you may have a target of keeping max 20 stocks or so. it will be easier for you to track. also, when new to the market, you may look specifically into large cap blue chip stocks like hdfc, tcs etc to learn. eventually get into small cap. i am doing the same.

Posts in category Value Pickr

Samarth’s Portfolio (25-12-2023)

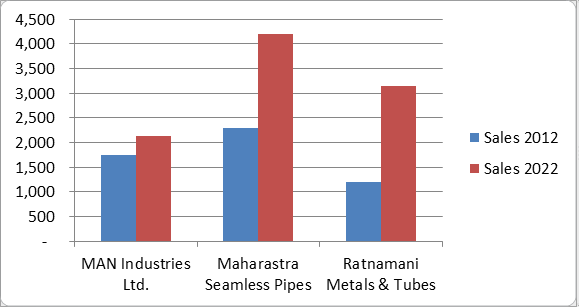

I will be sharing my thesis about my take for MAN Industries Ltd. so that we can discuss and most importantly you can share your points of disagreement and insights because ig that’s how we learn and grow

Brief Introduction:

The Man Group was promoted by the Mansukhani family in the 1970. It is a diversified group with its flagship company Man Industries (India) Ltd incorporated in 1988. The Company is engaged into manufacturing of Line pipes, Core Carbon Steel LSAW & HSAW Pipes, API grade ERW Pipes, Seamless Stainless Pipes & Steel Bends & Connectors.

The Company has two facilities at Anjar, Gujarat & Pitampura, Madhya Pradesh totaling 10 MTPA per annum equally distributed between LSAW & HSAW Pipes and recently company has commissioned 1.25 Lakh Tons API grade ERW pipe manufacturing facility. The company has recently declared its foray into Seamless Stainless Steel Pipes manufacturing with capacity of 20,000 tons per annum.

Brief History:

The Company has a history of poor corporate governance due to promoter disputes regarding ownership/Title rights to shares & Acquisition of shares during closer of trading window. The company has two promoter groups mainly JCM group & RCM group. The Bombay High Court has given the statement in favor of the company and currently RCM Group heads the company.

My Rationale :

- The Company is doing a Capex of around Rs. 170 Crores in setting up API Grade ERW pipe manufacturing facility, Rs. 800 Crore Capex for Seamless Stainless Pipes & DFT technology Pipes & Rs. 75 Crores Capex for Steel Benders & Connectors totaling to Rs. 1045 Crores. Whereas the entire capex in the last decade from FY12 to FY22 was Rs. 403 crores hence, the current capex program is 3x the capex done historically.

- Our Take on the company earlier had internal family & promoter disputes but that doesn’t translates into lack of integrity secondly the company faced governance issues primarily related to procedural violation of security laws but, no money was siphoned out of the company.

- The current promoter group is making serious efforts to rebuild the image of the company by engaging in quarterly concalls giving raw explanations regarding the historical disputes and timeline by which it will be solved

- The Company’s has forayed into value added products that are high margin products which will help company to improve its EBITDA margins (%).

- The Company’s traditional business of SAW pipe manufacturing is not a very attractive business & the industry suffers from over capacity plus the ROE for last 10 years has been 10% & MAN industries is also not a industry leader in it. They are however, expanding into high value growth products.

- The company is available at a relatively cheap price (P/E ratio: 19.5, 6x PAT of FY24e) which offers good safety of margins to us.

- The Natural gas pipeline sector in India is going through structural transformation and is facing strong industry tailwinds as India intends to increase the share of natural gas in energy mix to 20% from current 6% by year 2030.

- The government also Target to increase the pipeline coverage by ~54% to 34,500 km by 2024-25 and to connect all the states with the trunk natural gas pipeline network by 2027.

- Capex under City Gas Distribution Scheme, Nal se Jal Mission, Jal Jeevan Mission & National River Linking Scheme are further providing strong tailwinds to the sector & LSAW & HSAW pipes are widely used for water transportation.

- The SBI lead consortium has supported Company’s expansion plans by granting them working capital & long term debts for their ERW plant they also conducted special audit on the company, they wouldn’t have granted the loan if they would have found siphoning of the fund it is to be noted that the current loan has been sanctioned to the company after the Forensic audit conducted by SEBI & transaction audit conducted by SBI led consortium.

MAN Historical Growth has been Poor:

- MAN lost almost a decade due to internal promoter & family disputes

- Over the last decade from FY12 to FY22 total cash generated from operations is Rs. 1562 Crores only Rs. 403 Crores were invested back into business.

- The company lost the market share and order book to the competitor leading to lack of growth & expansion.

Expectations of the Management:

- The Company aims to have sales of Rs. 5000 crores or more by FY 2025-26 & growth of 20% CAGR in revenue from now.

- The company targets EBITDA margins in the range of 11-15%

- The company has an order book of 13,000 crores as on this date and expects conversion rate of 20-25%

- The company aims to expand revenue from ERW pipe, Seamless Steel Pipe Sale to Rs. 1700 Crores

- Expects sale of Rs. 200 Crore from ERW pipe sale in the current year

- The Stainless steel pipe plant will become operational from Q1FY24 & start full fledges production from Q2FY24.

Concerns for the company:

- ERW pipes & Seamless Stainless Steel Pipes is a new sector for the company & does not have existing relationships with clients in this sector

- The Company derives majority of its revenue from Oil & Gas industry and even today the capex of this industry is linked to oil prices and the sector goes through cyclical in nature.

- The Company has contingent liabilities worth Rs. 406.33 Crores & Disputed Debtors worth Rs. 95.20 Crores however; the company has given guidance that the company will be able to recover the amount.

- The promoter groups have dispute regarding right to receive dividends of Rs. 4.45 Crores however; the Bombay high court gave decision in favor of the company and the JCM group has further challenged it in Supreme Court of India.

*Not a SEBI registered Research analyst just sharing my views and its for learning indeed

Deepak’s portfolio requesting feed back (25-12-2023)

Sold further SGB and raised further cash. The percent of Gold holdings to total holdings is approx. 7.5 % now from a peak of 55 in Dec’22. Saw few twitter feeds on how people are quitting jobs to become full time investors. When I stated this to my wife the reaction I got was don’t even dare.

@saikathalder I’m still learning the nuances of investing yet. All the books I bought are at various stages of completion. still figuring out . Also I started building my portfolio after 2021 when I started to deploy some serious money. The small cap carnage during 2018-19 is still fresh in my memory. I continue to deploy funds when ever I have them, looking for margin of safety in the scripts I invest. Due to time correction of blue chip and me adding more funds in to it (Kotak @1750) or due to the run up in midcap where I couldn’t add more (idfc@40) their size of portfolio becomes significant. Others I would have taken a tracking position and I wouldn’t have any discretionary funds to deploy which I would sell them off for meagre gains. I can have significant allocation if I have a thesis. Also adding cost price to make my case clear ![]()

For example EIH I deployed funds faster (reallocated from SGB) as I want to have a significant allocation in hotel sector.

Similarly in Aegis logistics I wanted something from logistics sector so made a huge initial allocation (reallocated from SGB) .

Piramal pharma I sold all my holding after the last result and the ones I have were allotted in rights issue where I had substantially lower price than the prevailing market price.

Granules and Rain I took a tracking position and I don’t want to scale up. Uniparts just doubled the allocation will increase more if the results are good.

I do book profits now and then.

| Instrument | Avg. cost | LTP | Net chg. | Allocation |

|---|---|---|---|---|

| KOTAKBANK | 1733.29 | 1861.3 | 7.39 | 11.1% |

| IDFCFIRSTB | 37 | 88.45 | 139.05 | 8.5% |

| SKIPPER | 70 | 225.85 | 222.64 | 6.0% |

| INTELLECT | 524.72 | 811.7 | 54.69 | 5.2% |

| KNRCON | 267.46 | 260.55 | -2.58 | 3.8% |

| SGBJAN29 | 4745.48 | 6170 | 30.02 | 3.7% |

| SGBJ28VIII-GB | 5341.6 | 6161.74 | 15.35 | 3.7% |

| SGBJUN29II-GB | 4894 | 6170 | 26.07 | 0.1% |

| FLUOROCHEM | 2783.67 | 3569.05 | 28.21 | 3.4% |

| CARYSIL | 658.91 | 859.95 | 30.51 | 3.1% |

| AEGISCHEM | 295.68 | 364 | 23.11 | 3.1% |

| IDFC | 43.83 | 124.2 | 183.37 | 3.0% |

| KILPEST | 324.69 | 824.15 | 153.83 | 3.0% |

| EIHOTEL | 224.82 | 237.55 | 5.66 | 3.0% |

| HDFCBANK | 1490.18 | 1670.85 | 12.12 | 2.8% |

| VINATIORGA | 1769.9 | 1715.2 | -3.09 | 2.7% |

| HDFCAMC | 1723.06 | 3221.5 | 86.96 | 2.3% |

| SATIA | 114.52 | 142.9 | 24.78 | 2.3% |

| HBLPOWER | 92.66 | 443.3 | 378.43 | 2.1% |

| AVANTI | 394.63 | 398.5 | 0.98 | 2.1% |

| SUNTECK | 283.81 | 428.7 | 51.05 | 2.1% |

| HINDUNILVR | 2382.61 | 2575.6 | 8.1 | 2.0% |

| ASAHIINDIA | 479.46 | 564.3 | 17.7 | 2.0% |

| UJJIVAN | 243.33 | 577.2 | 137.21 | 1.8% |

| KSCL | 568.12 | 608.2 | 7.05 | 1.7% |

| PAUSHAKLTD | 5778.43 | 5680 | -1.7 | 1.6% |

| AMBIKCO | 1376.06 | 1743 | 26.67 | 1.5% |

| KRBL | 236.6 | 353 | 49.2 | 1.5% |

| NATCOPHARM | 624.19 | 792.2 | 26.92 | 1.4% |

| APLLTD | 730 | 773.4 | 5.95 | 1.4% |

| UNIPARTS | 559.91 | 536.15 | -4.24 | 1.2% |

| DHPIND | 350 | 798.15 | 128.04 | 1.0% |

| DRREDDY | 4468.46 | 5633.35 | 26.07 | 0.9% |

| MARICO | 350 | 523.6 | 49.6 | 0.9% |

| PPLPHARMA | 81 | 140.5 | 73.46 | 0.8% |

| UJJIVANSFB | 30.2 | 57.7 | 91.06 | 0.8% |

| RAIN | 150 | 145.1 | -3.27 | 0.7% |

| ICICIGI | 1078.37 | 1422.6 | 31.92 | 0.7% |

| PRAJIND | 545.13 | 562.05 | 3.1 | 0.7% |

| GRANULES | 275.72 | 385.55 | 39.83 | 0.6% |

p.s: im using this thread now as a journal to see how i evolved in my investing process.

Investing Basics – Feel free to ask the most basic questions (25-12-2023)

OEMs are vehicle manufacturers including 2, 3 or 4 wheelers. Tata Motors, Maruti, Hero Moto Corp are examples.

Auto ancillaries sometimes known as Tier 1 companies are suppliers to the OEMs. Bosch, Motherson are examples.

Control Print – Deserves attention? (25-12-2023)

I still regret that I couldn’t add it more when it was 680. It is at only 2% of my PF currently.

IREDA: Renewable Energy Powerhouse (25-12-2023)

Based on 285 qtr of PAT in Q2FY24, annualized PAT = 4*285=1145 cr. On a loan book of 47 k cr , ROA is approximately 2.42%.

Investing Basics – Feel free to ask the most basic questions (25-12-2023)

When understanding Auto sector, I always have the doubt relating to OEM.

I was of view that OEMs are basically those company who make parts that is used in final product. As per that companies that make brakes, tyres, etc. are OEM.

However, when we search on google, it tells even Maruti, Tata Motors, Toyota are OEMs.

Can someone please provide more understanding on this? Thanks

Also, in case of auto industry, are OEMs and auto ancillaries means the same thing?

Selan Oil Exploration (25-12-2023)

Thank you for zoning in this very interesting slide. We were invested in Selan before Antelopus, so I happened have many investor presentations, including 2P of Selan’s portfolio before Antelopus. I opened one of them to see what the 2P numbers were on Bakhrol oilfield presented by Selan before Antelopus took over. I was curious because those numbers, I recalled from memory, were much hgher than the 1.77 mmbls above.

Can I ask you to take a guess on what they were? Were they higher or lower? If so, by what degree?

Some other points to note are that (a) currently Selan has performing wells, Antelopus portfolio does not, (b) we do not know the economics of drilling these new potential but unproducing wells whereas Selan was making good money; the Capex, PSCs and management plans (c) adding up 2P of Oil / Gas reserves and comparing the ratios of pre / post Antelopus Selan is quite erroneous, if you think about it.