seems the ongoing promoter’s family settlement issue is a concern on the future of the company. Stock is trading low for this reason?

Posts in category Value Pickr

Yasho Industries (25-02-2024)

Hey @divygupta

So Yes you are correct that any kind of RM Increase will result in the increase in the revenue as the it’s a pass Through

The Downward Revision is on the basis of Current Prices of RM if you see management has said that they are not committing to the statement that Price will go back to mean of RM and hence the statement that → weather the price inching up is likely to be a fire or Fizzle out

Hence in short downward revision is Excluding the increasing RM Prices

→ my bad should have framed sentence better ![]()

Disclaimer as Above

Action construction equipment ltd (25-02-2024)

According to Manish Mathur, the CEO of Action Construction Equipment (ACE), a new plant for heavy machines is set to be commissioned. This development will significantly enhance their capacity, increasing it 3-4 times compared to the current scenario(A new plant for heavy machines will soon be commissioned which will increase our capacity 3-4 times. – Top Construction and Infrastructure Magazine).

Here are the key points from the article:

- Current Market Scenario:

- ACE is the largest mobile crane manufacturer in India and holds the distinction of being the world’s largest manufacturer of pick-n-carry cranes.

- The cranes market in India is witnessing robust growth, with a 25-30% YoY rate.

- The economy’s momentum and the government’s focus on infrastructure and manufacturing are expected to sustain this growth at a 15-20% CAGR.

- Infrastructure development and the demand for higher capacities and innovative construction equipment are driving the industry forward.

- Technology Trends:

- Technology plays a pivotal role in providing economically and environmentally viable solutions.

- ACE integrates Telematics into its equipment, allowing remote monitoring and supervision of functional parameters.

- The company constantly adapts global technologies to Indian working conditions.

- Future Outlook:

- ACE aims to expand its range of crawler and truck cranes.

- The upcoming plant will significantly boost their production capacity, positioning them for continued success in the heavy machinery sector(A new plant for heavy machines will soon be commissioned which will increase our capacity 3-4 times. – Top Construction and Infrastructure Magazine).

Escorts Limited – Playing for Margin Expansion (25-02-2024)

According to a recent article on Construction Times, the Indian mobile crane industry is poised for growth. Here are the key points:

-

Current Market Scenario:

- The Indian government’s ambitious “Vision 2030” initiative aims to transform India into a $5 trillion economy by 2025 and a $10 trillion economy by 2030.

- Infrastructure development projects, including roads, railways, seaports, airports, urban transport, and inland waterways, have created a strong demand for mobile cranes in India.

- Pick-n-carry cranes, which constitute over 90% of the total mobile crane industry in India, are widely used for material handling operations.

-

Growth Trends:

- In the current financial year (FY24), the Indian mobile crane industry recorded an impressive 26% year-on-year (YoY) growth.

- The pick-n-carry cranes segment specifically saw a remarkable 45% YoY growth.

- Escorts Kubota Limited, a market leader in safe cranes, introduced the TRX 30 crane with a 30-ton capacity for mega infrastructure projects.

- The TRX 30 features joystick-controlled craning, a hydraulically operated winch with safety brakes, and efficient driveline components.

- Telematics integration allows real-time monitoring of crane performance and location.

-

Future Outlook:

- Despite a potential drop in the first quarter of FY25 due to general elections, the mobile crane industry is expected to grow at a CAGR of 4-5% until FY28.

- Government policies supporting infrastructure development will continue to drive demand for mobile cranes in India ¹.

(1) The Indian mobile crane industry will continue to grow in future… The Indian mobile crane industry will continue to grow in future. – Top Construction and Infrastructure Magazine.

(2) Construction Times – Top Construction and Infrastructure Magazine. https://constructiontimes.co.in/.

Is China investible? (25-02-2024)

If India is a consensus long trade today, China is a consensus short trade. Betting on any consensus trade is a losing strategy in the long run. As a trader & investor, I like to sit on the sidelines watching patiently as consensus trades start getting questioned and momentum starts reversing! That’s the best time to get in. But of course this is easier said than done.

Smallcap momentum portfolio (25-02-2024)

Update for entry on 26th Feb 2024

Based on ranking

- BSE

- MEDANTA

- MRPL

- SUZLON

- NBCC

- HUDCO

- TATAINVEST

- BSOFT

- SWANENERGY

- MCX

- CHALET

- WELCORP

- OLECTRA

- IRCON

- SOBHA

- KALYANKJIL

- COCHINSHIP

- ITI

- IRB

- MOTILALOFS

Based on A → Z for easy tracking

- BSE

- BSOFT

- CHALET

- COCHINSHIP

- HUDCO

- IRB*

- IRCON

- ITI

- KALYANKJIL

- MCX

- MEDANTA

- MOTILALOFS*

- MRPL

- NBCC

- OLECTRA*

- SOBHA

- SUZLON

- SWANENERGY

- TATAINVEST*

- WELCORP

Entry:

OLECTRA and TATAINVEST make an entry.

IRB and MOTILALOFS cannot enter as there is not vacancy.

Exit:

KAYNES and NLCINDIA exit.

PCBL and SJVN stay within the top 25 and hence remain.

Yasho Industries (25-02-2024)

Hi @Ashar_Mann

From whatever I understood abt Yasho, is that the pricing of the items would be generally a pass through. if that is the case and the RM costs is inching upwards, then why would the revenue from the new plants decline, shouldn’t it increase? Did the mgmt say anything about why the downward revision to the revenue potential

Disclosure: not invested

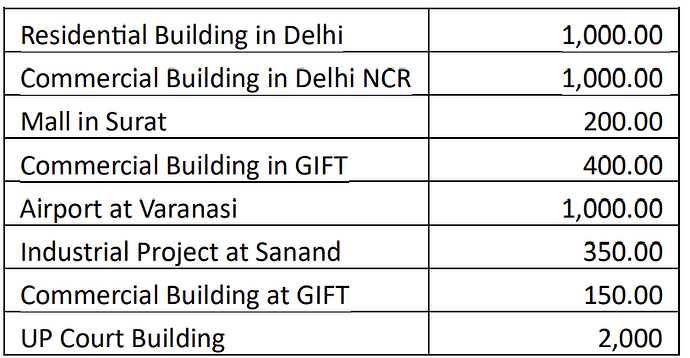

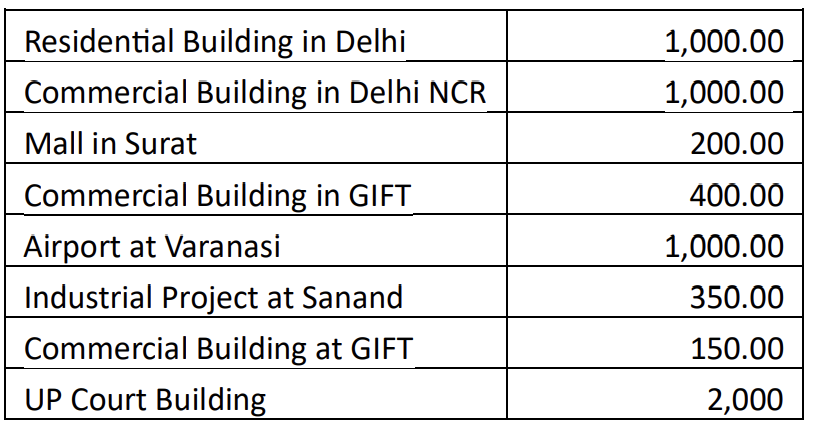

PSP Projects – Construction Company (25-02-2024)

Q3 FY24 Concall notes

-

Project Highlights:

- Completed 7 projects in Q3FY24, including Adani Realty’s residential and industrial warehousing for Reliance Jamnagar.

- Awarded 2 major projects: Kalamkhush Campus at Gandhi Ashram and Gujarat Biotechnology Research Centre.

-

Order Inflow and Bookings:

- Q3FY24 order inflow at Rs.1,060 crore; total Rs.1,995 crore post recent letter of acceptance.

- Outstanding order book at Rs.4,443 crore (51% government projects) as of 9MFY24.

-

Project Development Updates:

- Legal proceedings for Surat Diamond Bourse underway.

- UP Projects revenue: Rs.250 crore (Q3), Rs.1,429 crore (9MFY24).

- SMC administrative building progressing; Q3 revenue Rs.49 crore, 9MFY24 total revenue Rs.171 crore.

-

Recognition and Awards:

- Awarded “Fastest Growing Construction Company in India” at 21st Construction World Global Awards, 2023.

-

Financial Outlook:

- Company bids for large projects in new states, displaying confidence in effective nationwide execution.

-

Strategic Vision:

- Gradual move up value chain, targeting higher-ticket projects.

- Bid book spans Madhya Pradesh, Odisha, Delhi, UP.

- Aligns with 2024 budget’s Rs.11 lakh crore infrastructure allocation (3.4% of GDP).

- Commitment to India’s growth, positive development, confident in solid economic fundamentals.

-

Financial Performance (Q3FY24 vs Q3FY23):

- Revenue from Operations: Rs.697 crore (40% YoY increase).

- EBITDA: Rs.71 crore (16% YoY increase).

- EBITDA Margin: 10.25% (down from 12.39%).

- Net Profit: Rs.33 crore (8% YoY decrease).

- PAT Margin: 4.63% (down from 7.01%).

-

Expense Analysis:

- Other Expenses: Increased from Rs.5.2 crore (Q2) to Rs.8.51 crore (Q3), includes ECL provision on Trade receivables.

- Employee Costs: Rose from Rs.29.56 crore (Q2) to Rs.33.75 crore (Q3) due to appraisals.

- Finance Cost: Increased from Rs.12 crore (Q2) to Rs.15 crore (Q3) due to short-term borrowings and bill discounting.

-

Capital Expenditure and Balance Sheet:

- Capex during 9 months: Rs.142 crore, with Rs.74 crore for precast facilities.

- Long-term Borrowings: Rs.75 crore (including short-term maturities of Rs.50 crore).

- Short-term Borrowings: Rs.403 crore (excluding short-term maturities of Rs.50 crore).

- Gross Block of Assets: Rs.543 crore, Net Block Rs.325 crore (additions in Q3: Rs.34 crore).

- Net Unbilled Revenue: Rs.409 crore.

-

Working Capital and Credit Facilities:

- Working Capital Days: Debtor – 63, Creditor – 60, Inventory – 35, Total – 38.

- Utilized Credit Facilities: Rs.1,030 crore; Rs.467 crore available for utilization.

-

Fixed Deposits:

- Total Fixed Deposits: Rs.257 crore; Lien-free deposits: Rs.47 crore; FDs under lien: Rs.210 crore.

Business Growth:

- Order Book and Revenue:

- Current year’s target: Rs.3,000 crores order book.

- Next year’s projection: Rs.3,000 crores revenue, Rs.3,500 crores order book.

- Profit Margin:

- Targeted margin: 11% to 12%.

- Commitment to maintaining margins through tender criteria.

Promoter Shareholding:

- Reduced from 74% to 66% over 2-3 years.

- Reductions due to personal requirement.

- Commitment to maintaining current level (66.2%) for the next year.

- Reductions driven by personal needs.

- Approximately 10 employees beyond the promoter family earn over Rs.50 lakhs.

Revenue Growth and Projections:

- Nine-Month Performance:

- Achieved 15% revenue growth in the last nine months.

- FY24 Revenue Projection:

- Projected revenue between Rs.2,500 and Rs.2,600 crores for FY24.

Margin Outlook:

- Margin Range Adjustment:

- Margin range revised to 11-12% due to uncertainties in EPC projects.

- Fourth Quarter Margin Expectation:

- Anticipation of returning to the original margin levels after the completion of UP projects.

- Previous quarter’s lower EBITDA margin of 10.3% attributed to UP project expenses.

Equity Raising and Financial Strategy:

- Equity Enabling Resolution:

- Enabling resolution for potential growth capital needs.

- Not an urgent requirement, contingent on order book expansion and bank guarantees.

- Bank Guarantee Requirements:

- Anticipated bank guarantees for Rs.1,500 to Rs.1,600 crores order book.

- Potential need for Rs.350 to Rs.400 crores in bank guarantees, requiring a minimum margin of Rs.300 crores.

Project Updates and L1 Orders:

- L1 Order Clarification:

- L1 order of Rs.928 crores includes Science City and Gati Shakti, Vadodara projects.

- Exclusion of the dairy plant, Rajkot project, due to cancellation related to budget constraints.

- Dairy project expected to be re-tendered in March or April.

Bid Pipeline and Project Status:

- Delhi Railway Station Project:

- Status: Tender of Rs.4,800 crores has been cancelled.

- Overall Bid Pipeline:

- Total Bid Book: Stands at Rs.6,000 crores.

- Major Projects in Bid Pipeline:

Financial Strategy and Debt Management:

- Surat Diamond Bourse (SDB) Claim:

- Claimed amount: Rs.539 crores

- Section 9 proceedings initiated to protect funds.

- Outcome expected by end of February.

- Potential settlement of Rs.300 to Rs.400 crores.

- Equity Raising Consideration:

- Decision on equity raising contingent on SDB outcome.

- QIP option under consideration if needed.

- Monitoring the situation for the next 1-1.5 months.

- Debt Situation:

- Current combined short-term and long-term debt: Rs.478 crores.

- Rise in debt attributed to SDB and UP projects’ receivables.

- Anticipating Rs.300 crores from SDB by March to normalize debt levels.

- QIP Enablement:

- QIP enabled to address potential working capital needs.

- Ensures smoothness in working capital and reduces interest costs.

- Unbilled Revenue and CAPEX:

- Net unbilled revenue: Rs.409 crores.

- Nine months CAPEX: Rs.142 crores.

- Additional CAPEX of 2-3% anticipated for new projects in the fourth quarter.

- Upcoming Projects:

- Initiating 2-3 large projects, including Gatishakti (Rs.630 crores) and Dharoi and Sabarmati Riverfront (Rs.400+ crores).

- Anticipating minimal CAPEX for Dharoi and Sabarmati Riverfront initially.

Precast Revenue and Margins:

-

Nine-Month Precast Revenue:

- No specific figure available due to orders being from various clients.

- Anticipated overall revenue from Precast by year-end: Over Rs.180 crores.

-

Margins Expectation:

- Initial stages focused on market penetration.

- Targeting margins of 11% to 12% in the long run.

- Potential for higher margins (3% to 4%) when technology is universally accepted.

-

Current EBITDA Status:

- Presently EBITDA-positive but not at the targeted margin levels.

-

Current Utilization and Capacity:

- Present utilization: 40% to 50%.

- Total plant capacity: 30 lakh square feet per year.

-

Potential Margins with Increased Utilization:

- At 80% utilization, expected margins of 11% to 12%.

Smallcap momentum portfolio (25-02-2024)

(post deleted by author)

Ganesh Benzoplast – Cash rich chemical storage/tank king (25-02-2024)

With recent Funds mobilization by the company by FPIs, Promoters and Non Promoters, the company is poised to grow with capacity increase. Currently their Liquid Gas Storage Tanks are operating at 100% capacity.