Significant reduction in pledged shares. No pledging observed in last 1 year.

Posts in category Value Pickr

Hero Motor – Leader in two wheeler (03-02-2024)

The current multiple is already on the higher side. The electric scooter business may not be as profitable as the ICE business, which means profitability at the consolidated level will be pulled down. Unless EV business improves profits, and scales up meaningfully, there is limited upside potential. Rest we know Mr. Market, the stock can go anywhere based on the mood. There seems to be limited margin of safety at these levels.

Disc: No holdings

Why Ramky Fall today with 20% , do not see any bad news also (03-02-2024)

May be due to profit booking… got nothing on internet

Burger King ~ Whopper of an Opportunity (03-02-2024)

Hey Rohit.

Any source for this. Thanks ![]()

Neuland Laboratories Limited – Transformation towards niche APIs? (03-02-2024)

Management may provide some clarity on revenue potential of KARXT drug in concal. Karxt drug is just a feather in the cap and since it is claimed to be a block buster drug, there will be lot of recognition for Neuland in Big pharma and Company may get lot of new deals. Over a period of 2 to 3 years we may see significant increase in number project molecules in which Neuland will be working. As discussed earlier in this forum, the nature of business is lumpy, however ever year the base will increase as evident from last several years.

Disclosure : Invested and adding in SIP.

Deepak Fertilizers and Petrochemicals (03-02-2024)

Management itself admitted that high margins in previous year were an aberration. Its a pure commodity play and accordinlgy valuations will also adjust accordinlgy.

EPS will be in the range of Rs 5 per quarter (i.e annualised EPS of Rs 20 ) for next 6 to 8 quarters. Now it is upto individuals what PE they can give for a commodity player.

Even if we give a PE of 15 to 20, there is a long head room for correction in valuation.

Further there is an over hang of 2 major CAPEX undertaken by the Company of around Rs 4000 to Es 4500 Cr (TAN & Nitric Acid)

Fertiliser business is making losses, overall margins are squeezing, Ammonia Capex of Rs 4500 Cr is making losses and Gas for Ammonia plant has been contracted at a higher price.

Disclosure: Exited position and now tracking for knowledge purpose.

Strides Pharma Science (03-02-2024)

Detailed investor presentation by the company. Provides more specifics around. Strides and OneSoruce revenue and EBITA targets in next 3-5 years. Overall market opportunities.

Disc – Invested

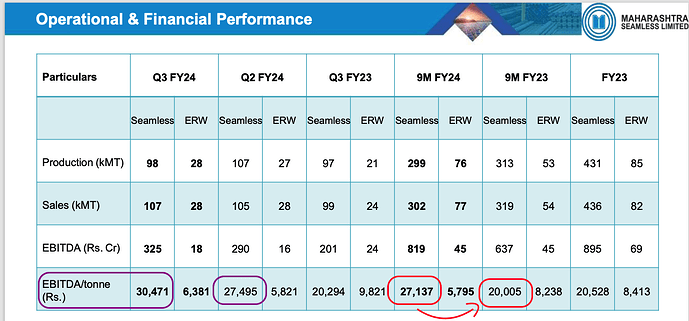

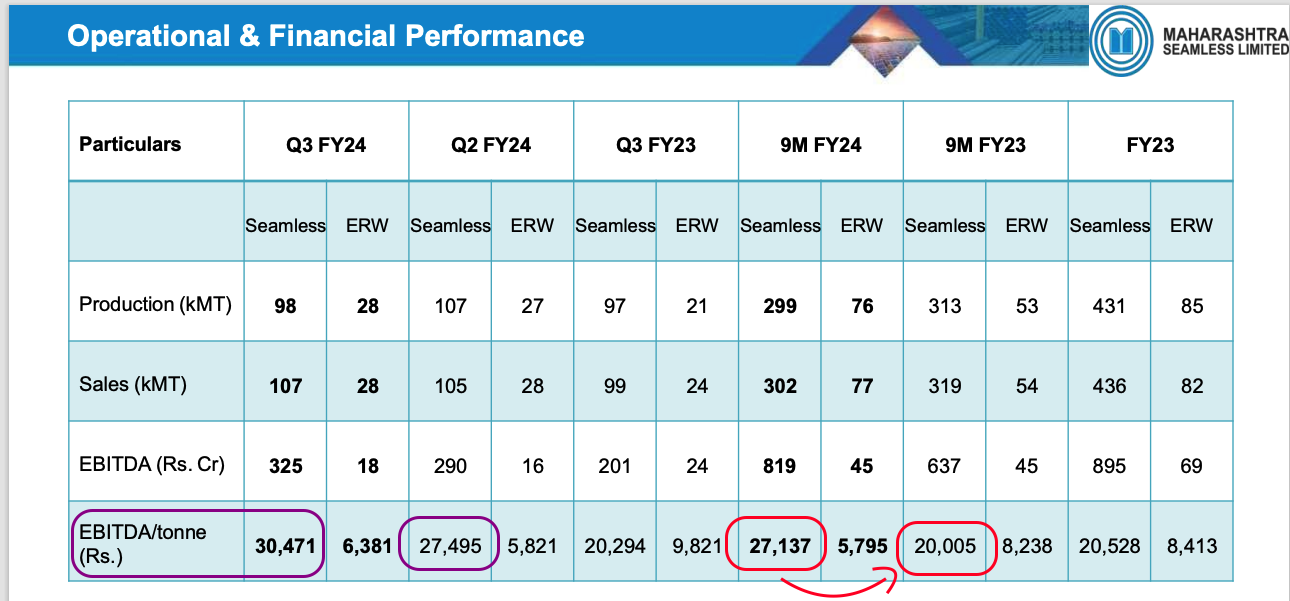

Maharashtra seamless-a value plus cyclical play (03-02-2024)

My takeaways from the conf call ( any mistakes are truly mine, as they were my running notes ):

- Highest EBITDA ( but on lower production volumes). Have been able to control costs.

- There is spending in O&G sector, and orders are getting topped up.

- Seamless pipe product down by approx 10% to 98 kMT from 107 QoQ but sales have been higher, indicating higher price for seamless pipes. Ebitda/tonne has also increases Q, Y and 9m YoY too.

- Domestic demand is high. Exports is only 10% and has not picked up over last 9 months, domestic has compensated. If we wanted to get export order, we could have gotten it by reducing the prices/margins, but we had more than enough domestic orders and hence export is lower.

- Promoter stake has increased over the past 2 years from 63 to 68, when will it improve to 75? No timeline, but would like to get to 75%

- Order book: 1563 cr.

- Orders are typically 3-4 months only

- why is there an increase in EBITDA/Tonne:

- Good domestic market. Export started declining from April of last year, and our margins started increasing from the same time. This indicates the domestic market is good and is indicative of higher margins.

- RM prices have declined. Steel price has come down. When the tender from ONGC came 3 months back and we book RM at a lower price. Not all or 100% of RM is booked, hence lower steel [RM] prices have helped in this quarter.

- FY25 the EBITDA/tonne will go back to 20,000 and will not sustain at 30,000 level. FY24 might close closer to 27,000 levels but FY25 will be lower. [ this year was more opportunistic – volatile market, higher prices for end product and RM was lower ]

- No plans for deploying cash back to shareholders. No opportunities seen yet for buying other companies, we are ‘hoping’ for an opportunity. Dividends plan will be in consideration.

- ONGC comes out with lower value and lower duration order, compared to in the past when it was a large one and for a full year out, unlike today where its for 3-4 months.

- We are one of 3 participants and are the market leader, we will get good orders.

- Exposure to oil and gas segment is 70% other area we cater too are: boiler and general engineering. Power sector uses boiler segment.

- ERW margins are going down. Two types of sectors for ERW we cater to: Oil and water. Depending on the sector, the margins fluctuate. Oil ERW has better margins than water ERW.

In my view, given that the margins are at an elevated level and the mgmt has stated that the EBITDA might not sustain at these levels of 30k and might revert to 20k levels in the next financial year, I have sold most of my holdings. Have transactions in the past 30 days.

AGI Greenpac- on the cusp of growth? (03-02-2024)

Date moved to 9 Feb. Taarik pe Taarik!

Skipper Ltd., (Power and Water) a moat in making? (03-02-2024)

Here is what the mail from ZERODHA says

Blockquote

These RE’s will be temporarily traded on the stock exchanges and will then be extinguished. You can either use the RE’s to apply for the rights shares of the company or you can sell them in the market.

So basically if you are applying then please do not execute any sale transaction. Hope that adds little more clarity.