Buy back regulations allow for increase in price up to 1 day before record date. Record date announcement will happen later.

Posts in category Value Pickr

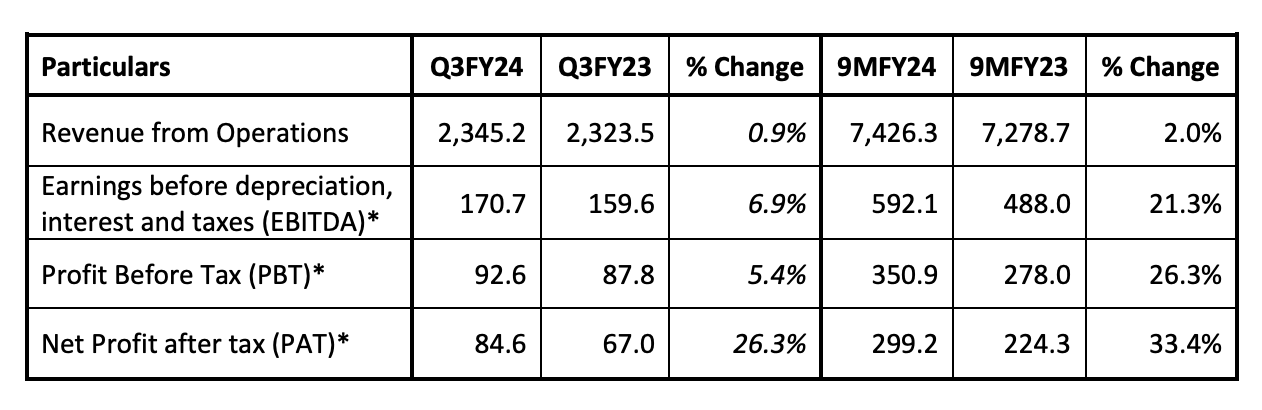

Tube invest india ltd (04-02-2024)

Tube invest india ltd has recently posted Q3 results, in which they have showed other income of Rs.551 cr. Can you tell me what is the source of this income?

Pharma || Hospitals || Diagnostics : Industry perspective (04-02-2024)

In hospitals, Brand is associated with Clinical Outcomes and the complexity of procedures. These are done when you have the best Doctors and the latest Equipment. if your and loved one’s life depends upon the operation you will do the research. The way new hospitals try to cover this by building 5 star buildings but outcomes are what matters. More complex surgeries you do more image builds for hospitals and famous people get operated and legacy is built.

Insurance companies and TPA would like to squeeze the margins of these hospitals but people can decide not take insurance from companies that don’t cover good hospitals. so the power of good hospital chain is immense. Think Breach Candy in Mumbai or Mayo Clinic in the US.

All the great Pharma company’s products even if it Novo Nordisk Ozempic will be recommended and can be sold by Hospitals.

No one is shopping for a cheap hospital esp with insurance. Life is precious so pricing power is unlimited.

The ART of Valuation (04-02-2024)

Hi Donald,

Thanks for insightful information. These pointers definitely are sure to look upon while investing. With the dynamic business scenario, was thinking there should also be some points on how fast the companies can adapt. With the advent of SME exchange, the money flows in faster, thereby increasing competition.

Need thoughts on how can we measure flexibility of a company to adapt to industry dynamics.

Godrej Agrovet ~ Animal Feed, Crop Protection, Palm Oil, Dairy & Processed Foods (04-02-2024)

What worked

- Animal Feed: 3.90KT this qtr, 2% revenue up.

- Processed Food: Revenue 21% up yoy. Mngmnt claims margin improvement is sustainable (Here).

- Domestic Crop Protection: Q3 Rev 172Cr, margin improvement

- Dairy, Bangladesh business

What didn’t work

- Commodity nature continues to impact profitability across different verticals

- Astec’s and Oil palm biz.

References: Presentation and Press release

Disclaimer: I may or may not be invested in Godrej Agrovet or its subsidiaries. I am not SEBI registered and this is not a buy or sell recommendation.

Praveen’s Portfolio (04-02-2024)

I think it’s valued same as peers like cantabil retail, TCNS clothing killer and other brands (excluding retailers like pantaloons, etc). For whatever reason, the stock didn’t do well at listing.

I’ve looked at this as an opportunity instead of worrying about why it’s not priced higher at IPO and didn’t list with good premium.

Anti thesis :

- Margin improvement from 10% to 33%. Margins may or may not be sustainable

- Wage hikes for lbaour could hit gross margin and so ebidta and profit margins

These are the only major risk I could see

Other risks could be not growing in 14-15% but as the industry is growing in this rate. This growth rates are within reach

Thesis:

- Not a asset heavy business, as the manufacturing is outsourced

- Operating leverage will play out as Same store sales growth continues

Valuation rerating upwards is a major part of investment thesis for me (in addition to 14-16% growth and operating leverage)

Disc : No reco

Praveen’s Portfolio (04-02-2024)

Great to see you adding this. I am also tracking this company since its IPO. The low valuation and a very decent looking Management attracts me here. But why would someone value their company at a good discount to listed players in such a roaring bull run? This has been stopping me from entering this company. I could not find much to read about the company either. Any theses you have to add?

Praveen’s Portfolio (04-02-2024)

Portfolio Update (as of 4th Feb 2024)

| Company | Weightage |

|---|---|

| XPROINDIA | 7.9% |

| PDSL | 7.4% |

| FINOPB | 7.1% |

| KERNEX | 7.0% |

| KRSNAA | 6.7% |

| MAYURUNIQ | 6.6% |

| REDTAPE | 6.4% |

| DCMSRIND | 5.3% |

| CIGNITITEC | 5.0% |

| KAMAHOLD | 4.4% |

| MOLDTECH | 4.2% |

| NSE:MCX | 3.9% |

| SAIL | 3.6% |

| Vishnu | 3.5% |

| Shreepushk | 3.3% |

| CONFIPET | 2.2% |

| DEEPAKFERT | 2.2% |

| SHARDACROP | 2.2% |

| MUFTI | 1.9% |

| NHPC | 1.9% |

| LAURUSLABS | 1.9% |

| ULTRAMAR 506685 | 1.8% |

| SBCL | 1.4% |

| KSCL | 1.0% |

| AARTIDRUGS | 0.8% |

| AMBIKCO | 0.4% |

| WIPRO | 0.1% |

Changes:

-

Added Mufti (Credo Brands): Trading at 20x P/E and seemed like a good opportunity in Fashion and apparel space. Industry growth is in double digits and the management expects to double the sales in 4-5 years. There is chance for operating leverage. Anti thesis: Need to see if the margins could sustain above 30%

-

Added NHPC: Bought via OFS as the allotment was below then CMP. Stock price has good momentum and so holding half the quantity of the allocation and sold the other half. No strong fundamental view expect that the power sector sees tailwinds in near future . Holding as there’s good momentum

-

Sold ANGELONE after the results (~3400 rs) as I see the margin pressure could continue in near future. May turn out to be a bad decision for me, but won’t regret

- Added small qty of Kaveri Seed Co. Ltd (KSCL) to participate in buyback as I see opportunity to make 6-8% in 2-3 months for small shareholders (investment < 2 lakhs)

- Added small qty of DCMSRIND as I see value unlocking coming out of demerger… Expected timeline of 2 years (may take more time depending on NCLT hearings and postponements)

Please feel free to share your views or ask questions on my PF or any of the cos mentioned

Thank you

Praveen

Disc: No reco to buy or sell.

Zen technologies – A micro cap in the defense space! (04-02-2024)

Thanks for sharing insights on the company. It’s quite concerning that the anti-drone segment is an assemble-in-India play and not IP driven product. I went through con-calls and found out this comment from Ashok Atluri.

“So, we think that we are in a very good space, but we expect competition to come, but how will they really get it even if we developed because it has taken us hell lot of time to develop this product hell lot of expertise.”

I hope you can share more details. If Zen’s anti drone products are just assembled products without any significant IP why did Zen take a lot of time to develop the products?