Grim commentary. Mean reversion as something is fundamentally broken.

China’s Real Estate Collapse Has Only Just Begun, Argues Brian McCarthy

Grim commentary. Mean reversion as something is fundamentally broken.

China’s Real Estate Collapse Has Only Just Begun, Argues Brian McCarthy

A friend of mine who is HNI, invested 2 Cr with Marcellus in 2021. RG – 1 Cr, CCP – 50 L and LCP – 50 L. He wanted sell 50% of the portfolio because of recent underperformance. Attaching the note I sent to him.

Marcellus – Query.docx (22.5 KB)

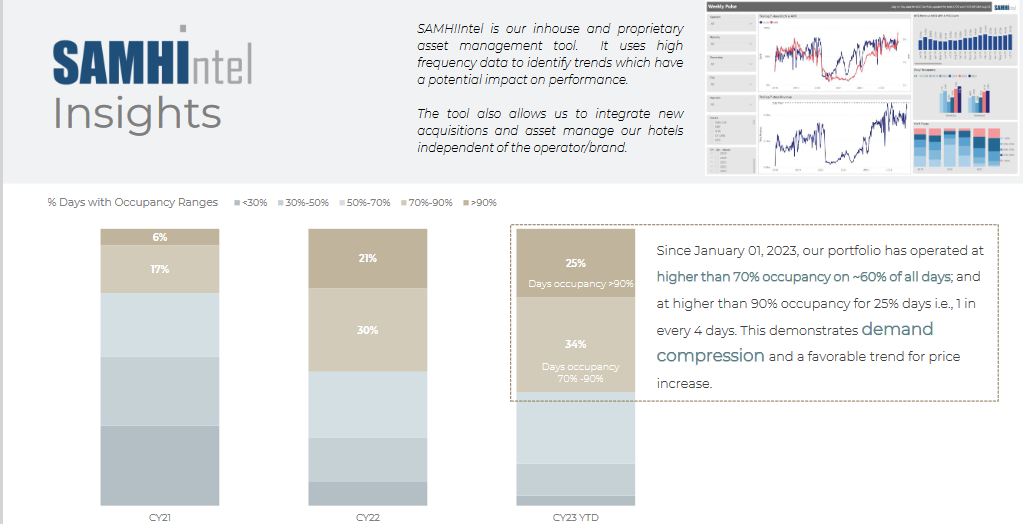

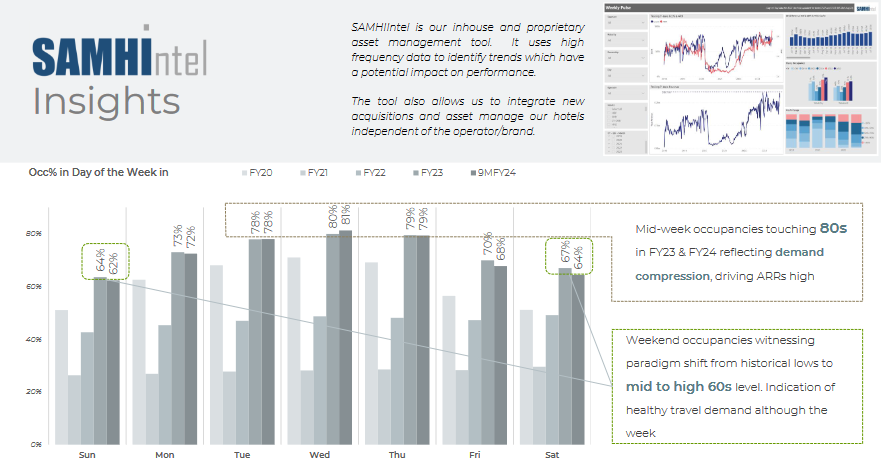

Interesting data shared by management in quarterly investor presentation.

This on from Q2 FY24 shares insights on % days with occupancy range.

This is from Q3 FY24 gives info on occupancy % on different day of the week.

More like fairly priced. Growth is in mid single digits and no major triggers for re-rating.

224 CR as per Screener

Unlikely, unless they make some kind of leap to capture market share.

Disc: Holding a small position, might add more if valuations get attractive

GSK Pharma –

Q3 FY 24 concall highlights –

Revenues – 805 vs 802 cr

EBITDA – 218 vs 229 cr ( margins @ 27 vs 28 pc )

PAT – 46 vs 165 cr ( due an exceptional provision of 163 cr wherein company laid off some employees as a part of its restructuring efforts, hence had to pay for the VRS. Company has laid off 12 pc of its MRs )

Company has a large presence in vaccines and general medicine segments

New focus areas in India – Adult Vaccines

(starting with Shingrix – a vaccine for adults to prevent Shingles) and new Respiratory products

Q3 of LY was a very good Qtr. Hence, the growth this yr looks tepid because of the base effect. Vaccines portfolio grew 10 pc in Q3. Shingrix continues to ramp up well

Company commands 24 pc mkt share in Paediatric vaccines in India in the private – self pay segment

Key brands like – Calpol, T-Bact ( antibacterial ointment ) grew strongly in Q3. Company had to cope up with a minus 8 pc impact on its sales because of the NLEM. Still managed to keep the topline flat

Vaccines form 18 pc of company’s total India business. EBITDA margins are lower in Vaccines as these are imported and the company effectively trades them

Despite severe pricing pressures from NLEM regulations in last 5-6 yrs, company has still improved its EBITDA margins by around 700 BPS over that period

Company is aggressively growing its new and innovative respiratory assets – Trelegy and Nucala ( both for asthma ). These brands are growing at a very healthy rate. Trelegy is big brand for GSK in the international mkts clocking sales > 16000 cr / yr

Company intends to launch new and innovative Onco, Respiratory products in India in next 2-3 yrs. Most of these are big brands in developed Mkts

The layoff of MRs in q3 should aid margins in Q4. MR count now stands at around 2500-2600

Nucala is a monoclonal antibody. Has been showing extremely positive results. Company is adding an avg of 1000 patients/yr. It’s an expensive treatment. Costs aprox 70k / month

Trelegy is also growing very strongly. Treatment with Trelegy also costs > 50k / month

Shingrix is doing a sale of 7-8 k injections / month. It was launched in May last year. Each injection costs > Rs 9k

MR productivity at around 85-90 lakh/ MR

Trials are on for GSK’s global asset Bepirovirsen before it can be launched in India. It’s used to treat chronic Hep-B. It can potentially be a really large molecule

Company’s 40 pc portfolio is under NLEM

Calpol and its brand extensions continues to be No.1 prescribed brand in India

Company has 03 major Oncology brands in the international Mkts. Will introduce them in India at some point in time ( maybe 2-3 yrs )

Disc: hold a small position, biased, not SEBI registered

KSE sell Ice -creams

Hi. Which MF has bought? Any confirmed source of this news?

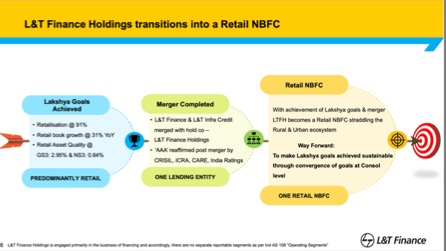

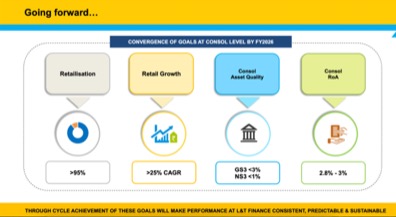

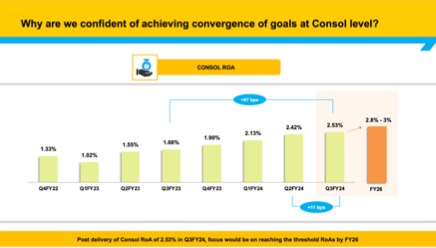

L&T FH delivered another great set of numbers this quarter, whilst Lakshya 2026 goals have been met 2 years in advance.

Consol ROA is now at 2.53% vs 1.66% Q3 last year, consol ROE is now 11.35%

Consol PAT is up 41% YOY at ~640 Cr for Q3

Merger is completed with L&T AMC sold off and L&T Infra and L&T Finance now merged into this company

Retail book grew at 31% YOY and is now > 90% of the business. I think this is now largely a retail NBFC and with only a small part of the wholesale book to sell post bringing it down so sharply, do not understand with these growth/ROA metrics why is it still valued at under 2 PB when the likes of Chola, FiveStar are trading much higher (>4 PB).

Even in pre covid times (Jan 2020) when things were terrible for NBFCs after 2018 and this was not a retail NBFC this has traded at 2x book. Whilst in great times in 2018 with the credit cycle, valuations were much higher than that as well when it traded at 5x book

Management has addressed doubts on personal loans/contracting NIMs well in the concall and have mentioned not much impact, but this remains to be seen in future results

CEO transition handled quite well and old/new CEO were both on the last concall with lots of positivity. Current CEO Mr Sudipta Roy is ex ICICI/Citi/Deutsche bank and ex CEO Mr Dubhashi superannuates from the company in April’24

Below snapshots from Q3 investor presentation sum up last years progress quite well

Disclosure : I am invested in self and family accounts for the last 1 year odd and am biased. Have further buy transactions in family accounts in last 90 days. I am not a SEBI registered advisor and this is not investment advice.

There is no court order.

This is just CCI order reaffirming international sugar approval. (Since AGI had filed objection 9

Case is tentatively listed for hearing on 23 Feb in supreme court.

With passage of time, HNG’s furnaces have become inefficient and dangerous without any repairs and maintenance.

If one or two years further pass on this IBC , HNG would have died slow death.

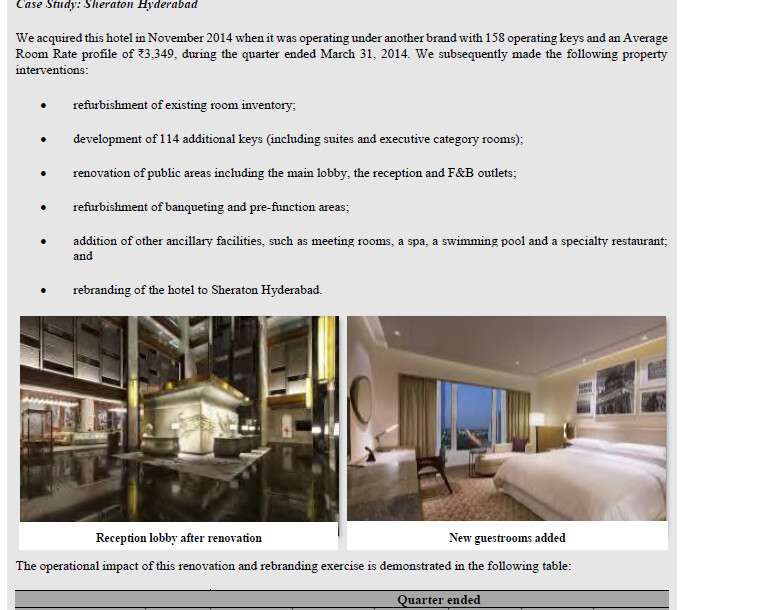

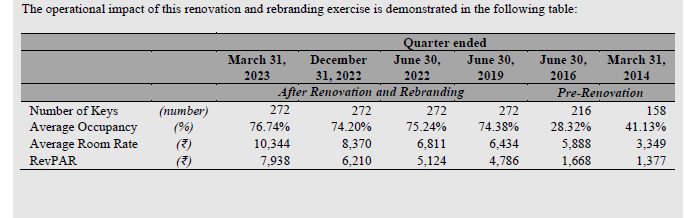

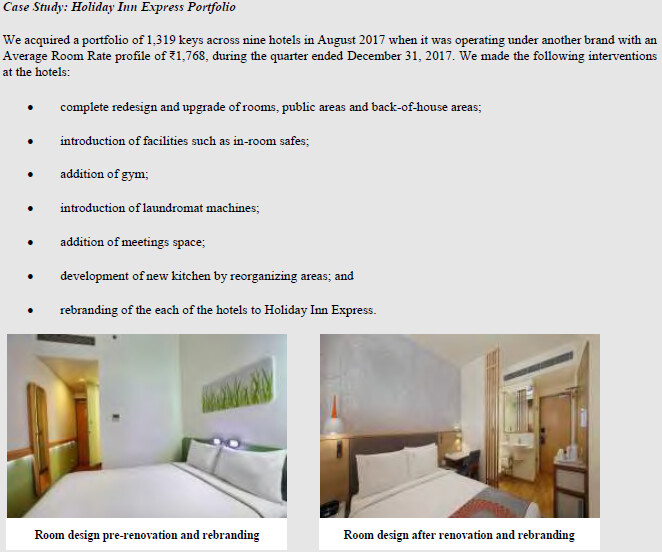

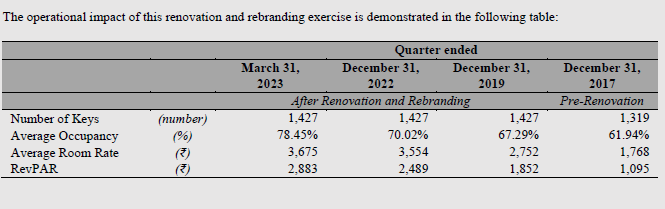

Interesting case study in RHP about their track record in acquisition.

Above record seems interesting. It would be nice if management gives account of acquisition which were not successful.

If we compare with industry, ARR and occupancy level were really low pre-acquisition and they seems to have managed to increase both.