The company has successfully placed its products in 50 Reliance retail stores and 13 Balaji Grand Bazar stores.

SSFL_01022024162937_Reg30.pdf (193.1 KB)

Posts in category Value Pickr

Srivari Spices and Foods Limited (02-02-2024)

Himachal Futuristic communication (02-02-2024)

Q3 2024 result is not impressive…

Any comments from experts?

PayTM (One 97 Communications Ltd) (02-02-2024)

Just to put things in perspective,

If you compare it with phonepe valuation with 47%+ market share vs 14% for paytm in UPI** that should give around 3.6B USD (phonepe last valued at 12B USD) + lending business is much bigger than phonepe or anyone else in fintech + PayPay’s 5% stake (it is major player in Japan where you can get good money for payment business, as per google search (https://www.reuters.com/markets/deals/softbank-considering-us-listing-paypay-payments-business-sources-2023-07-12/) last time it was valued at 7B USD+) + PayTM money has decent scale + Decent marketing and distribution business/ event business + travel agent business + Offline dominance in soundbox – this is piece will get impacted in near term but nothing that will kill it.

**I do not think P2P UPI will ever chargeable (of course there can be charge after some limit) but main income is P2M where I think PayTM has more comparable share with Phonepe.

This is as of now. Thanks!

Disc. Holding significant position in portfolio so may be biased.

HDFC Life Insurance Company (02-02-2024)

As per my analysis, Profit Before Tax has been trending downward in the past 4 years.

It has dropped from 1400 to 1050 Crores in the past 4-5 years.

Net Profit is also under pressure due to this.

As mentioned in this thread, they are expanding their Agents network and the revenue per agent is not yet up to the mark. So overall except growth in premiums, all other profitability parameters are under stress after acquisition of Exide Life.

It seems that, Management may need more time to show increase in profit parameters. Market may not be happy with this scenario of low or nil growth in PAT, hence Stock price is also under constant pressure.

Burger King ~ Whopper of an Opportunity (02-02-2024)

I have been tracking this business for quite sometime and here is my thought –

While the overall strategy of expanding and operating this business looks fine to me as already mentioned by @akhilgulecha the moot question to me still is how different is BK from McDonald’s and what prevents McDonald’s from taking away BK’s market share. At the end of the day, people don’t care for the brand name BK as long as long one gets similar quality products at lower prices.

I happen to accidentally visit and compare price and offerings of McDonald’s with BK and found McDonald’s offerings (similar products) priced lower to that of BK. Rather than comparing different QSRs a detailed comparison of McDonald’s with BK is more of an apple to apple comparison here. It should not be difficult for McDonald’s with its brand and distribution reach to take away BK’s market share in the coming qtrs/years. The recent q3 results of BK seems to indicate a slowdown in SSSG which reaffirms my thinking.

PayTM (One 97 Communications Ltd) (02-02-2024)

Paytm’s Marketing & Financial Svcs Biz Will Not Affected Due To RBI’s Curbs: Vijay Shekhar Sharma

any comments?

2 things is clearly gone, and that is wallet and fastag. Everything will be done with separate banking partners, like lending, PoS or QR. So, then what is the difference between PayTM and other fintechs like GPay and PhonePe. Especially PhonePe which provides almost similar suite of services like PayTM. The main difference was wallet, Fastag and Bank (ability to raise deposits, which can then be lent to customers). So, there might be issue of competitive pressure as well. This doesn’t look like an existential question as people are making it, but surely it will delay profitability in far future.

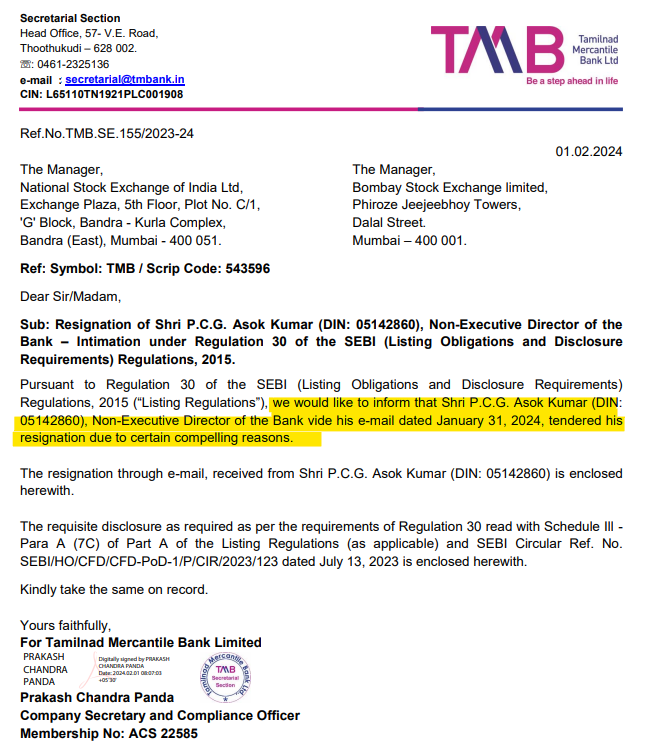

Tamilnad Mercantile Bank Ltd (TMB Ltd) – An undervalued pvt. sector bank? (02-02-2024)

Resignation of Non-Executive Director

Mr. P.C.G Asok Kumar tendered his resignation.

Note : He and his immediate relatives together holds almost 1.15% of TMB Ltd.