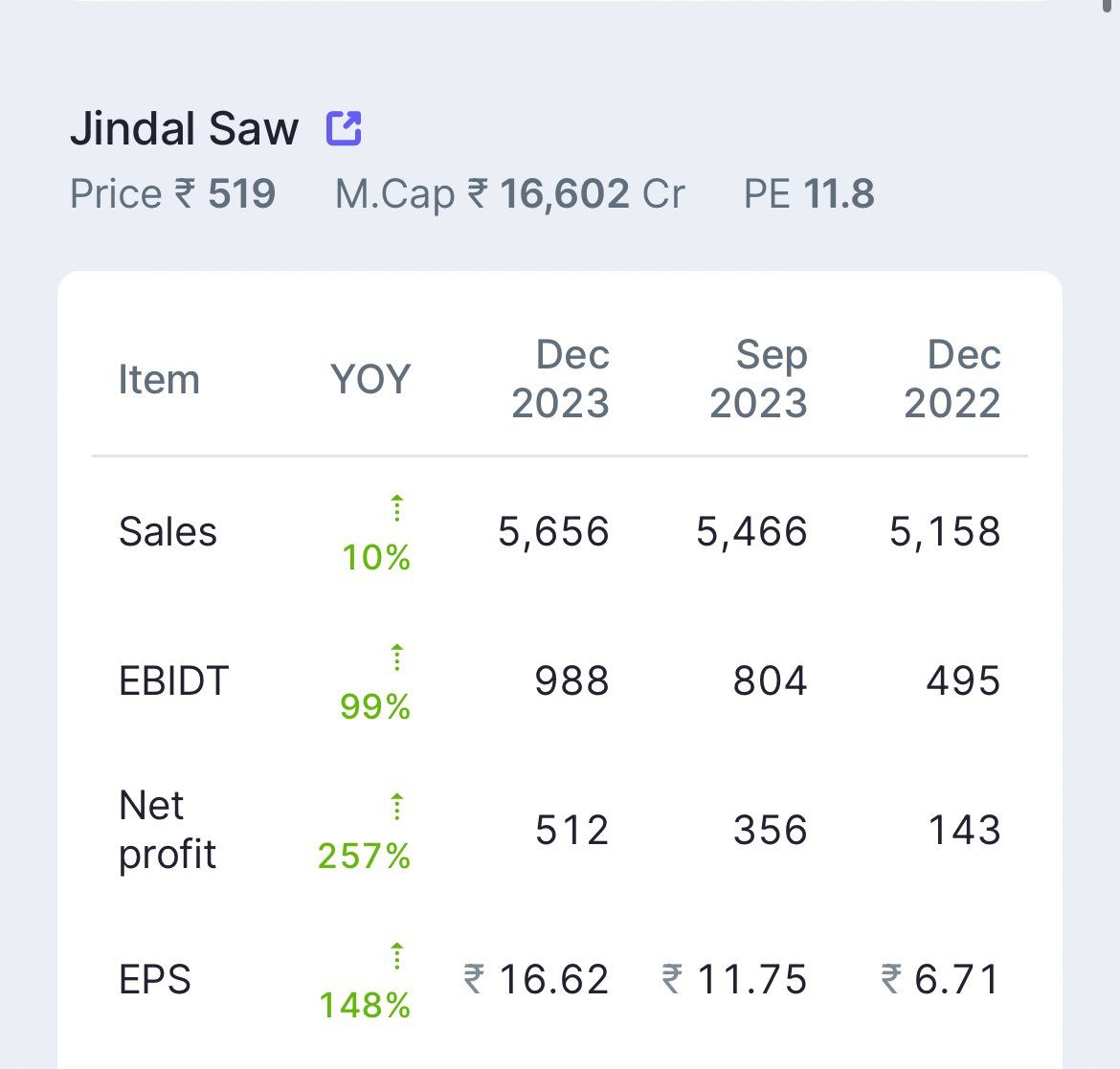

Extremely strong results reported by Jindal Saw as management said in the last concall.

Extremely strong results reported by Jindal Saw as management said in the last concall.

Edition 1: How to generate sustainable dividend income?

Challenges with Dividend Investing:

Establishing a reasonably large dividend income tends to be one of the primary questions that many investors have. It has its own advantages which we’ll not talk about as much. We are more interested in the challenge that dividend income tends to usually pose. Understanding challenges inherent in our paths is the first step in trying to overcome them.

So if I were to break it down, there is one large challenge to dividend investing:

Capital Appreciation Challenge: If a company is providing a large dividend, it automatically means that there is little in terms of growth opportunities for the company and therefore capital might not appreciate even in a roaring market.

A good investor would like to think of dividends as downside protection or some kind of stability that is brought into their lives, but they wouldn’t like missing out on the part related to growth.

Solution to the Challenge: We have to then build a framework to find companies that don’t really have large capital requirements to take part in future growth. This might look a little complicated, but typically in a business setting, there are ways to make money without putting in extra money every single time in terms of capacity or new products. We have to essentially find such companies to address the capital appreciation challenge.

Inverting the problem: What to not look for

Now in looking for what we need to find, let us first think about where we won’t find it for sure, here are a few kinds of companies that don’t give out dividends:

Banking and Financial Services Firms: There is a Capital Adequacy Ratio that banks have to maintain, plus they have to also invest aggressively in setting up branches and growing their asset base. This is why they don’t give as many dividends.

Non-Shareholder friendly companies: Companies that tend to have high cash and investments on the balance sheet are not supportive towards shareholders.

High PE Companies: The valuation for these companies tends to mostly come from the multiple that is assigned to them and not necessarily their actual profits. So the ability for them to grant dividends is severely constrained.

Low Growth Proposition: These are typical value traps type businesses. Wherever there is lower growth, the ability to grow in India is really crucial because of the kind of market we are, without it any investment will have terminal value risk.

With this assessment we have eliminated a large universe of companies from which we’ll not look to invest for dividend purposes.

Framework for the companies we are looking for:

Now we shall look at the framework for companies that can provide a good dividend, this will be in the increasing order of risk:

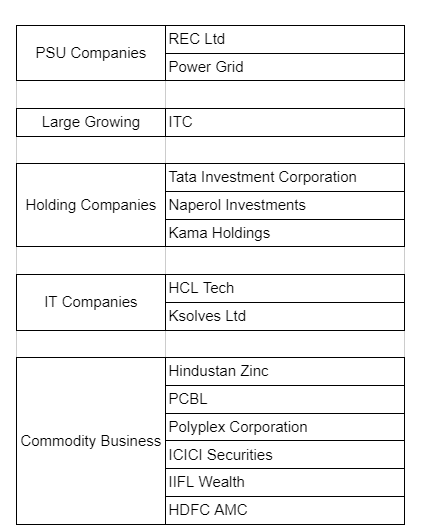

PSU Companies which are seeing good growth:

PSU companies have a mandate to give dividends to their largest shareholder ie the government. If they are seeing good growth or you feel there are triggers in the future that can ensure this, they present a great opportunity for capital appreciation and dividends. This is what has happened in the past few years in these companies with the growth coming back.

Large cap companies that are diversifying to fast growing sector:

examples like ITC would include these companies. Essentially the company should be gaining market share or staying constant in terms of market share but have better growth plans for the future. The fast growth would ensure these stocks don’t become a value trap. It is better if these companies have an announced policy of a set percentage dividend distribution for their shareholders.

Hold Cos:

Holding companies of fast growing companies can present another good opportunity but what tends to help here is some sort of understanding about how the hold cos discount tends to move and how it has moved in the past.

Fast Growing IT companies:

IT companies that are exhibiting growth regardless of their size are another candidate of good dividend generation. These are truly asset light companies as we discussed above. Track IT companies for when there are valuation gaps that you perceive and invest heavily to reap in good times.

Commodity Business with high growth rates at the right time:

Commodity businesses with high rates of growth in good cycles can present a good investment opportunity if you invest at the right time. What is a right time? It is when the margins are at their lowest cyclically or are bottoming out. I think the Poly films businesses are at that stage currently.

I’m sharing an illustrative list for what kind of companies we have discussed here.

In the next post, I’ll discuss a few examples of good dividend opportunities.

I think there is very little attention that is paid to this topic which is around how one can utilise the market to achieve certain specific goals. But this is a very structured query, and therefore there can be a very good response to such a question when one tries to solve the problem from a first principles basis.

I’ll try to take the approach of taking up a query which is commonly asked and try to resolve it through a framework and then give specific recommendations using that framework to satisfy both audiences, i.e. those who want to answer questions themselves and those that just want the answers.

Gradually if this thread does see good engagement I think we can start picking up queries that people might have and try to resolve them collaboratively.

There is no such thread already on VP so hoping to get some first mover advantage here.

See you in the first edition.

As Expected Good Q3 Result

Each n every company compulsorily declares quarter ending shareholding pattern on bse and nse website…

Will delete this post after a few hours…

Pl don’t take offence but if you trust the judgement of Trendyline you will never be able to catch a multibagger.

I have monitored some of my portfolio stocks including Shivalik Bimetal over last 2 years. It was always shown as an expensive start after it crosses 150 levels(pre bonus price).

So pl be informed about the value of these platforms. Their data is very quantitative and lacks quality of analysis which only a human mind can do.

which platform do you use to track FII / DII share holdings

Anyone has clarity in why the share is moving so much so quickly?

These are findings from Google bard AI

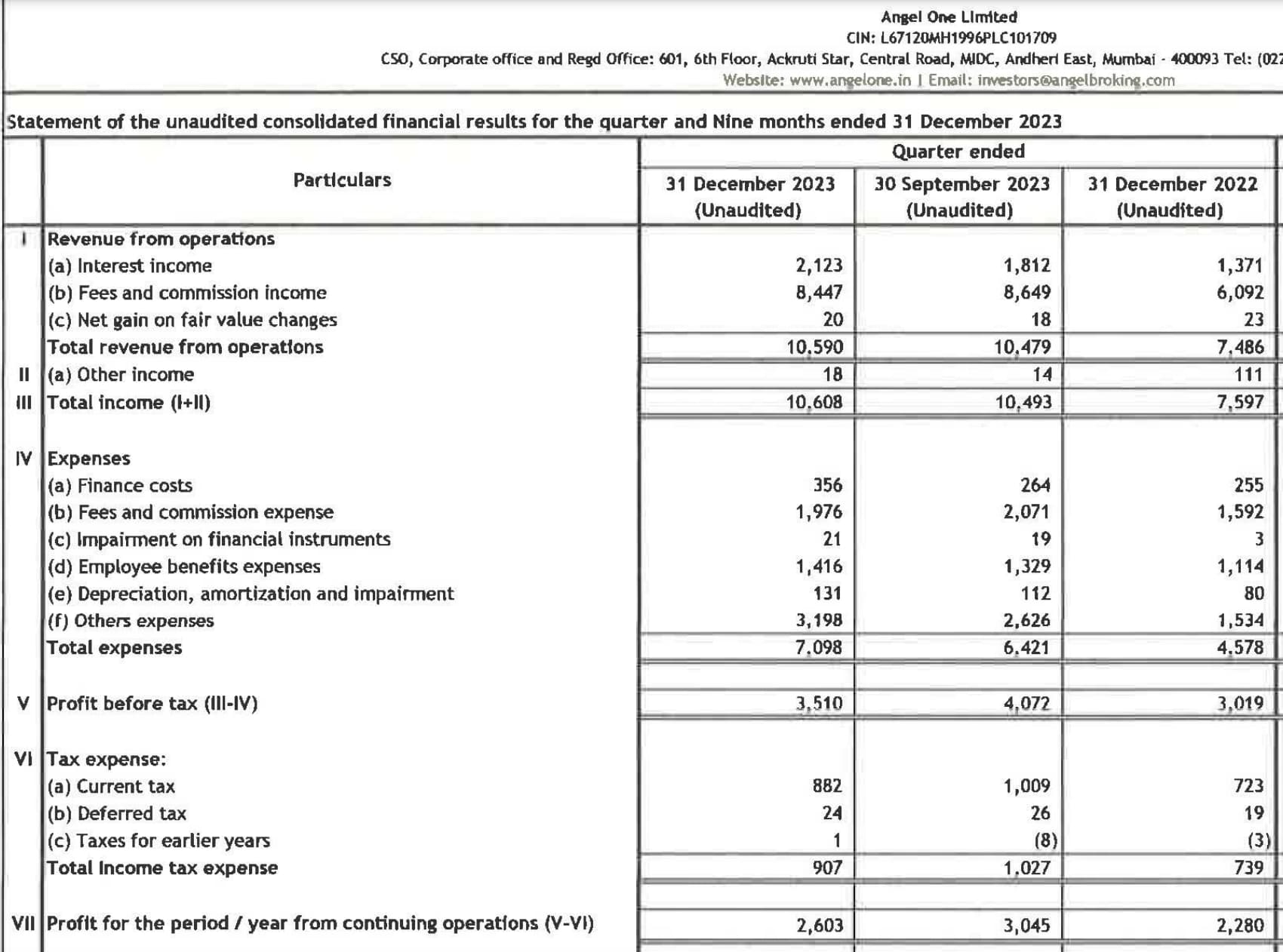

Angelo One Q3 results are released yesterday. There is good revenue growth QOQ and YoY.

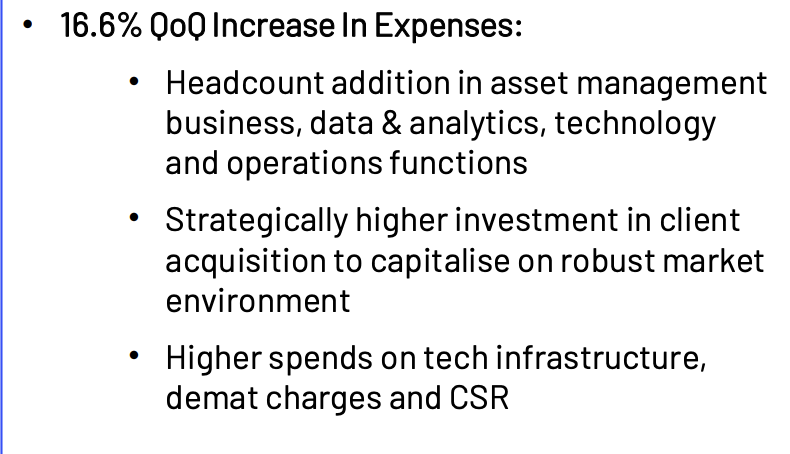

But the PBT is lower QoQ due to other expenses which were higher QoQ by 16%. Look at snapshot below from investor presentations

While this is ignored by some investors as the expenses are related to business growth, not every investor (short, medium and longterm) may look at it the same way. My thoughts below

The above mentioined points may lead to Time correction (may be price correction as well) in near future.

Disc: Just sharing my thought. Not a recommendation to buy or sell. Please do you own due diligence. Exited in personal PF but holdings in family PF