.

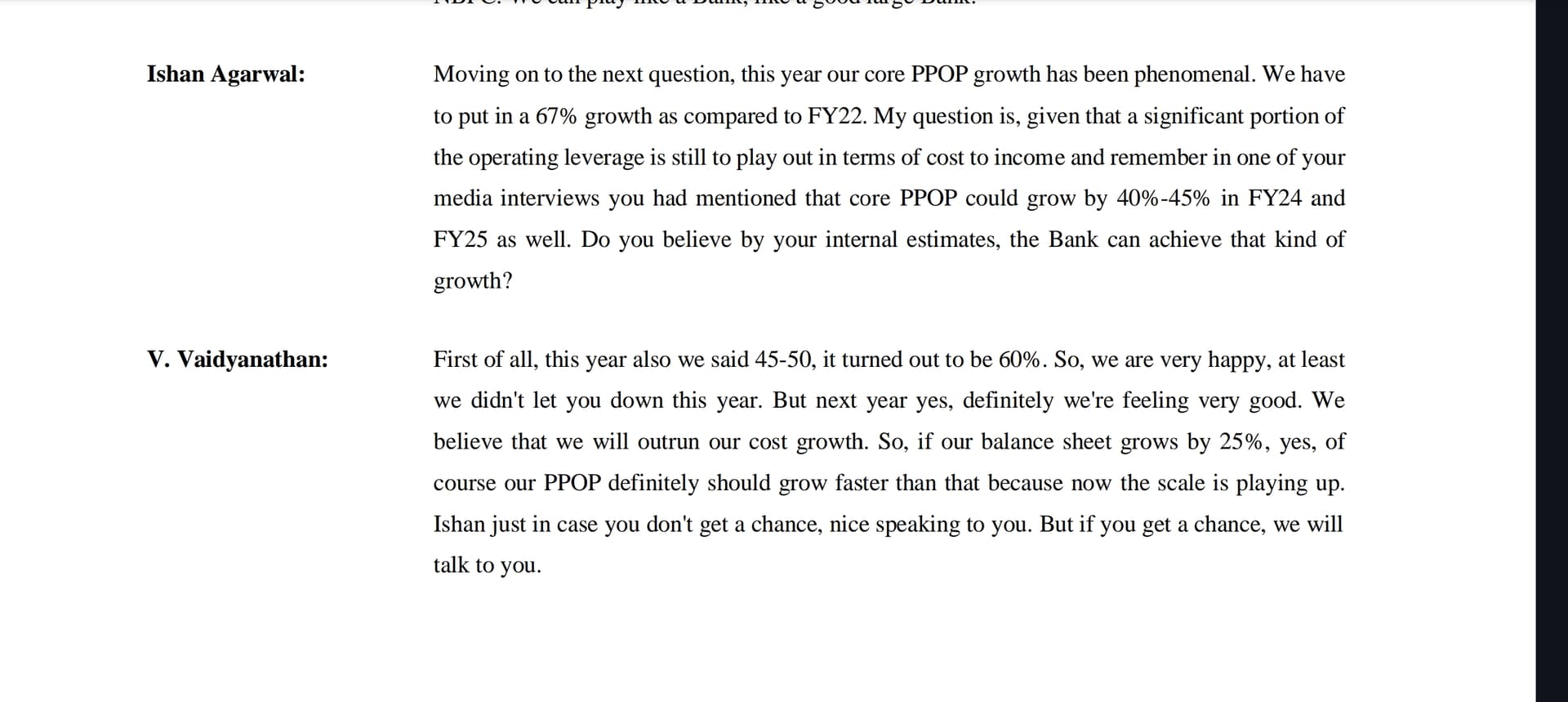

This is from Q4 concall on April 29th, 2023…Vaidya repeated same thing in many of his media interviews along with terms like ‘opening of the jaw’ and ‘J curve’ to signal that profits will grow significantly but in reality profits are declining from last 4 quarters along with dilution of equity.

.

Also comparing IDFC First with other established banks and saying that it has performed better than those does not seem to be the right way to looking at things imo, there is NO OPERATING LEVERAGE story at play in other good banks, they are already at a respectable number in terms of ROE, ROA and Cost to Income.

The problem is with management

over promising and under delivering and still trying to promise more in form of guidance 2.0

It’s not about judging it every quarter but about seeing the direction in which it’s going, bank’s performance is slowing down significantly QoQ and it will start showing in YoY number also from next quarter onwards.