Thank you. It gave me conviction. Signed up and will buy shares on Monday.

Posts in category Value Pickr

Pitti Engineering Limited: Is it on an inflection point? (09-02-2024)

Q3FY24 results are as expected.

The accompanying Investor Presentation gives a rosy picture. Q4 FY24 numbers could be as per company’s predictions.

Trent — A value unlocking story from the house of TATA (09-02-2024)

It’s not just the size. It’s the quality and execution chops they have delivered.

It should keep on getting re-rated, on every result.

52 week highs and all time highs strategy (09-02-2024)

Hi Hitesh sir,

Many thanks for spreading knowledge. After your last assessment about NBCC, the stock has been on a non-stop rally reaching to the highs of 168 and now is cooling down. It seems that the stock has run quite a lot and has also reached a 6 year high backed by good volumes however as the results will be coming on 13 Feb. Do you think that the earnings will be able to justify this sharp rally or this was due to the craze built on the PSU theme. Please can you share your current assessment of the stock, whether it has still some steam left or is it time to be cautious? Many thanks in advance.

For the last 6 years, Vedanta Resources has been repaying its loans by taking more loans. It can’t do that anymore, so it wants to demerge. A fun read (09-02-2024)

The dividends have taken out the risk of investing in this stock provided the investments were made when they were selling for 80-100 when they were trying to take the company private. Do you think Hindustan Zinc is a safer bet than Vedanta?

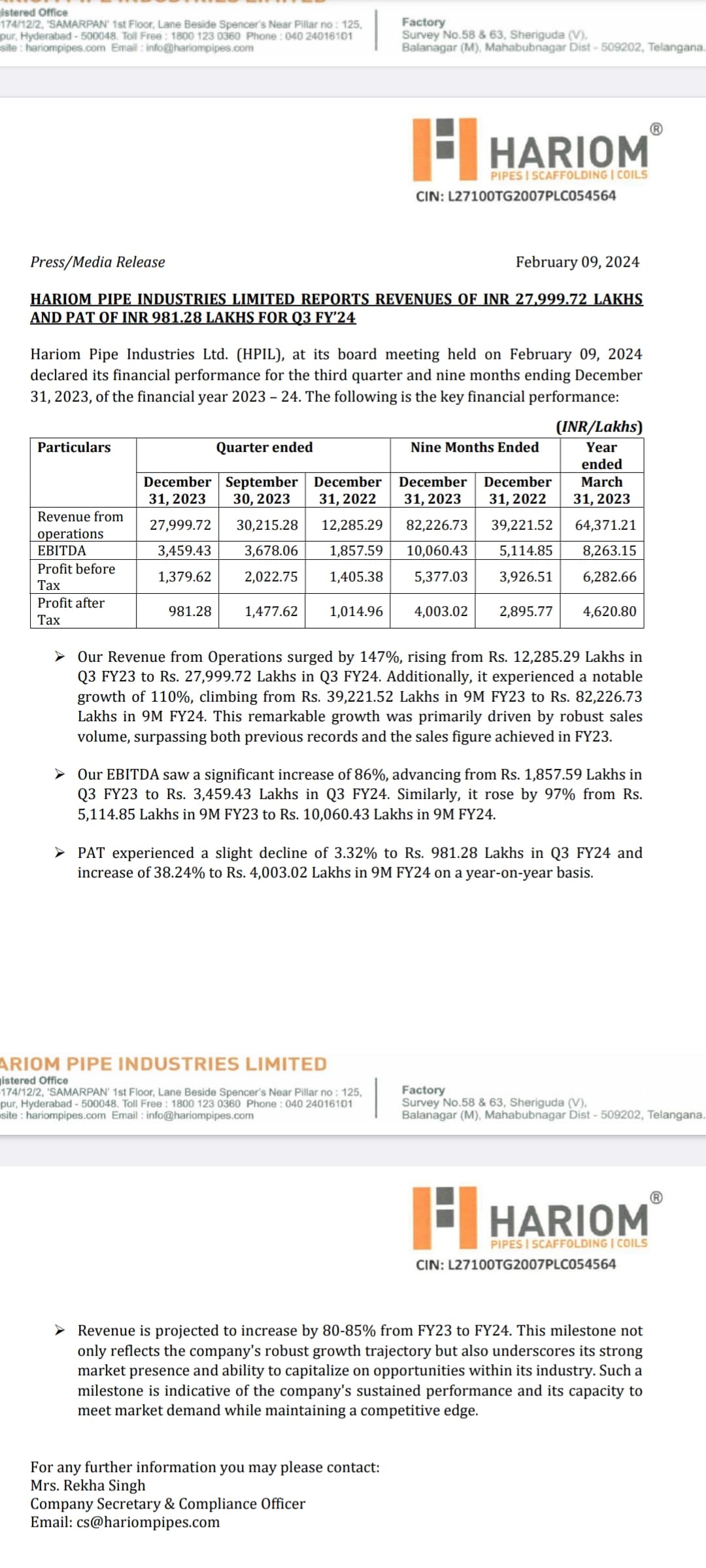

Hariom Pipes Ltd: A Capex Play! (09-02-2024)

Hariom Pipe Results update:

-Revenue growth of 146% n QoQ fall

-EBITDA growth of 86% n QoQ fall

-PAT fallen QoQ n YoY led by dep & int exp

-Lack of disclosure in press release, what I believe industry weak demand + South flood had led the impact on operations

-Management released a simple press release compared to the last one which was detailed…

-Poor results were already backed in price as suggested by fall of 20% from ATH

-Behind the words guidance is given of 80-85% growth in FY24 over FY23

Q4E Sales: 360-375 cr

Q4E PAT: 15-17 cr

-Warrants money allotted can take care of Q4 WC requirements

-CF needs to be improved to have some impact on PAT & Free cash flows… if not happens then growth guidance (2500 cr revenue Target in FY26) will turn out to be a hindsight

-My honest review

No Reco

Disc: Invested

Kovai Medical Center and Hospital – Health and Wealth (09-02-2024)

If we consider same PAT on 4 quarters. 53cr x4 = 212 cr

Kovai Medical Center and Hospital – Health and Wealth (09-02-2024)

How you calculated forward PE 17 ?

Kovai doesn’t give Guidance IMO

Kovai Medical Center and Hospital – Health and Wealth (09-02-2024)

A VERY GOOD Q3FY24 RESULT HAS BEEN REPORTED BY KOVAI MEDICAL ![]()

Q3FY24 Net Profit Of 53 CR

VS

Q2FY24 Net Profit Of 43 CR

VS

Q3FY23 Net Profit Of 31 CR

Net profit growth of 23% QOQ & 71% YOY

Available at a forward PE of 17

Neuland Laboratories Limited – Transformation towards niche APIs? (09-02-2024)

What was the most important key learning from the con call today?