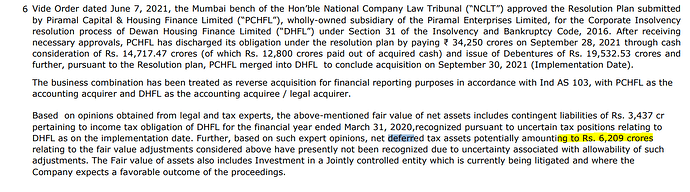

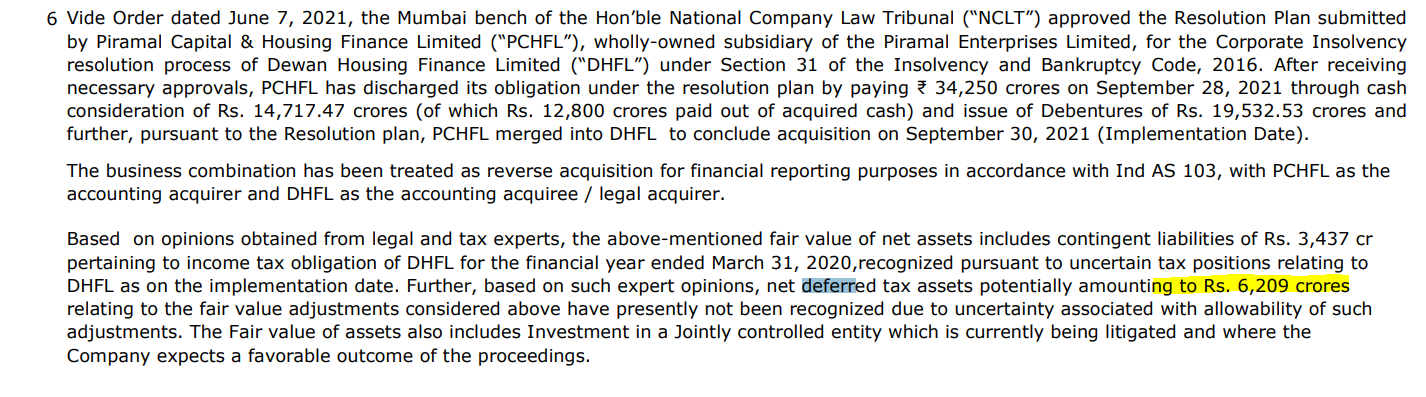

Deferred Tax Asset timeline in Q4 with tax authority. We should hear in the Q4 result. As per this link it was 6209 cr in June 2022.

-

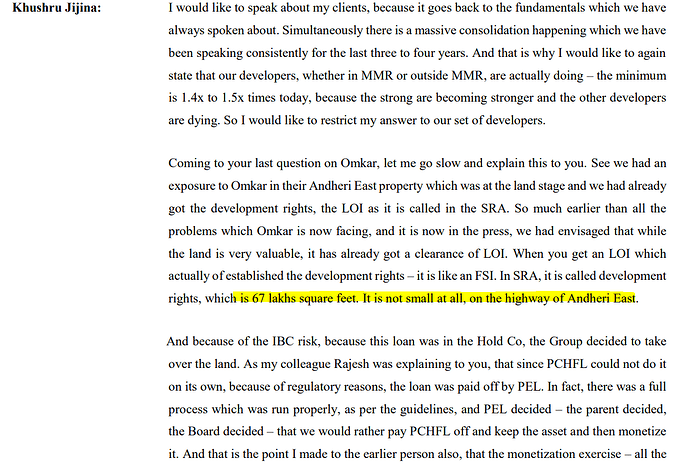

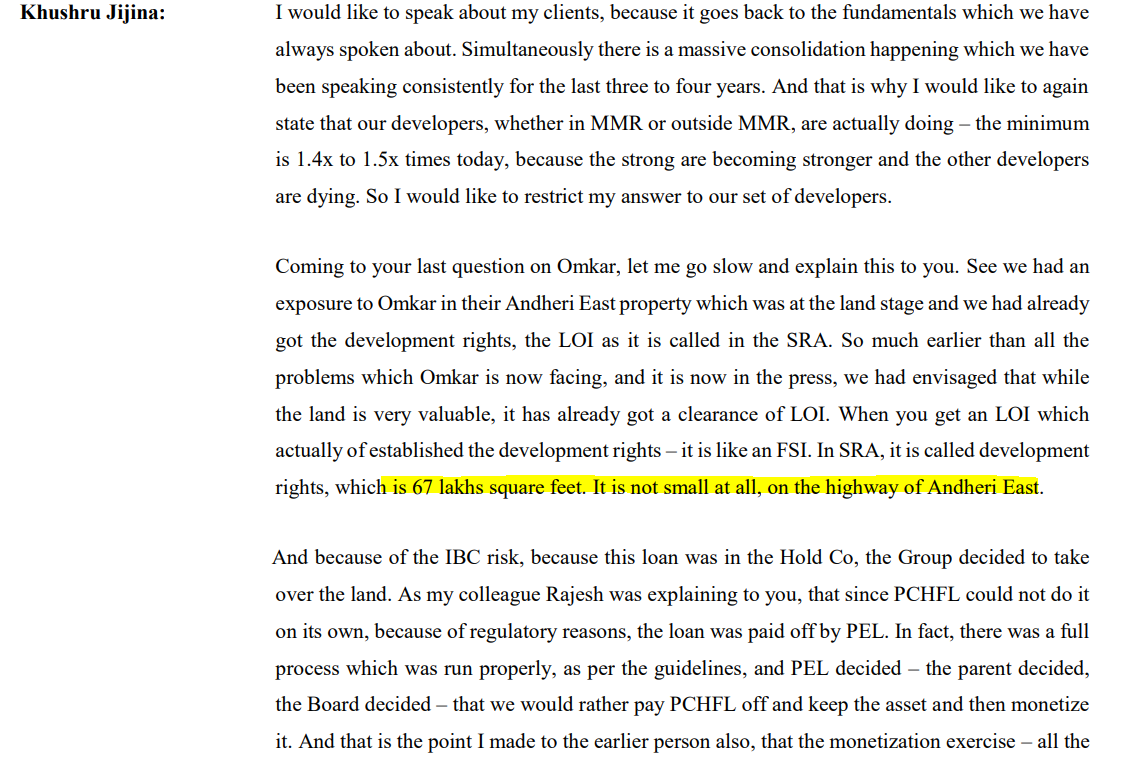

Andheri East Land- 67 lakh square feet on Andheri East Highway. Work in progress for monetisation. It is around 1300 cr on the book as ‘Investment property’. Below snapshot from old con call for reference.

Road to 3% ROA (by FY28 as per Investor Day PPT)

- There things that need to happen

- OpenX need to come down from the current level (5.6%) to around 3%

- Yield plus fees need to go up

- A moderation in the cost of borrowing.

If these things happen, ROA will improve even if credit costs remain in the same range (1.5%)

AIF

- It was formed in 2020 and comprised 35 loans. Of this, 22 loans exited and 13 remaining. Proceeds of this 22 have been used to bring down AIF

- All 13 loans are residential real estate projects. One project is backed by an undeveloped or early-stage land parcel

- earlier, it was 8000 cr. Now it is 3500 cr

- Confident of recovering pretty much everything.

- As per CNBC interview, most of it shall be recovered in the next 6/8 quarter (major shall be recovered in the first 5/6 quarter).

Unsecured Loan

- Total is 10,000 cr. But less than Rs 50,000 loan book is 600 cr( there is a serious strain in Rs 50k and below loan book overall)

- This part of the book is a flywheel kind of business. PEL is originating a bunch of customers, but only a small part of it will be going to become large ticket customers in future

Fintech business

- Done at 14/15% IRR. 90% of this business is protected through FLDG(First Loss Default Guarantee), which means PEL is not taking any credit costs.

- Essentially, it is a 14% IRR business with no opex and no credit cost, so hence, it is profitable.

- Currently, it is done through partnership, but looking forward to doing it internally

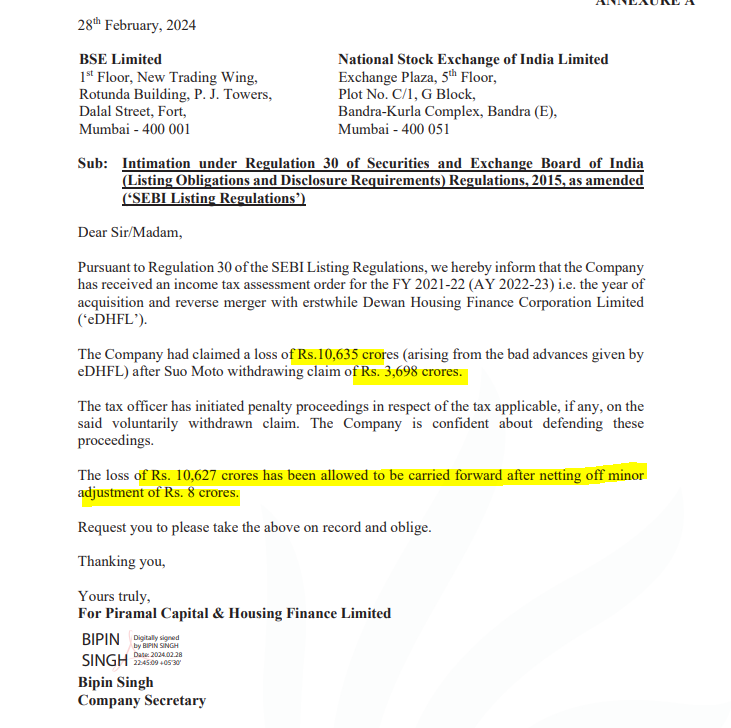

PEL Just reported that they are allowed to carry forward losses of Rs 10627 cr. Not sure it this is same as Deferred Tax asset referred above.

Note: Invested

Ranvir’s Portfolio (28-02-2024)

Shalby Ltd –

Q3 FY 24 results and concall highlights –

Revenues – 220 vs 207 cr, up 6 pc

EBITDA – 47 vs 38 cr, up 23 pc ( margins @ 21.2 vs 18.5 pc )

PAT – 19 vs 15.5 cr, up 25 pc

Standalone Revenues @ 200 cr, EBITDA @ 47 cr, PAT @ 25 cr ( all grew at very healthy rates )

Net Cash ( minus debt ) on books @ 61 cr

Company’s portfolio / businesses –

10 Multi Speciality hospitals across West, Central and North India. A leader in Joint replacement in the represented market

60 OPD domestic clinics + 16 international OPD clinics ( mainly in Africa )

06 Franchisee hospitals

US based Knee and Hip implants manufacturing facility

Total bed capacity @ 2150 + beds, present across 13 cities in India

Q3 operational matrices –

ARPOB @ 37.3 vs 36.3 k

Occupancy rate @ 47 vs 43 pc

Surgery count @ 6746 vs 6782

Hospitals business segmental revenue percentages –

Anthroplasty – 43 pc

Critical care – 9 pc

Cariac – 9 pc

Onco – 10 pc

Ortho – 10 pc

Neuro – 5 pc

Nephro – 4 pc

Others – 11 pc

Hospitals business payor mix –

Self pay – 35 pc

Insurance – 41 pc

Govt – 24 pc

Implants business sales mix –

India – 57 pc

US – 43 pc

Implants business financials –

Revenues @ 21 cr, up 46 pc

EBITDA @ 20 lakh

No. of constructs sold @ 2630 ( 70 : 30 – Knee : Hip )

Company invested 102 cr to acquire 87 pc stake in Sanar International hospital Gurugram. Its current bed capacity is 130, expandable to 180. This hospital caters mostly to international clients ( 68 pc of its revenues )

Still have the vision to grow the implants business to 800 cr / yr kind of sales in 5 yrs

Sanar International is likely to do a 30-35 cr / Qtr kind of topline for next yr. Also, the ARPOBs here are much higher – in the range of 1 lakh. However, current occupancies are low @ around 25 pc. Currently making EBITDA losses

Aiming to do high single digit EBITDA margins from the implants business by end of next yr

Mumbai – is a Greenfield project ( Hospital ) that’s lined up by the company. May take 3-4 yrs to go live

Aiming for 20-22 pc growth in EBITDA for next FY without accounting for the new facilities and inorganic opportunities like the Sanar hospital

Seeing pickup in no of surgeries in Jan, Feb 24. Confident of doing better business in Q4 vs Q3

Disc: holding, biased, not SEBI registered

Rategain – Fast Growing SaaS Leader (28-02-2024)

Looks like the partnership with FLYR is quite a big deal. Although the announcement was made yesterday by FLYR, media has covered extensively today and looks like it is likely to benefit 40% of the hoteliers who struggle to manage their inventory though multiple channels. This is also a good opportunity for rategain to promote their new navigator platform and hopefully this will become a industry standard in the years to come. The biggest plus I see in near term is that the distribution segment which has been a laggard over last two quarters will start growing faster with this partnership. Posting the link for everyone which has these details in plain English. Rategain has also made this disclosure today through an exchange filing.

Rain Industries – An oversold de-leveraging play (28-02-2024)

Always the price difference is passed on to customers with one or two quarters lag effect., that is what is happening now., when the prices goes up from here which should since it has bottomed out., they will reap the benefits of inventory…they easily maintain 14% plus margin always… check last 10 years data

Dreamfolks services limited( DFS) (28-02-2024)

Motilal_Oswal_DreamFolks_Initiating_Coverage_Note.pdf (4.4 MB)

![]() Motilal Oswal Coverage On Dreamfolks Services Limited

Motilal Oswal Coverage On Dreamfolks Services Limited

Page industries (28-02-2024)

I think worth a serious look. Apparel growth will bounce back and page has commanded a premium valuation for a reason. Look out 2/3yrs