Posts in category Value Pickr

Is China investible? (29-01-2024)

China curbs short selling

The China Securities Regulatory Commission delivered, with new anti-short-selling rules aiming to stabilize the market going into effect on Monday:

- Per the new rules, investors who buy new shares will be barred from lending them out within an agreed “lock up” period, effectively closing off the mechanism used to bet against a stock.

- The move is similar to one China implemented during a similar period of market turmoil back in 2015, when activity from short-selling day traders was deemed as causing “abnormal fluctuations” in the market — a decision that ultimately failed to stem market losses in the following months.

The Complete Portfolio – SM (29-01-2024)

Exited Homefirst finance, policybazaar, gland, laurus (may enter laurus if it falls to 300 levels), nykaa, rhi magnestia, and Garware technical fibres.

Increased the allocation of Kotak bank considering valuations and TRIL recently.

Entered West Coast Papers again after 3 years. Shouldn’t have exited it. I still feel Bangur family (promoter of West Coast) is managing it extremely well.

The Complete Portfolio – SM (29-01-2024)

The decrease in promoter holding of Sonacom star is reflecting at FII holding so it seems fine. One of the reason could be addition of stocks in tax free SPV. So, it isn’t a worry.

Investing Basics – Feel free to ask the most basic questions (29-01-2024)

If a company’s promoter are selling some shares in block deal to some other investors and its has been reported in block deal section, is there no requirement to report that in insider trading section also?

P.S – By the way I’m talking about TIPS Industries

Tips Industries Limited – Ready to RACE ahead! (29-01-2024)

While I can see this in block deals, why its not reported on insider trading page?

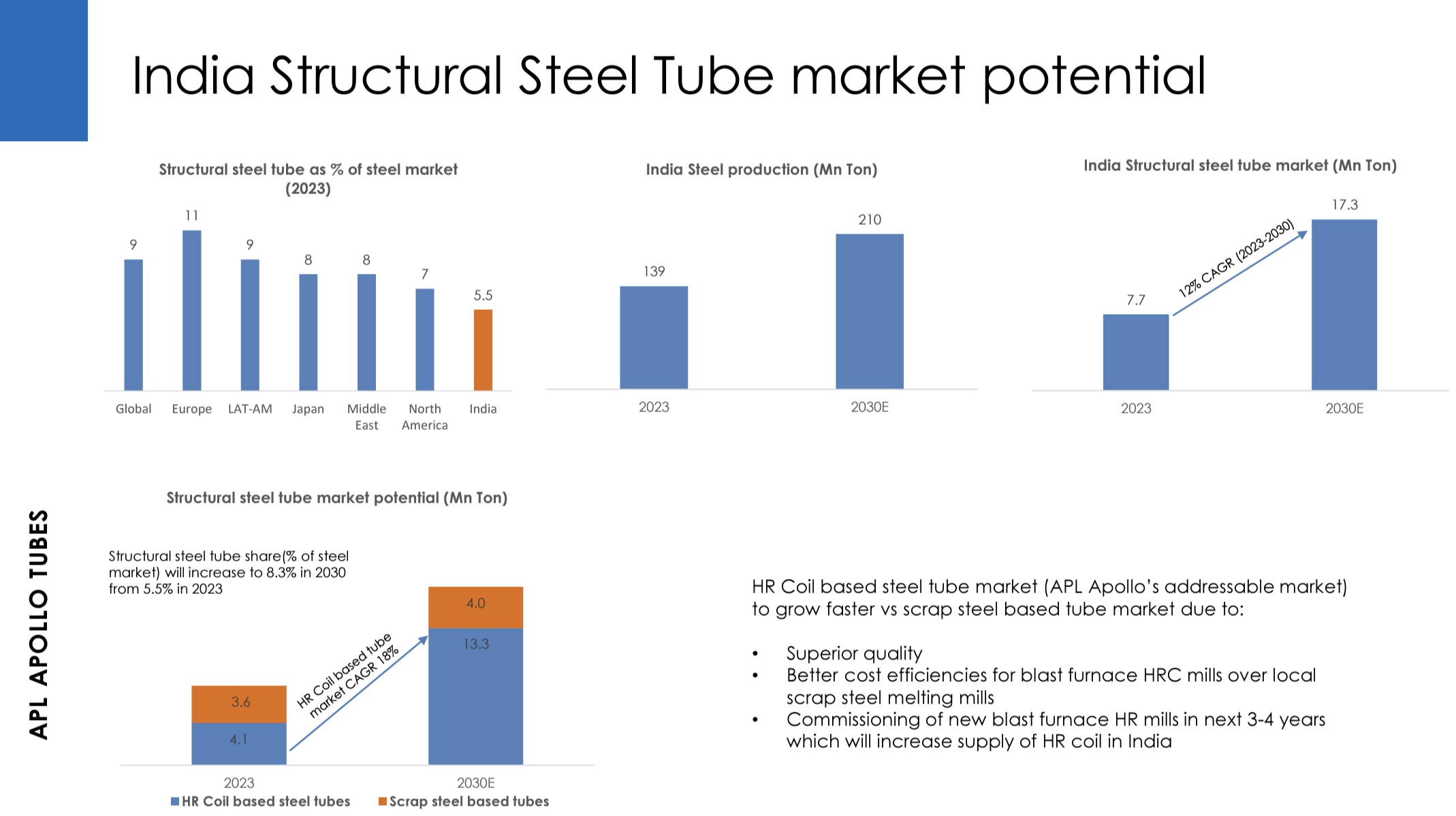

APL Apollo Tubes (29-01-2024)

Great slide on landscape for Structural Steel tubes

Olectra Greentech – Electric Bus Opportunity (29-01-2024)

Olectra Greentech is trading at a P/E of 177 times at a market capitalization of INR 13,902 CRORE as at 29 January 2024. At this price point, if you’re entering the stock – it’s hard to see any major upside unless the company can expand earnings substantially over the next few years. Can it do that?

I’ve written a detailed blog on ^. I cannot include the link to that blog here, in case you’re interested, check out the link in my profile bio or DM me for the link.

Here’s my summary on the brief reading of the Q2FY24 investor con call:

Pros

- Won order of 5,150 buses from MSRTC – which is the largest single order in the EV bus category in India. At the L1 stage for its order from BEST for 3K e-buses. Anticipating a tender of 10K e-buses from PM e-Seva, although how much share Olectra could get out of this 10K is unknown at this point.

- Expecting good order inflows for e-tippers in the next 6-12 months. But, no major order book for e-tippers at this point. Would need to watch out next few quarters to see if there’s any development here.

- Execution of the above order book as follows – (i) 2500-3000 e-buses in FY25 (ii) 4000-5000 buses in FY26.

- To achieve these volumes, company is expanding capacity. New factory being set up which should be able to commence production from Q4 with output of 3.5K units per year.

- Insulator segment is a [relatively] high margins segment. Olectra has market share of 45-50% with market size of 350-400 crore. Expecting revenue of INR 150-160 crore in FY24 from insulator segment.

- Invested in 50+ R&D personnel to bring in new designs + new models

Cons

- Delivered only approx. 240 e-buses in H1FY24. Targeting to deliver 1000 e-buses in FY24 due to disruption in production of 3-4 months. It has to complete certain testing / obtain certifications to comply with new battery norms. R&D costs have gone up due to extensive testing of products.

- Guidance initially was given to deliver 1200-1500 e-buses in FY24. Guidance has been lowered to 1,000 buses now. Gross margins decreased in Q2 due to change in product mix.

- Not going for equity fundraise but a debt fundraise to fund the capex expansion plans. 70% of requirement will be met with debt options and the rest through internal accruals.

Some general points

- Management expects partnership with BYD to continue beyond 2025. Olectra has been slowly acquiring technology + knowledge transfer from BYD. Sources battery cells + certain child parts for the power train from BYD which constitute around 25-40% of total components procured. The rest are sourced from local vendors.

- Hydrogen bus (partnership with reliance) is still in progress. Will take another year to get clarity on the potential of this project. Very early days.

- The management doesn’t have any plan to enter into 3 wheelers / passenger vehicle segment in the foreseeable future. Obviously, since they don’t have capacity to fulfil existing demand at this point.

- EBITDA margins on sale of e-tipper would be around 10-12%

Concluding thoughts: Olectra is a good business. Good potential. Robust order book. However, valuation plays a very critical role when investing in a company & unless Olectra can grow their profits 2X every year from here – the valuations look lofty with little margin of safety at this point.

Disclosure: Invested, looking to add if there is a good correction in the stock.

Newgen Software (29-01-2024)

Any incremental business is good – But 97 Cr over 7 years seems more like business as usual. ![]()