Added Bajaj Finance today

Posts in category Value Pickr

Indiabulls Housing – A compounder from here? (30-01-2024)

May be you are right. But, this is a massive dilution of equity and does not conform with their statements in the q2 investor ppt where around slide 6 or 7 they are projecting that every quarter they have 1200 cr to 1800 cr excess cash. Alternatively, they could have met this requirement easily through bank loans.

Skipper Ltd., (Power and Water) a moat in making? (30-01-2024)

What do you mean by ‘doesn’t make sense now’? @bully

Priyank’s Portfolio (30-01-2024)

Personal reminder to read between the lines

Link: https://www.bseindia.com/xml-data/corpfiling/AttachLive/7ed73bb4-384e-4a4e-8292-c049147eded2.pdf

Investment strategy review (Long term) (30-01-2024)

Inflation nibbles savings. Wrong investment devours it.

Imo you should take time to understand your needs, investment profile, and actions. Something doesn’t seem right (but this is my POV and I am naive).

Skipper Ltd., (Power and Water) a moat in making? (30-01-2024)

Hi Moonrise will try to explain to the best of my ability.

If you hold 10 shares you are eligible to buy 1 share of skipper.

To buy the same you have to follow the ASBA process of applying rights issue through the bank (the same way as you apply for ipo)

Caveat here is suppose you have 100 shares and you are eligible for 10 , you can apply for more than 10 through the ASBA application process. In the final allotment you might end up having more if other eligible shareholders have chose to skip.

I did a similar exercise with piramal pharma rights issue, I applied for 250 and got all the 250 where in I was eligible for only 150. Regretted that I should have applied more in the process.

Coming to the second part. you just need part payment to book the share , the rest you have to pay later once your shares are allotted.

If you are buying Skipper-RE from the secondary market then you will be allotted that many more. Doesn’t makes sense now as it trades at no discount value when I last checked.

AGI Greenpac- on the cusp of growth? (30-01-2024)

Looks like this SC case is not tilted in favour of AGI . And many be market is skeptical about HNG acquisition plan.

Orchid Pharma Ltd (30-01-2024)

Cefepime+ enmetazobactum(Exblifep) gets a positive opinion for marketing authorization by the committee for medicinal products for human use( CHMP) of the European medical agency. CHMP positive opinion will be referred to the European commission which will grant the final approval in approximately 2 months.

Interestingly, indications mentioned include Hospital acquired pneumonia including ventilator associated pneumonia, even though the original phase 3 study(ALLIUM trial) was done in complicated urinary tract infections. {Exblifep found to have good lung penetration(site of action for pneumonia) in one of the phase2 study}

chmp-summary-positive-opinion-exblifep_en.pdf (163.5 KB)

Current recommendation is based on ALLIUM, a phase 3 multicentre randomized controlled noninferiority double blind trial involving 1034 patients with diagnosis of complicated UTI / Pyelonephritis randomized to receive either Pipercillin-tazobactum ( current standard drug in complicated UTI) VS trial drug Cefepime-enmetazobactum( Exblifep).

EXBLIFEP demonstrated statistically significant superior overall treatment success (clinical cure combined with microbiological eradication) at test-of-care visit compared with piperacillin/tazobactam in cUTI, including AP, caused by Gram-negative pathogens (79.1% vs. 58.9%). Statistically significantly superior results were also observed among patients with infections caused by ESBL-producing pathogens (73.7% vs. 51.5%, respectively) with tolerable safely profile compared to standard drug. Study results were published in original article(behind paywall)

More details from Allecra website about the drug /study trial.

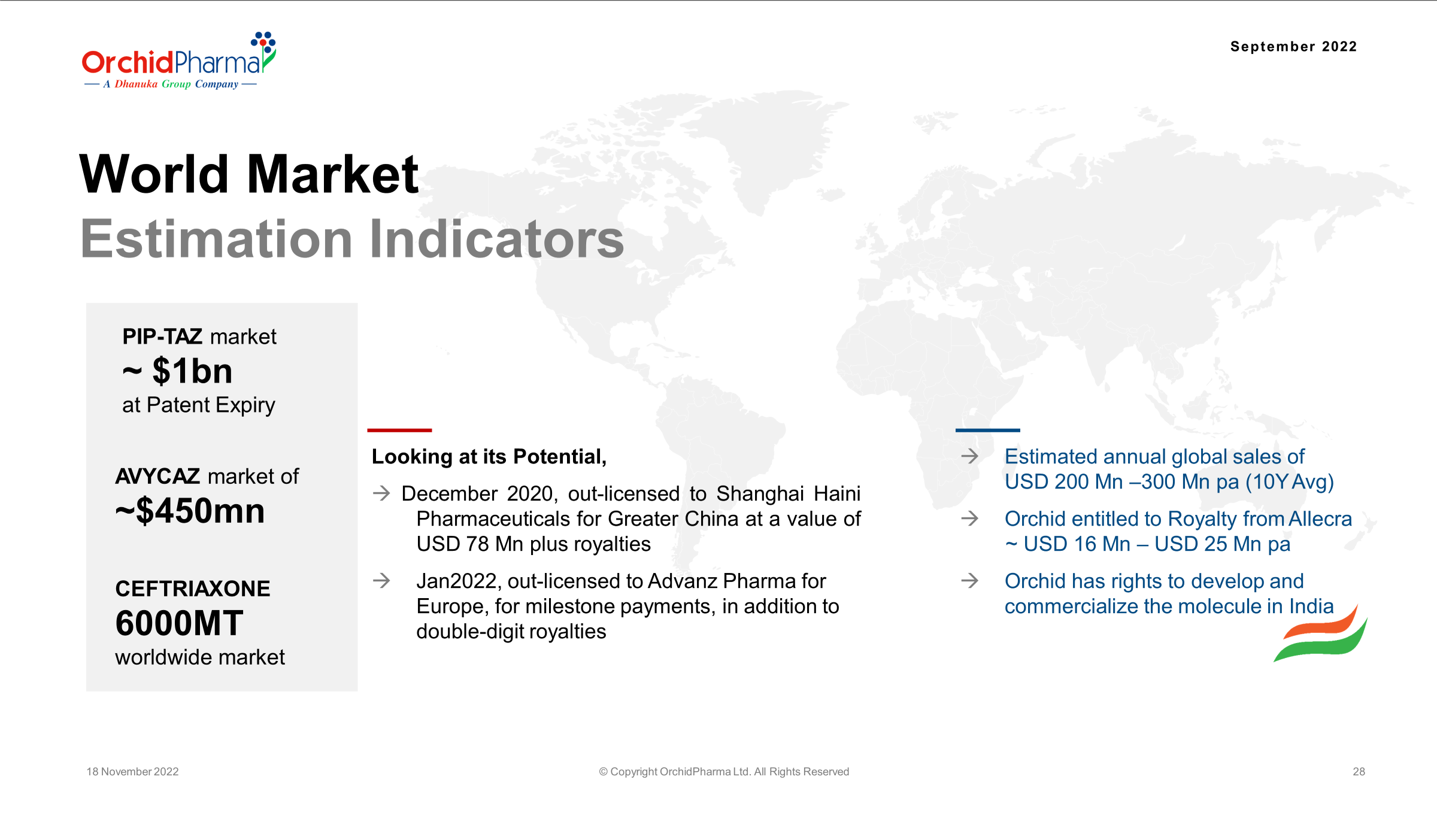

Orchid had licensed the Exblifep to Allecra for development/phase3 trial. Allecra inturn has licensed the product to Advanz pharma for commercialisation within the European union,UK, Switzerland and Norway.

Orchid will get royalty of 6-8% on global sales of Exblifep.

Orchid has indicated that( Nov 22 company presentation) estimated annual global sales of USD 200 mn-300mn per year and expected royalty of 16mn-25mn USD/year. With EU approval it’s likely that US FDA approval also should happen soon and global sales may start from the later half of FY25/26.

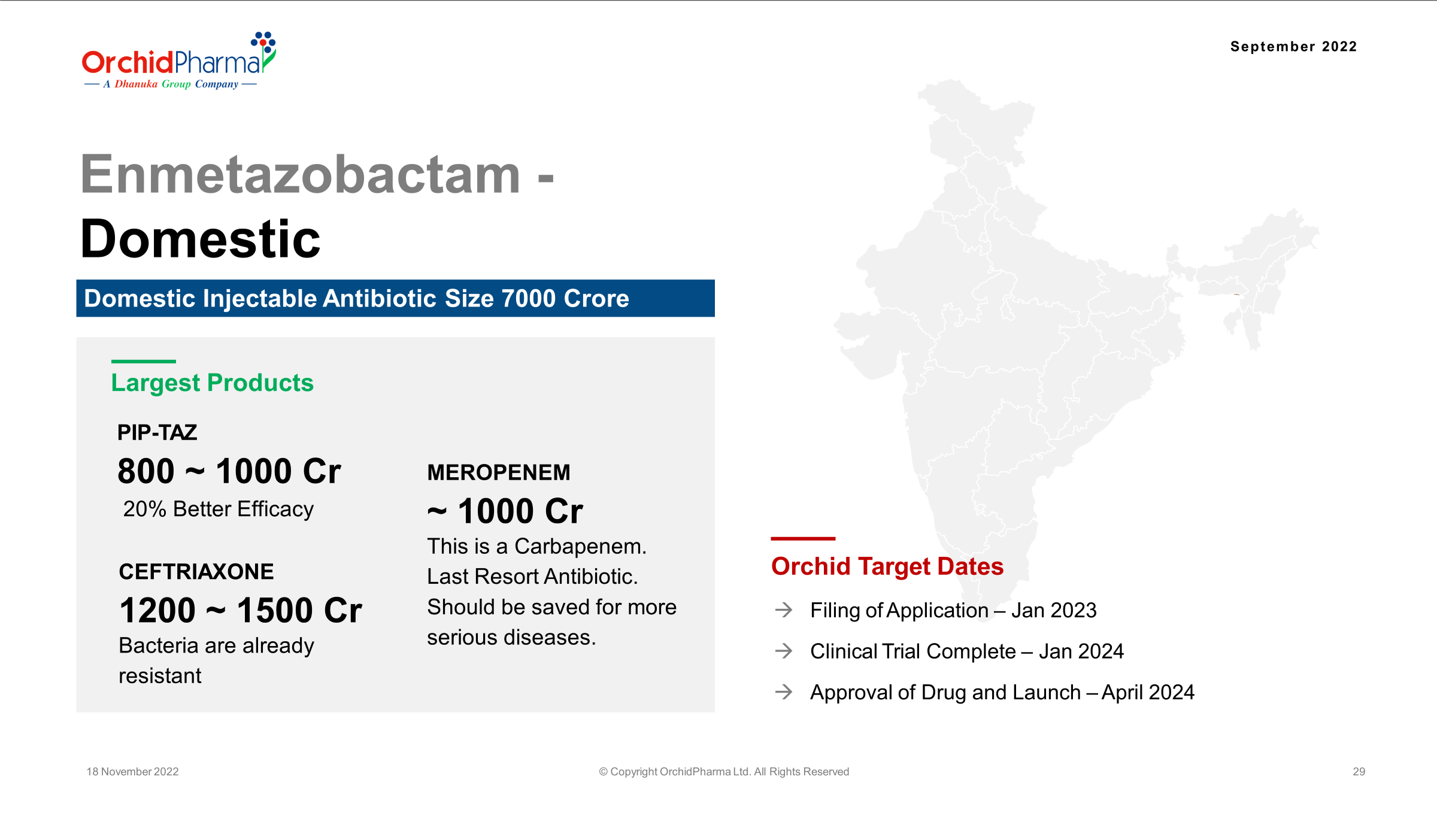

Orchid retained the right to market the molecule in India. current standard drug Pipercillin tazobactum market size in India in around 800Cr.

Disclosure: invested

Man Industries (India) Limited (30-01-2024)

@vineet_mittal

Man Industries has been heating up lately to the point where the rise is eye-soringly impressive! Do you think it’s still at good valuation to jump in ? What are your thoughts?

D-Tracking and plan to invest.

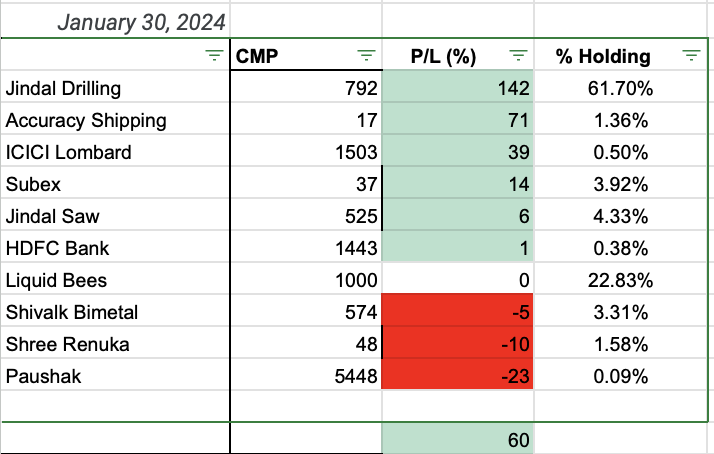

Portfolio Analysis (30-01-2024)

Update on the portfolio.

Some pointers:

- Continuing to hold Jindal Drilling as they’ve added rigs to enhance capacity. proxy play for Infrastructural development in India.

- Exiting Jindal Saw purely to book profits.

- Looking to exit Accuracy to book profits as well.

- Adding HDFC Bank to incorporate a large cap share with cheap valuation.