Players like Radico had a realization per case of around Rs. 1600 in its P&A category in FY23. Assuming Rs. 400 EBITDA per bottle of Indri would be too high?

Posts in category Value Pickr

Petronet LNG Limited – Green India with Clean Fuel (23-12-2023)

Petronet LNG seems to be in the same boat like Coal India 2 years back.

Its dividend yield is improving since P/E and P/B are both contracting. ROE has improved marginally after 2020 & 2021.

Main concern seems to be their capex plans in Petro-chemicals (looks like diversification in unrelated area) and usage of EV going up in next few years.

Stock has not moved much after 2021, and could be the right candidate to move in next few years.

Lot of patience is needed here.

PLNG may increase their presence in EV charging space, but that may not add meaningful revenues in near term. So mainly stock can go up only if P/B reverts to Mean.

Continue to hold the stock as long as Dividend Yield is above 2-3%.

CGVAK Software & Exports Ltd – Niche Microcap IT (23-12-2023)

I had attended CG-VAK AGM23 conducted through VC, following are some notes. –

AGM23

-

Negligible revenue from ITeS, 98% from IT services

-

Focus in the areas of Mobile, digital transformation

-

36 new clients added during the year

-

US and Canada – majority business is from these geographies

-

Have clients in 10 more countries

-

Repeat business from same clients – 96%

-

43cr from NA, RoW – 11cr

-

Every year some award winning work is delivered by the company

-

There is feeling of slowdown – still looks like business as usual – there is cautiousness around decision making

-

Growth trajectory to continue

-

333 employees – 19 in US

-

Don’t create capacity until we have pipeline. Hoping to exit with 360-380 employees in Mar 24.

-

Should have started construction for new office. Pandemic changed way – everyone is yet to come back to office. Doing some groundwork. Won’t start construction until majority people are back.

-

Order book – 37cr

-

Sectors – Healthcare, retail, telecom

-

BFSI – some business

-

We are into niche market space where ticket sizes are small. These are small/medium businesses which biggies can’t service. Majority of these are owner managed businesses and have high expectations

-

Margins dropped due to cost of manpower

Disc – Invested, no transactions for several months, not a buy or sell reco.

The Anti-Portfolio (23-12-2023)

Hi,

I’ve been tracking Shilchar from 1200-1400 levels and has moved all the way upto 2800 levels. Just wanted to understand what is your thought process to add the stock when it’s 6-8x up already this year. Would love to understand your reasoning.

The Anti-Portfolio (23-12-2023)

(post deleted by author)

Gourab Paul EV Ecosystem India, 2023 (23-12-2023)

A recent idea that have come to @nirvana_laha and my notice as an ancillary play to EV batteries.

https://www.screener.in/company/HEG/consolidated/

Demand scenario of Lithium ion batteries

Conservatively Battery capacity required by 2030 is around 122 GWh – Source and Discussion with experts.

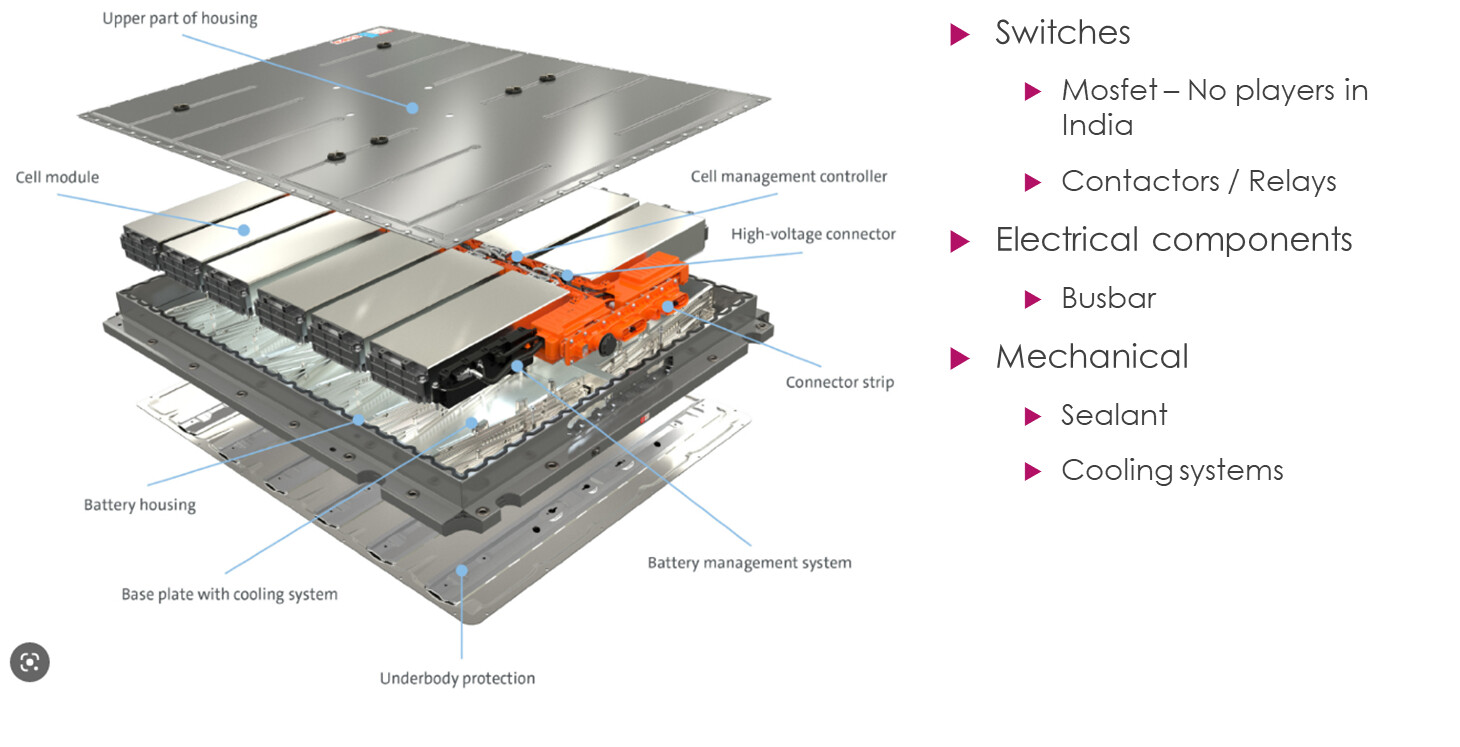

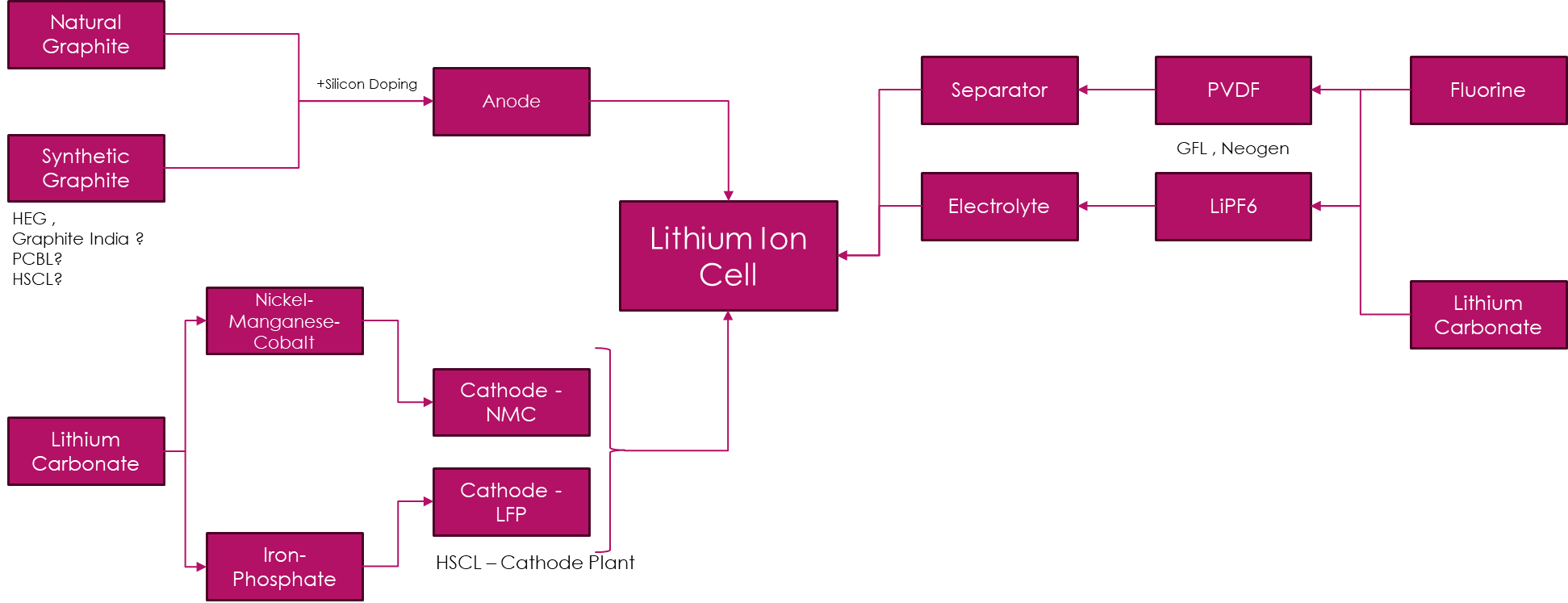

Major components of a Battery

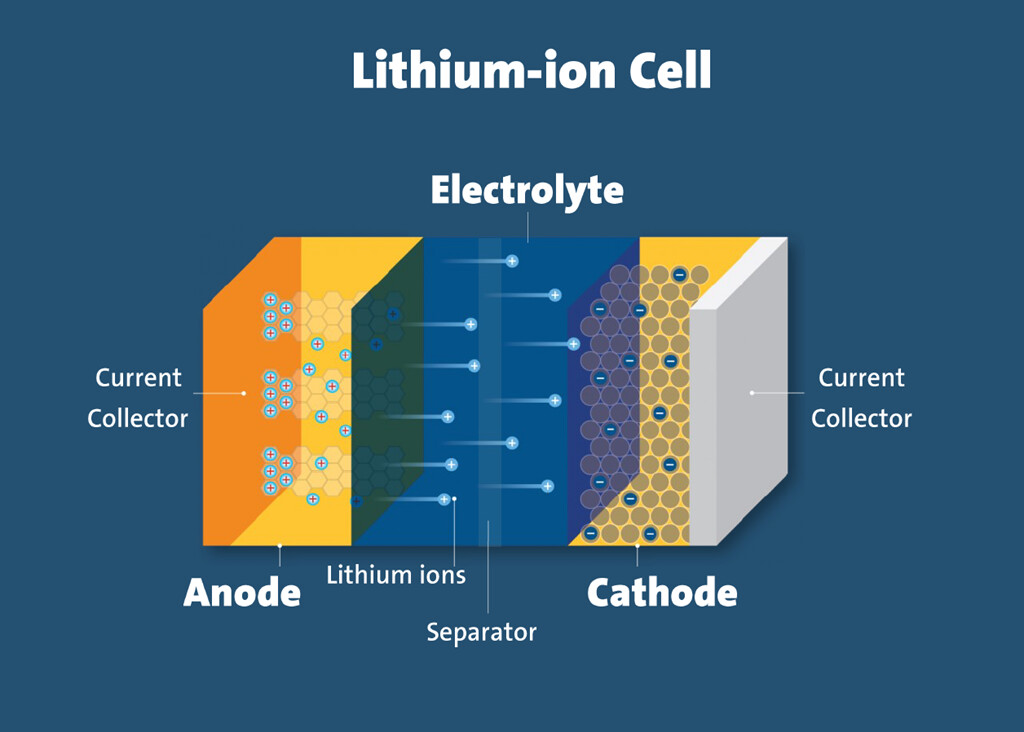

Major components of a lithium ion cell

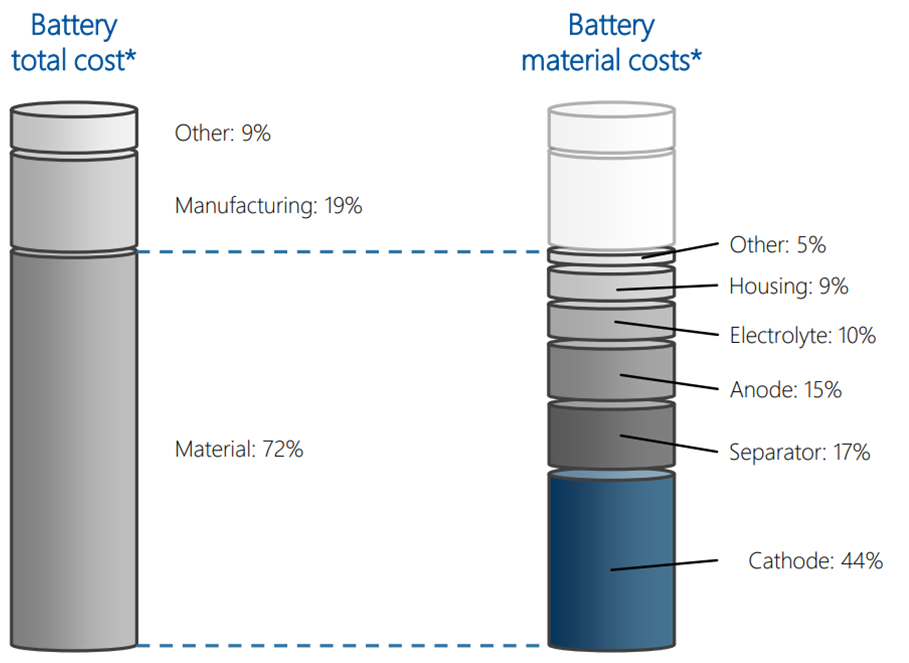

Approximate percentage of anode in a cell by cost source

the battery cell chemistry value chain

Conservatively = 122 GWh of lithium ion battery demand

1 GWh battery requires around 1000 tons of Graphite

Domestic demand by 2030 would be 1,22,000 tons at least. Globally much larger

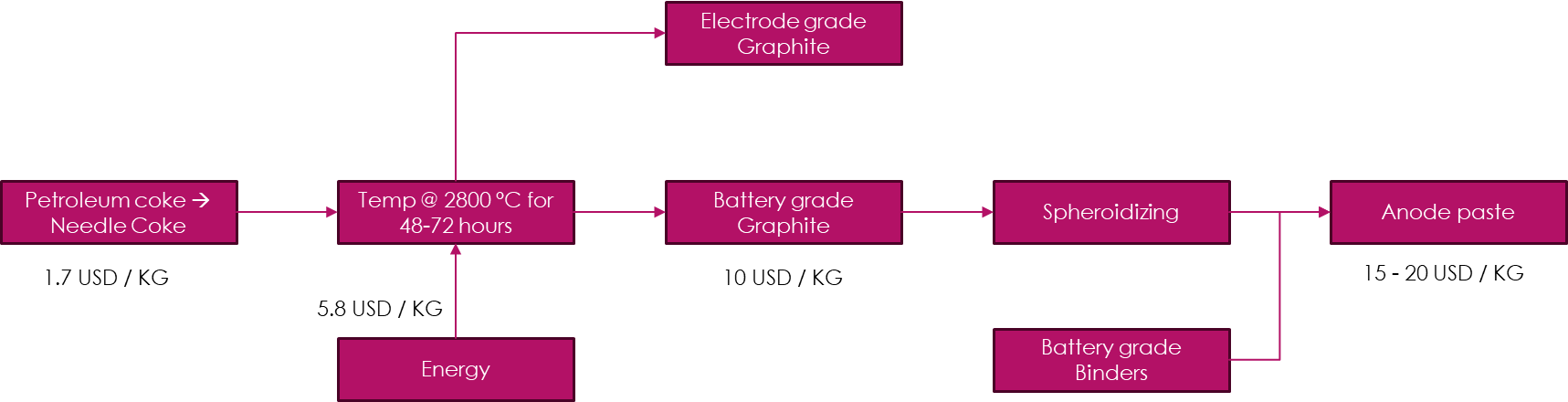

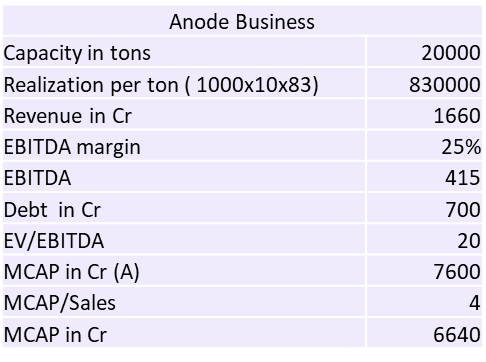

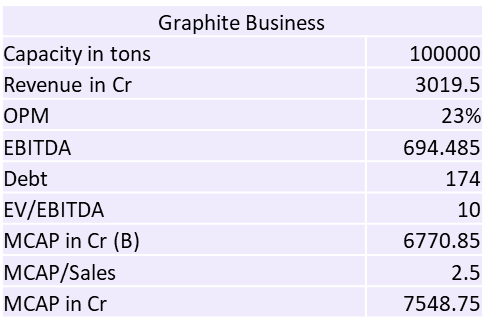

~40-50% of the cost is energy for anode production. HEG is the first company to invest in Capex under subsidiary TACC for 20000 tons by FY27.

HEG’s power cost is 5.5 rupees / Unit vs G.I ~ 8 rupees / unit, the management has claimed that they are the cheapest in the country and competitive with China

This is the cost structure, HEG’s new subsidy TACC will supply Battery grade Graphite

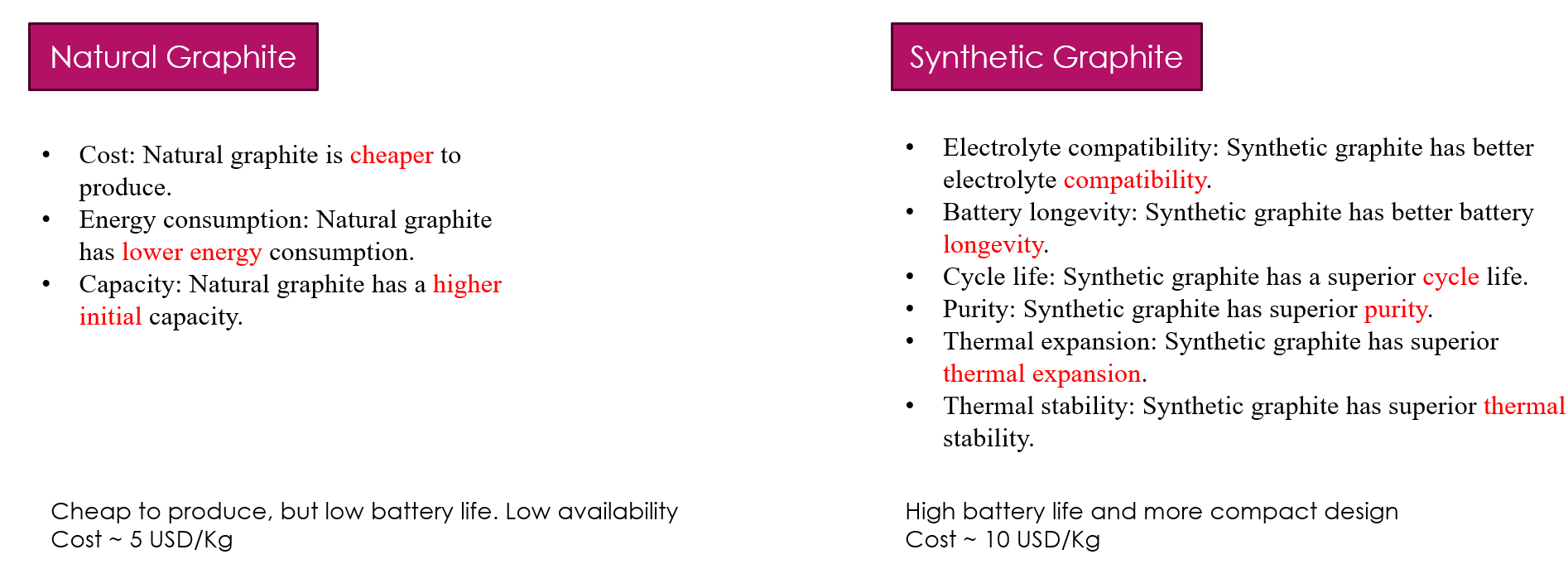

Synthetic graphite’s demand is rising as it can enhance life and fast charge applications. Most manufacturers will make synthetic graphite.

Upcoming trigger

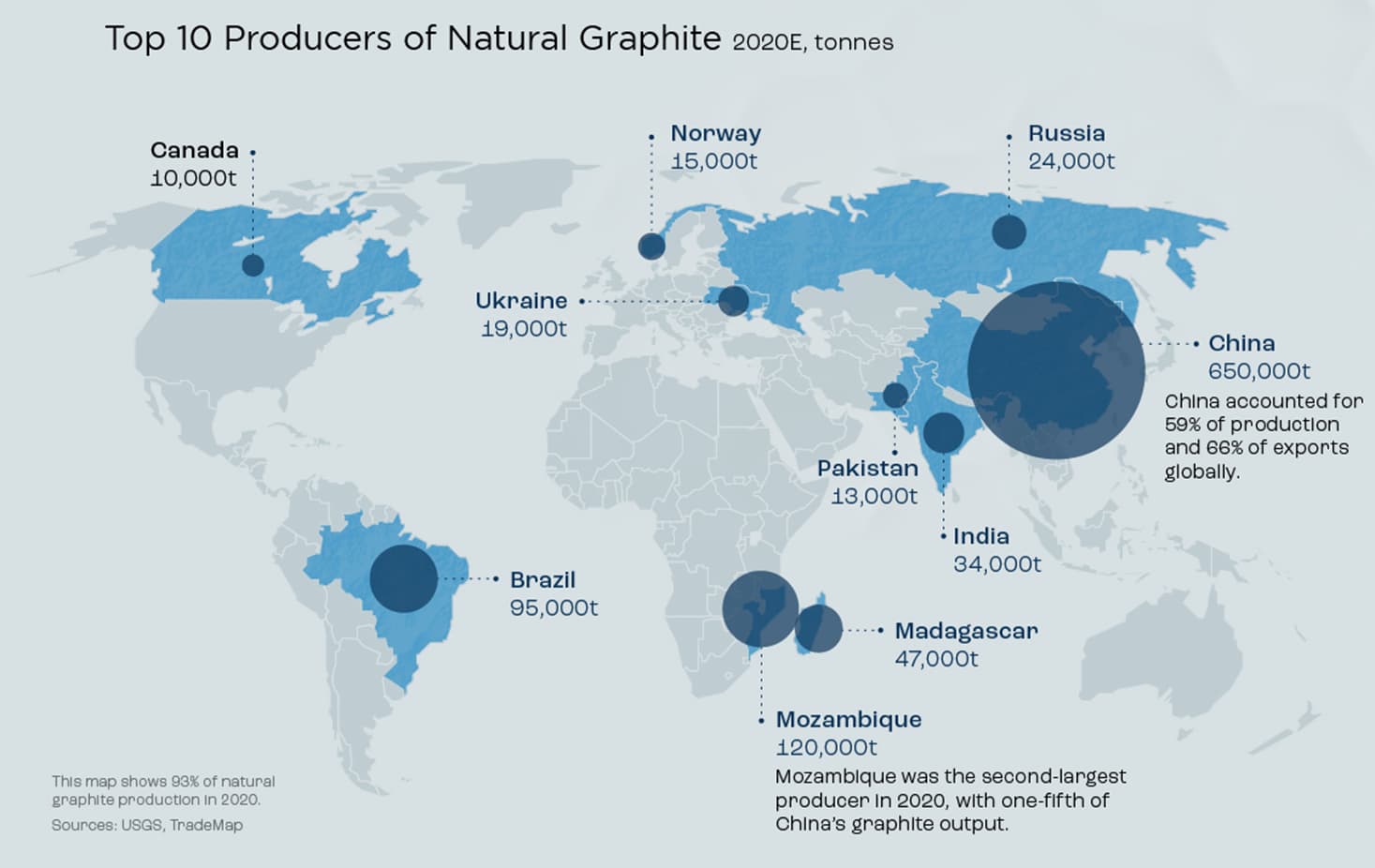

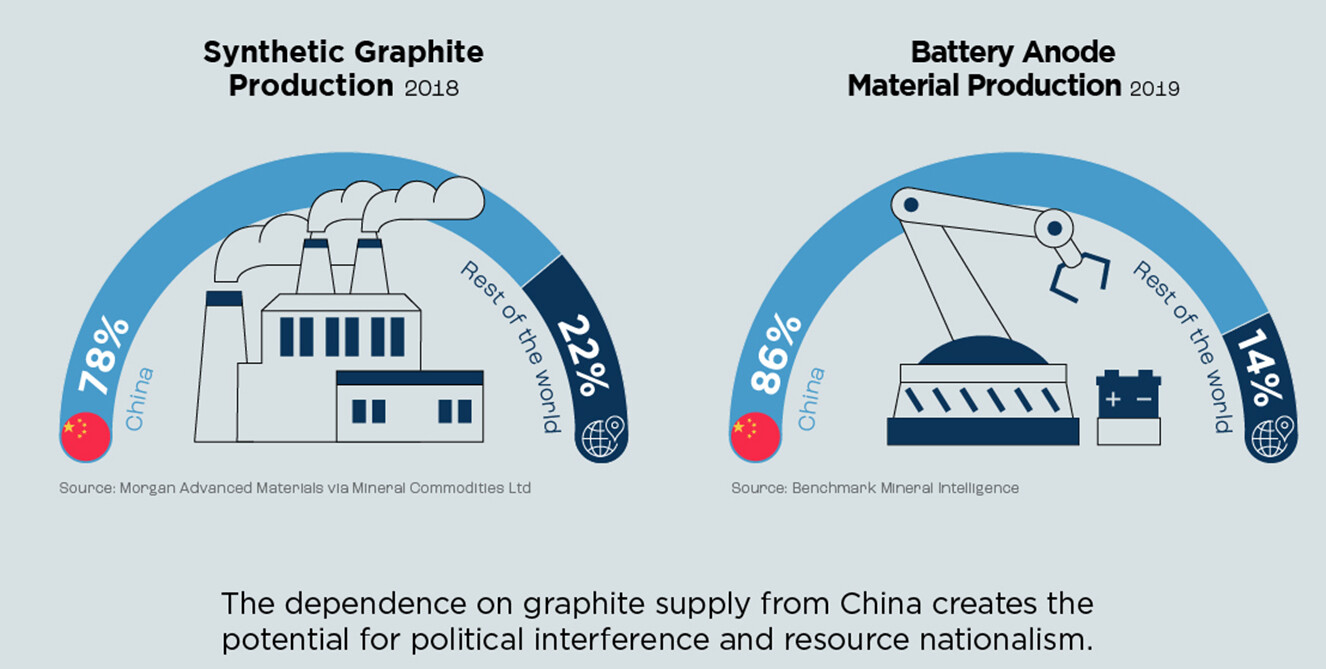

Chinese ban on Graphite export

China is a dominant graphite producer / refiner. The export curb would mean higher cost of Anode powder for rest of the world

Anode powder cost might rise to $14-15 for the rest of the world. Graphite will become a very strategic mineral.

Valuation by FY27

Note:

- Graphite powder will be used regardless we use Sodium ion, Lithium ion chemistries

- Silicon will not replace the traditional graphite anode before 2030. There is no commercial usage evidence [usage by Tesla, Merc, BYD ] other than company marketing

PEERS

Himadri Specialty Chemicals – Supplies to OLA on behalf of their JV partner, LFP play

PCBL – Not clear if they will venture into anode powder production, but management has indicated that they are definitely on the lookout for EV plays

Graphite India – Invested in some startups focused on silicon anode ( moonshot IMO)

Epsilon – Focus on US markets.

Disc: Invested and Biased. I am not a valuation expert.

Force Motors – racing ahead! (23-12-2023)

Force Motors Rating outlook revised to Positive; Ratings Reaffirmed

FM Rating Rationale.pdf (479.5 KB)

Key Points:

The Anti-Portfolio (23-12-2023)

Vikas, Any research around All-E tech? I know this was covered recently in IAS2020 but I didn’t subscribe to it.

I spent some time studying it but at surface I couldn’t find any moat that any run of the mill IT companies doesn’t have. My back of the envelope assessment of IT service companies goes like this. Calculate revenue per employee and see how they fair in comparison.

For All-E tech, 2023 revenue is 88 Cr for 331 employees (as per AR). This comes to 26 lakhs per employee. This is no different than others. In fact it is less than lot many mid size IT companies.

So why?

Gati – Long race horse? (23-12-2023)

Any idea what are these guys upto by doing all these corporate actions?