to simplify, YES!

PE in general is the hive expectations baked into CMP. although that’s reductive in nature, however it won’t be unfair to say that PE isn’t in our hands in short/medium term – thus speculative.

to simplify, YES!

PE in general is the hive expectations baked into CMP. although that’s reductive in nature, however it won’t be unfair to say that PE isn’t in our hands in short/medium term – thus speculative.

Just add on, recently CMS published this article on 3rd Jan 2024:

Key points:

This is July 29, 2019 news. Players of Cable Industry in Fake ITC Offences. Looks like evasion is on an industry level. But I am not sure if Polycab is guilty.

Disclosure: Not Invested.

I am closely tracking this company, some good MFs (PPFAS, SBI) also invested and have decent allocation, still not figuring out why the market is not giving value to this company,although Promoter as well as Financials are very good.

One concern that i think is – Trend of increasing UPI(Govt Push as well).

Disc – Not invested but tracking like a hawk eye for Price Volume actions.

I don’t know why he has entered, but money managers don’t start their work from numerical metrics. They get to know the business, in detail, and take positions as per their outlook of the business. We, as retail, start with metrics, screeners, as our resources are limited, including time. Managers have teams, they have people who dig up all the necessary information and data, not to mention the channels and connections they have, using which, managers take decisions along with their own experience and philosophies.

So, we might be playing in the same filed, in fact the same game, but the way the game is played is different.

Can some one pls update if there is any other open offer after recent Abuja’s 50% acquisition?

hi,

If any one can throw light on “Why Ashish Kacholia entered PTC industries at such high P/E” Means what should be the reason fundamentally

After Spending a 3 days and Refer Above Thread Here is My Take

Industry Overview

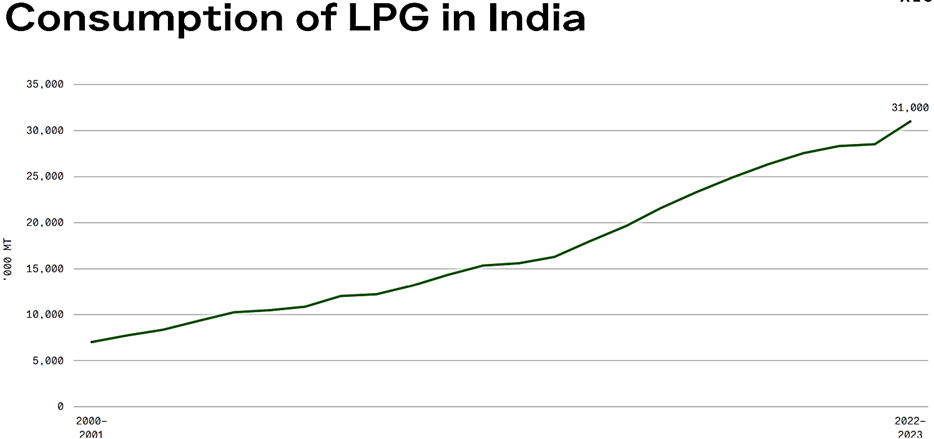

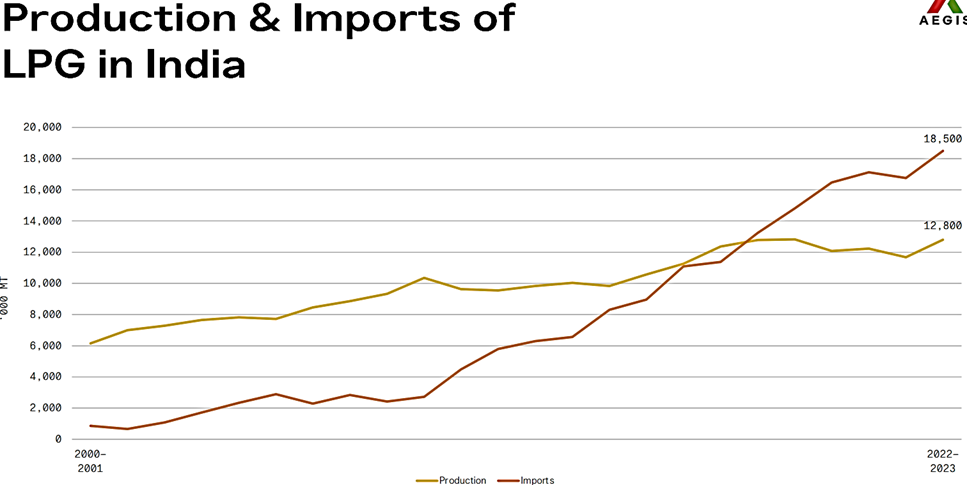

According to the fortune business insights the size of the world market for liquefied petroleum gas was estimated at USD 128.48 billion in 2020, and it is expected to increase at a compound annual growth rate (CAGR) of 7.3% from USD 129.17 billion in 2021 to USD 211.96 billion in 2028.

The demand for LPG in India was 30.6 million tonnes in FY2021 and is expected to grow at a healthy CAGR of 1.78% until FY2030, when it is expected to reach 36.9 million tonnes.

Company Profile

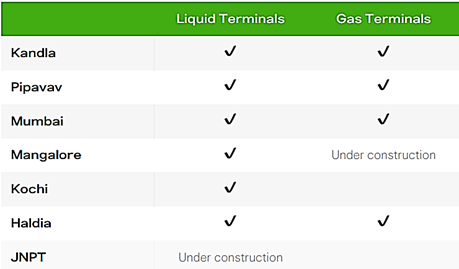

Aegis Logistics incorporated in the year 1956 and plays a key role in India’s downstream oil and gas sector

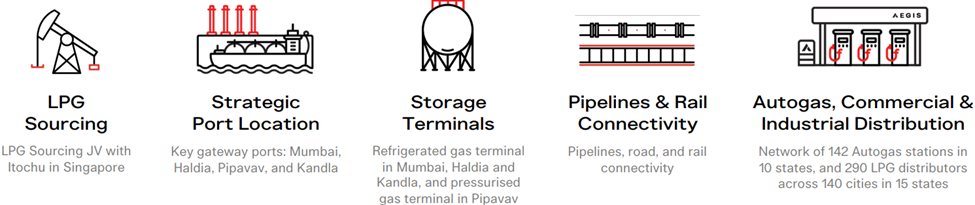

The Company is engaged in providing logistic solutions for Oil Gas, Chemicals and Petrochemical Industries and operates a network of bulk liquid handling terminals, liquefied petroleum gas (LPG) terminals, filling plants, pipelines, and gas stations to deliver products and services

Company has Network of 142 Autogas stations in 10 states, and 290 LPG distributors across 140 cities in 15 states.

The company operates through its state-of-the-art Necklace of Liquid & Gas terminals across major ports of India having a storage capacity of 15,70,000 KL for Chemicals & POL and 1,14,000 MT of static capacity for LPG.

Why I Liked To study?

Business Model

Aegis Logistics Ltd, along with its subsidiaries, provides logistic solutions for oil, gas, chemicals and petrochemical industries. The business of the company can be divided into two broad segments, viz., liquid logistics division and gas division.

Business Segment –

Key Clientele & relationship

Competitive Strength

Future Outlook

Risk

Dis: Only For Educational Purpose

Dr Reddy’s lab seems at very attractive valuations –

PE: 18

Industry PE: 35

ROE: 21.6

ROCE: 26.7

any idea… any one see why… or any problems with Dr reddy’s…