Past performance is no guarantee for future years. The main issue is with no order bidding in the pipeline or no big order wins in recent history. Also they have ventured in to EPC recently to bid orders from railways. Otherwise road construction is not a niche business with so many competition(especially NCC with huge order backlog). I’m just saying there is a perfect explanation why market have rated it low. Especially with no order bidding pipeline with elections looming one can revisit this counter at leisure. Upside is limited and downside seems protected (due to lot of MF holdings) . I’m offloading at my own pace.

Posts in category Value Pickr

JEENA SIKHO- seems shady, one off? (24-02-2024)

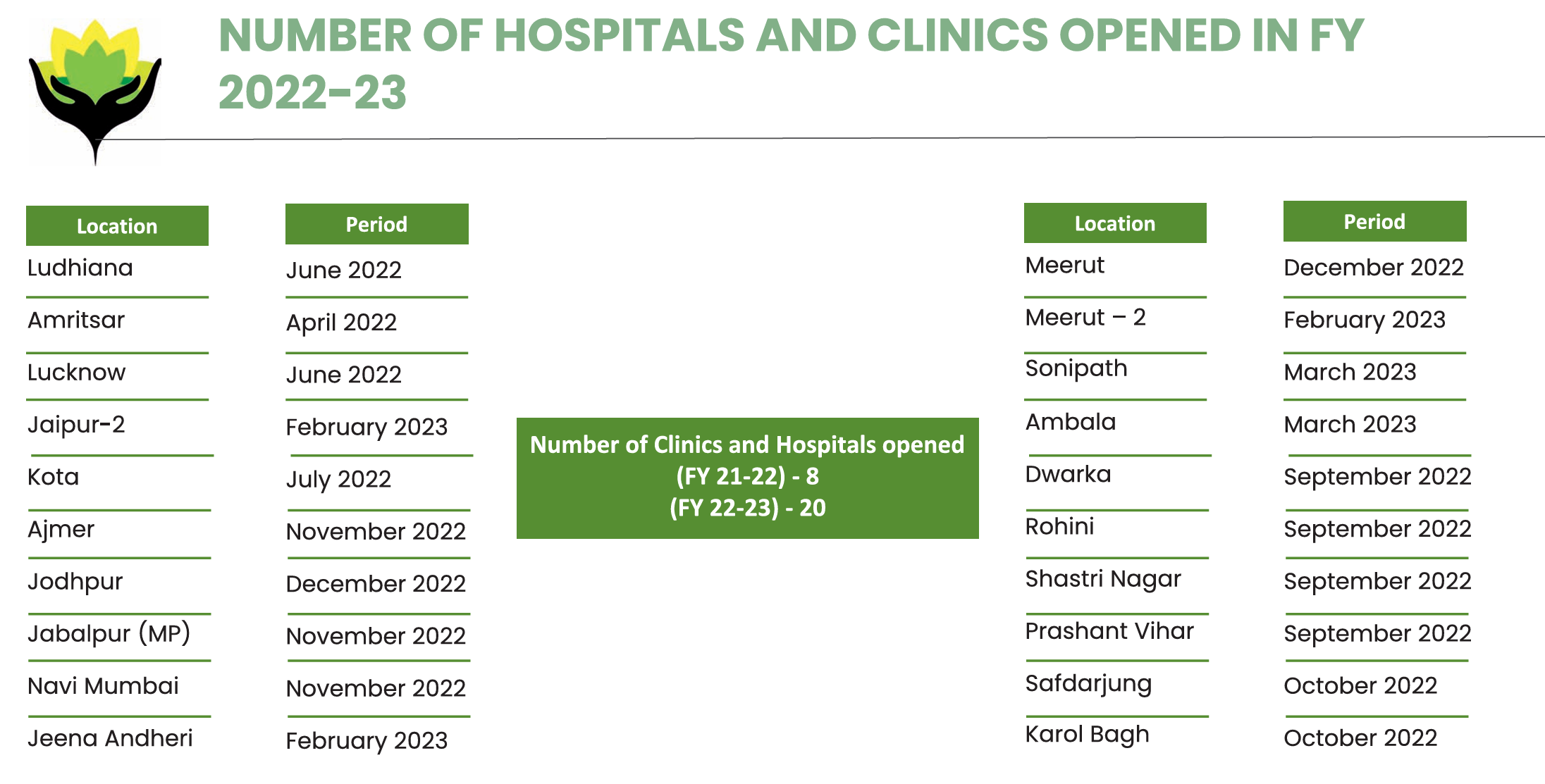

25 Clinics/hosps added in the CFY till date…thats approx an increase of 320 rooms

12 Clinics/105 rooms in H2… still a month plus to go!

Rush of updates on empanelment with Health Ins Firms (a few major ones), probably this expands the possibility of increase in footfall (being cashless transactions).

Intellect Design Arena (24-02-2024)

In case you have not heard why Teminos woes Nilesh Shah is referring here it is. This is the best thing that could have happened to Intellect the last few months.

This report will report create doubts in the minds of perspective customer which are being targeted by Intellect as well. Plus Teminos has a large user base in Europe, which is focus area for Intellect.

Key beneficiaries of this will be for large deal. However due to size, it takes long time to seal a deal. Looking at the trouble of Teminos, I think IDA shall report better deal win in the next 3/4 quarters IMO.

https://hindenburgresearch.com/temenos/

Note: Invested

Geekay Wires Ltd (24-02-2024)

I dont really understand this well, even at AGM management didnt explain this very well. But I guess their volumes might be higher in recent times, and with correction in commodity costs, overall revenues look muted. But this is just a guess.

Zen technologies – A micro cap in the defense space! (24-02-2024)

Sales not important it is important to see weather they have IP in ADS or not

Tips Industries Limited – Ready to RACE ahead! (24-02-2024)

I feel the growth would be high, whether it would be 30% or 5-10% here or there I don’t know.

The biggest low hanging fruit currently is proper monetization of shorts, Tips has already pulled its content from Instagram and I think the new deal would happen at a substantial amount whenever that happens.

And in the longer run, people will have to pay for convenience of streaming music like they are paying for now for say food delivery etc and that would trickle down to music labels.

I have shared some thoughts on monetization of convenience here if you are interested-

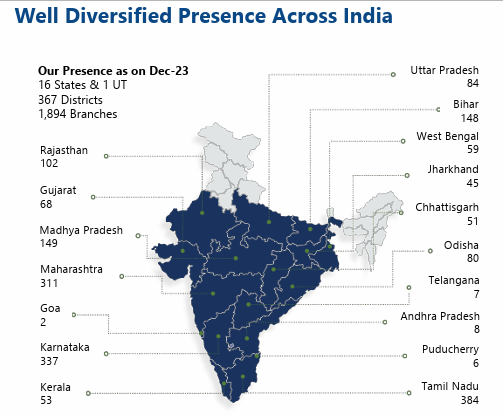

CreditAccess Grameen: Traditional MFI model, efficiently operating at scale (24-02-2024)

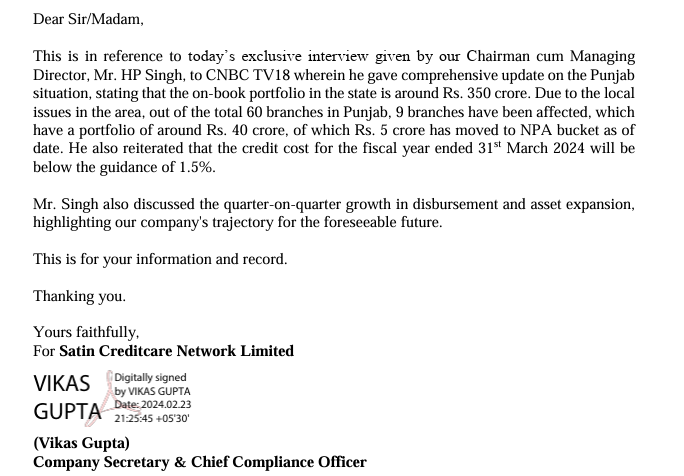

Satin is struggling in Punjab.

Any other state where there is trouble as such from Microfinance point of view.

And if Credit Access has exposure to that state ?

If not then Market Leader shall command better valuations

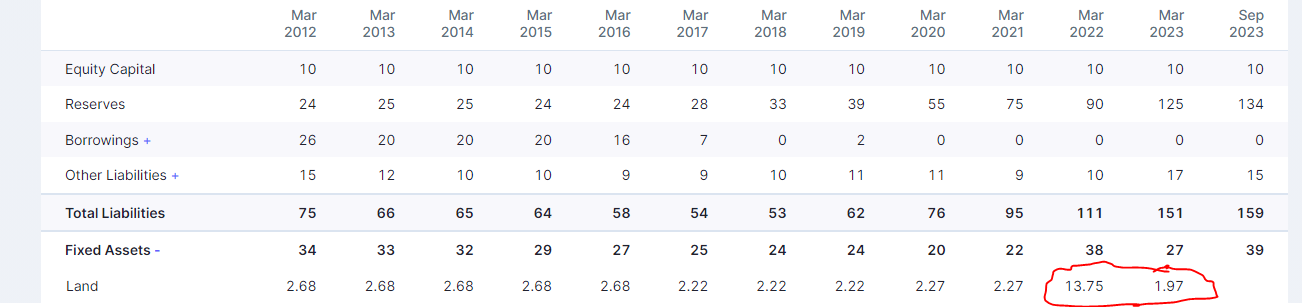

Diamines and Chemicals Ltd – Navigating for a long-term growth (24-02-2024)

What happened here where did the land go ?

MTAR Technologies – A wager on innovation meeting economies of scale (24-02-2024)

Really thought provoking questions + write up by @ankit_george above. Going through the earnings call for Q3, I’d like to take a shot at answering all the Qs asked above:

- FY24 revenue guidance is INR 610 crore, significantly lower than the earlier estimates. Definitely shakes confidence in the estimation capabilities of the management.

- Couldn’t deduce whether it was a revenue recognition issue, but the management highlighted stabilization issues at Bloom Energy which disrupted delivery schedule. They believe the worst is over and things should become smooth from Q4.

- 500+ hot boxes delivered to Santa Cruz in Q3. 664 hot boxes estimated to be shipped in Q4.

- Expecting orders of 300 units from Fluence Energy in FY25, which could increase to 1K units in FY26 and 3K units in FY27.

- 44 electrolyzers shipped in Q3. 60 electrolyzers expected to be shipped in Q4. No comment by management on transition to high volume mass manufacturing. No comment on volumes over the next few years – however, management sees electrolyzers as a BIG OPPORTUNITY.

- No exact commentary on this, but given a lower revenue guidance I don’t think they’ll achieve the INR 150 crore domestic sales #

- Expecting order book to close at INR 1,400 crore for FY24.

I covered the Q3 earnings call HIGHLIGHTS + LOWLIGHTS in this article if anyone wants a deeper dive.

Again, amazing thought activity @ankit_george !

Disclosure: Not invested. Tracking QoQ performance.

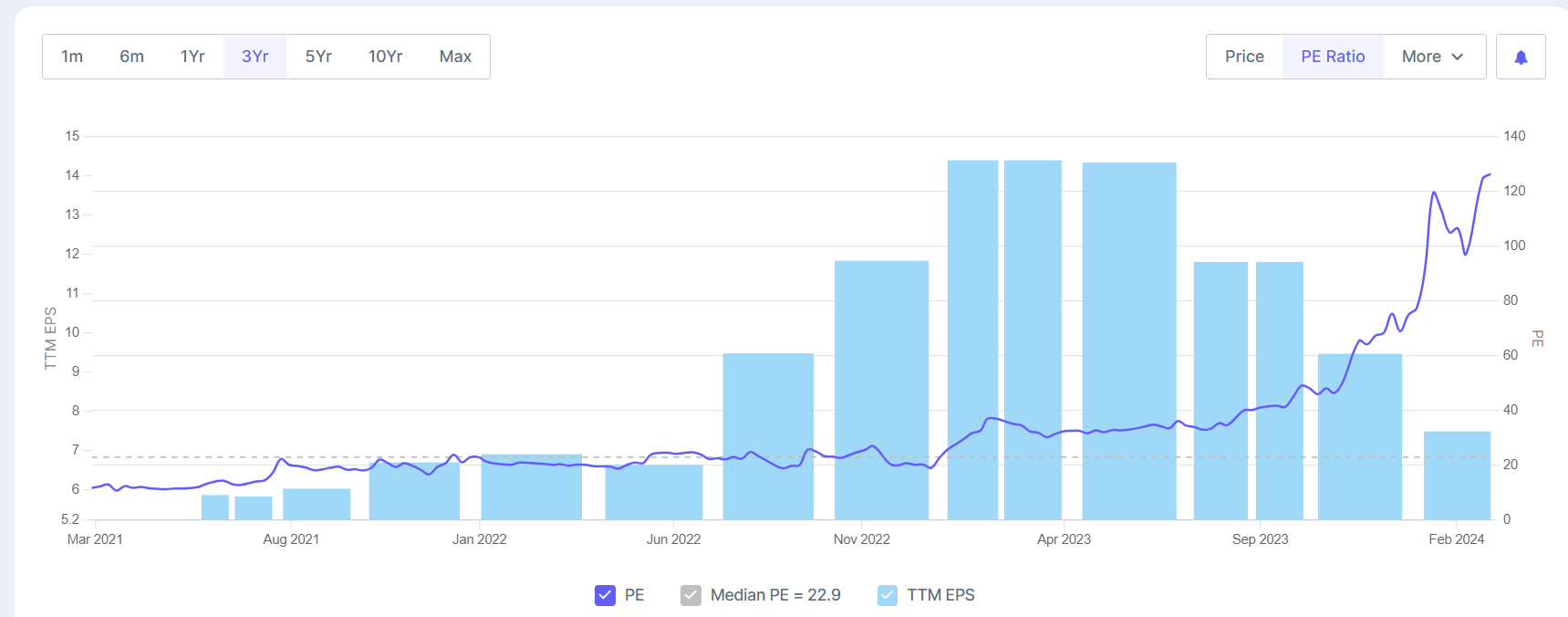

Praveg Ltd: Play on Indian Tourism Industry! (24-02-2024)

Refer all company announcement on allotment of equity shares after Dec 2023 (Q3) and try to estimate EPS on dilution basis for Q4 and FY2024.

Expecting correction in share prices as it should align with mean PE ratio