5fd389b8-6854-44f8-9e3d-fa5702b31e94.pdf (621.7 KB)

New order…

5fd389b8-6854-44f8-9e3d-fa5702b31e94.pdf (621.7 KB)

New order…

Dear @Amit2saxena This is a good writeup.

I believe Matrimony is a very undervalued bet. For 1100cr, one gets 350cr of cash and a business that generates 50cr of annual PAT. In the last one year, the Company added 20cr of revenue but that unfortunately went into provisioning for the Google payments. In the next one year, the next 20cr should help grow to 65-70cr PAT. This makes it valued at <20x PE for a true consumer company with very high ROE. Should competitive intensity reduce the Company is likely to see a lot of leverage flow from the 200cr of advertising expense (that does not add to sales), which could result in disproportionate returns.

Cheers

Safe to assume, I and everyone I know may have a vested interest in everything I post about. Nothing is a recommendation ![]()

Sold few KNR construction and SIPing PVR.

KNR the order bidding pipeline for road construction is expected to revive after two quarters, Also its venturing into EPC projects which is capital intense. Quite surprised to see no thread for KNR and the existing one has been locked indefinitely which makes it super hard to follow.

PVRInox fixated on the narrative. Near monopoly in multiplex. Only a few movie blockbusters away from another good quarter. The recent spat of big hero Hindi movies doing good business augurs well .The boycott Bollywood cries have subsided. Also at a decent entry point. will evaluate on a quarter to quarter basis.

Forgot to factor in revenue and profitability of epc segment

While the points you make are true, I don’t think they are holding back the discovery of the company. I also don’t think the market misunderstands the nature of the company’s business/ operations. I make this statement basis following:

1. The company, in its earlier avatar of Kilpest, was able to get US FDA approval for RT PCR kits, and was promptly recognized and rewarded by market.

2. The company has been meeting analysts and other investment firms/community from time to time.

3. Though the company doesn’t do concalls, the presentation all through has been giving enough information to decipher COVID and non-COVID revenue.

4. The market has also realized the one-time nature of COVID revenue, with the company being valued at 2-5 PE basis peak profitability in the past.

5. Above all, in a bull market, when people are searching for reasonable opportunities, a company of such nature (by financial numbers) is sure to pop up in screeners and is unlikely to escape attention.

The one-time rerating (from 300-400 odd levels to 850 odd levels) for the company is done and dusted, IMO.

Further performance trajectory would mainly depend on the following:

1. Utilisation/Misutilisation of the cash reserves.

2. Earnings growth.

3. Ability to tap into the opportunities thrown open by UK subsidiary.

Valuation Note 3 [21st February 2024]

Current Valuations can only be judged from the vantage points of How the future turns out.

If 1 year Down the line PAT growth is 30% or higher, and there is visibility for Robust Orders even beyond that, Current Valuations are approx ~ 20X P/E

If 1 year Down the line PAT Growth is 30% or higher BUT the order book starts to dwindle, the stock will be punished. Fast & Hard.

Therefore, What is cheap or expensive is based on our understanding of the future.

The question then becomes: How confident are we that Order book will remain Robust?

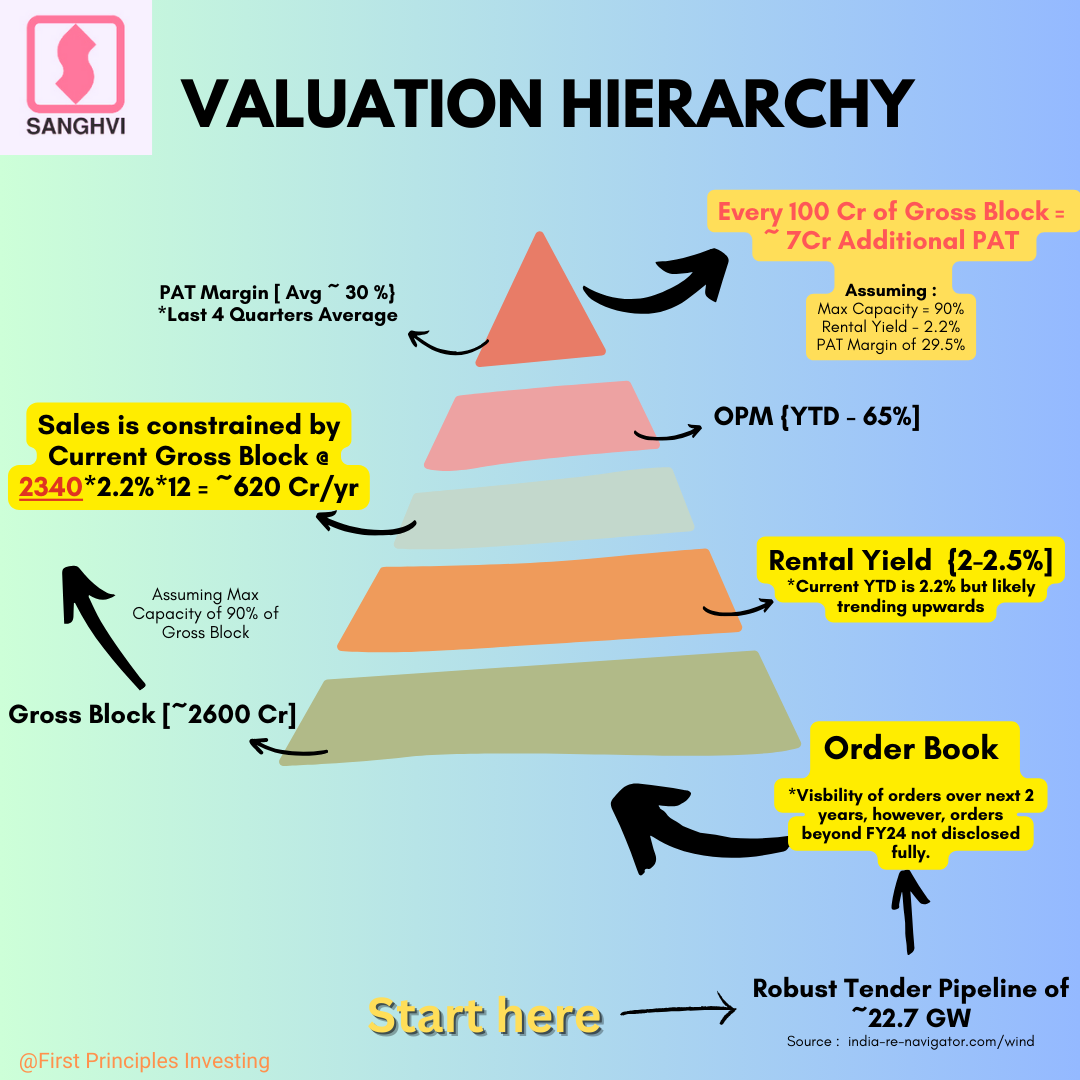

Firstly, Tender Pipeline for Wind/Hybrid projects & Awarded Capacity give us confidence that this most likely will be the case (Thanks to @rcinvestor999 for updating us on the same)

Secondly, the Management Commentary is bullish (Disclaimer: Management has a strong incentive to paint a rosy picture, so this is not always the most reliable Signal)

Given a 75% Market Share in Wind Energy Sector, plus a high % of Cranes with 100 MT and above capacity (most suited for higher Hub heights), Sanghvi is well placed to milk this Wind Energy boom.

The second question then becomes: If Demand is well taken care of for the foreseeable future, what can limit Sanghvi’s Growth?

My 2 cents : Its own capacity.

Even after spending ~400 Cr this year, Sanghvi has an Soft upper limit of ~154 Cr per Quarter of Sales or 615 Cr per year.

In FY24, Its already hitting that number (Q4FY24 Sales should be ~155 Cr),

If despite a huge capex of 400 Cr in FY24, Sales have a limit of ~154 per Quarter, where’s the 30% Growth going to come from?

- Rental Yields will need to increase

- More investments in buying Cranes

| Rental Yield (%) | 2.3% | 2.5% |

|---|---|---|

| Sales (Cr) | 646 | 702 |

**Assuming Current Gross Block of 2600 with 90% Max utilisation. Sales = 0.9*Gross Block Rental Yield

If Rental yield increases to 2.5%, Sanghvi can eke out as much as ~700 Cr. Nearly 80 cr more.

So, the same Crane Capacity can accommodate at least up to ~11% Sales Growth without spending more on increasing crane capacity (i.e – buying more cranes)

But there’s the kicker, an increase in Rental Yields to 2.5% goes straight to the bottom line.

This 80 Cr, on a post-tax (25%) basis, has the potential to increase PAT from 180 to 240 Cr.

A 30% PAT Growth.

Although the probability of Sanghvi being able to hit a Rental yield of ~2.5% should be viewed with a healthy Skepticism, it is NOT entirely outside the realm of possibility.

Either way, in my view there are 3 Growth Drivers :

Personally, given my understanding as of today I am least worried about point 1. The Demand for once does not seem to be a problem. Capacity might be.

My Guesstimate is that a combination of Rental Yields and Capex is likely to drive growth.

An announcement of a sizeable capex program in the near future should be an important trigger because it would be akin to “putting your money where your mouth is”

We’ve already got a sense of what Rental Yields can do for Sales and PAT, here’s a diagram that can help us understand the impact of Capacity on Sales and its limitations.

In short, Every 100 Cr spent on Capex can increase PAT by ~ 7 Cr. This means if the co’ spends another 400 Cr, PAT Growth is likely to be just about 15% (28/180 Cr)

Hardly inspiring.

This is why I believe, Rental Yields, Capex and Op. Lev Combined would be needed to hit a 30% or higher PAT growth, a minimum benchmark for us to conclude with confidence the Stock is Currently cheap or reasonably priced.

Look forward to hearing your views. Please Feel Free to point out any errors.

Adtiya buying stake in tourism finance …Any views ???

Sharing my notes on KRBL

Negatives

Positives

Facts

Points to ponder

Growth will command investing in inventory, which means profits will be plowed back in inventory. Generally speaking, inventory is the easiest place to bury all frauds. If investor trust the inventory numbers that company claims, then business produces good ROCE on incremental investments.

Concall notes available on screener