Anybody tracked this company? What are your thoughts?

Posts in category Value Pickr

Time technoplast (14-12-2023)

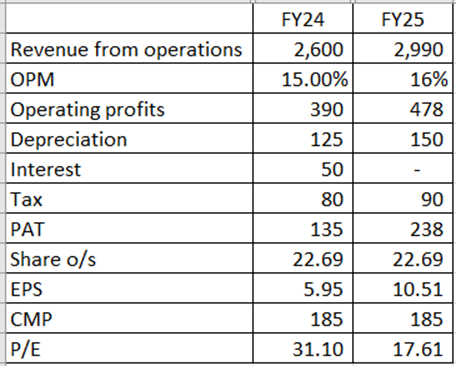

I don’t think “P/E of 16.5 X and an EV / EBIDTA of 7.7 X” is the right way to look at it. Since the company has already announced its plans to exit the overseas businesses, these investments should be looked upon as Assets Held For Sale. And so Time Technoplast should be valued on Standalone earnings, plus some value added for continuing subsidiaries such as TPL Plastech and the battery business.

Using Standalone earnings, a crude back-of-the-envelope calculation for FY24 suggests Time Technoplast may make something like Rs.2600 crore revenues and Rs.135 crore PAT, which gives an EPS of Rs.5.95 and a P/E of around 31 X. Benchmark P/E range for this group can be considered as 16 – 22 X based on where peer group companies trade.

The bigger jump in TTL’s numbers will come in FY25 when – if all goes as per plan – margins will improve further, debt can come down to zero or near zero and EPS can breach Rs. 10 plus. At this level, current P/E comes to 18 X which is in line with the sector benchmark.

Rough estimates (Standalone):

(Disc.: Holding)

Time technoplast (14-12-2023)

I don’t think “P/E of 16.5 X and an EV / EBIDTA of 7.7 X” is the right way to look at it. Since the company has already announced its plans to exit the overseas businesses, these investments should be looked upon as Assets Held For Sale. And so Time Technoplast should be valued on Standalone earnings, plus some value added for continuing subsidiaries such as TPL Plastech and the battery business.

Using Standalone earnings, a crude back-of-the-envelope calculation for FY24 suggests Time Technoplast may make something like Rs.2600 crore revenues and Rs.135 crore PAT, which gives an EPS of Rs.5.95 and a P/E of around 31 X. Benchmark P/E range for this group can be considered as 16 – 22 X based on where peer group companies trade.

The bigger jump in TTL’s numbers will come in FY25 when – if all goes as per plan – margins will improve further, debt can come down to zero or near zero and EPS can breach Rs. 10 plus. At this level, current P/E comes to 18 X which is in line with the sector benchmark.

Rough estimates (Standalone):

(Disc.: Holding)

SmallCap Hunter : Trying to find the dark horses with triggers (14-12-2023)

Infinium Pharmachem…New talk of town.

Pharma/API segment

Niche segment

Iodine derivative and related product…200+ products…7+API

Product used in most of industries including…pharma, chemical, cosmetics, agrochemical, electronics, rubber, dairy food product, oil & gas, medical, renewable energy…lots more.

Global presence 15 + country

Market cap ~340 Cr

Zero Debt

OPM ~14%

Topline/bottomline maintained

Healthy cash reserve

high promotor holding

Zero FII/DII

Suggestion and feedback required.

Disc…initial entry n planning to increase holding.

SmallCap Hunter : Trying to find the dark horses with triggers (14-12-2023)

Infinium Pharmachem…New talk of town.

Pharma/API segment

Niche segment

Iodine derivative and related product…200+ products…7+API

Product used in most of industries including…pharma, chemical, cosmetics, agrochemical, electronics, rubber, dairy food product, oil & gas, medical, renewable energy…lots more.

Global presence 15 + country

Market cap ~340 Cr

Zero Debt

OPM ~14%

Topline/bottomline maintained

Healthy cash reserve

high promotor holding

Zero FII/DII

Suggestion and feedback required.

Disc…initial entry n planning to increase holding.

Red Tape Ltd. – The next fashion giant? (14-12-2023)

ICICI Prudential Mutual Fund has added a further 7,60,100 shares of Redtape Ltd. during the month of November 2023. Mutual Funds are now holding about 6.85% stake in the Company.

Red Tape Ltd. – The next fashion giant? (14-12-2023)

ICICI Prudential Mutual Fund has added a further 7,60,100 shares of Redtape Ltd. during the month of November 2023. Mutual Funds are now holding about 6.85% stake in the Company.

ITC: “Will”(s) “Gold Flake” assist “Ashirwad” to win “Bingo!”? (14-12-2023)

BAT says cigarette brands to have finite life of around 30 years in US

How many years should we ascribe for India? Food, Hotels and Paper still constitute less than 20% profit if i am not wrong…

ITC: “Will”(s) “Gold Flake” assist “Ashirwad” to win “Bingo!”? (14-12-2023)

BAT says cigarette brands to have finite life of around 30 years in US

How many years should we ascribe for India? Food, Hotels and Paper still constitute less than 20% profit if i am not wrong…

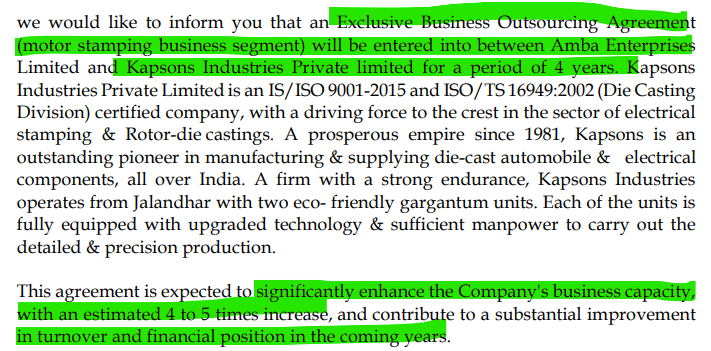

Amba Enterprises (14-12-2023)

Business Details:

- About company: It specializes in the manufacturing and trading of transformer lamination products and materials. With a foundation dating back to 1995, the company has established itself under the capable leadership of Mr Ketan Mehta, who has been at the helm since 2006. Mr. Mehta possesses extensive market knowledge and has a long-term vision for success.

The company operates two manufacturing facilities at Nanded in Pune, Maharashtra for the manufacturing of laminated steel cores. The production teams consist of qualified professionals with over 15-20 years of experience in this field, ensuring the delivery of exceptional quality products within specified timelines.

- Products Offering:

-

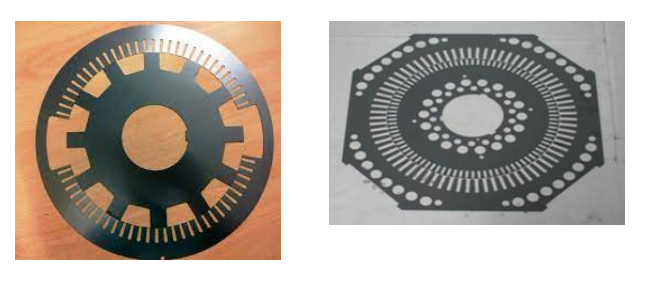

CRNO/ CRNGO Lamination Strips – It manufactures high-quality CRNO/CRNGO Lamination strips in various sizes. They offer these strips in a range of specifications and provide customization options to meet clients’ precise requirements.

-

Transformer Lamination – The company has a long-standing association in the market for this product. They are offering an extensive array of Transformer Laminations and strips.

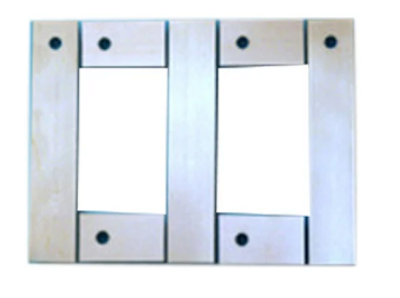

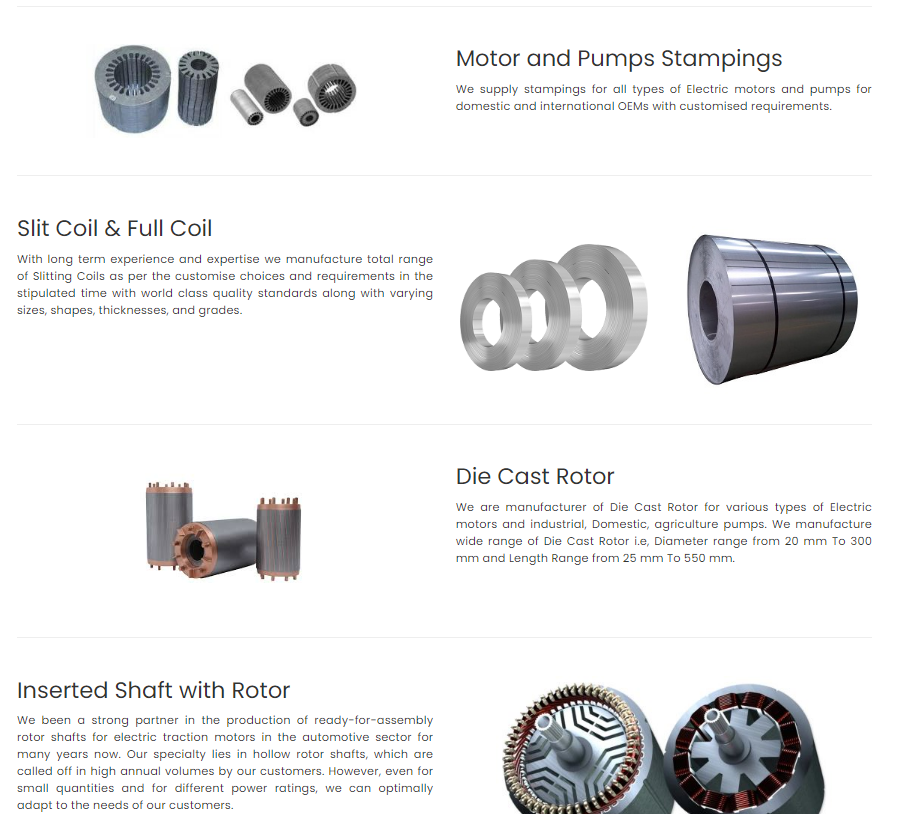

3. They also offer a diverse range of other products. These include Generator and Alternator Stampings, Motor and Pumps Stampings, Solid and Full Coil, Inserted Shaft with Rotor, and Die Cast Rotor.

- Application Industries : UPS, Transformers, Energy distribution, Automobile, Electrical equipment, Engineering and appliances, etc.

-

Clients:

Growth:

- Capex: AEL is planning to increase its production capacity at its plant in Kapsons, Jalandhar, Punjab by 4-5x.

- Opportunities: As per the recent disclosure, the company is also exploring new opportunities and conducting feasibility in new products and components in the EV sector.

- Clients Addition: The company is trying to add more customer base in FY23 – FY24. Negotiations with Havells are in initial stages and incremental revenue of almost INR 100cr+ is expected in the coming year.

- Revenue Guidance: The company is targeting a revenue of 550 Cr by 2025.

-

Outsourcing Agreement with Kapsons:

Industry Tailwind:

- The Indian Government has implemented various initiatives to foster the development of the domestic electronics manufacturing industry. Notably, the Make in India and Digital India initiatives have played a pivotal role in boosting the growth of domestic electronics production. As a result, the Indian Electronic Components Market has witnessed a significant expansion, increasing from $11 billion in FY 2009-10 to $20.8 billion in FY 2018-19 (excluding imported Printed Circuit Board assemblies). This represents a year-on-year growth rate of approximately 7%. These initiatives have been instrumental in promoting indigenous manufacturing capabilities and driving the growth of the electronics sector in India.

- India has set ambitious targets for the electronics manufacturing industry, aiming to achieve a manufacturing worth of $300 billion and exports worth $120 billion by FY 2026. These goals align with the broader vision of establishing a $1 trillion digital economy by 2025. According to the Economic survey, the key drivers fueling the growth in this industry include mobile phones, consumer electronics, and industrial electronics. These sectors are expected to contribute significantly to the expansion of the electronics manufacturing sector in India, driving economic development and creating employment opportunities.

- To establish India as a prominent global hub for Electronics System Design and Manufacturing (ESDM) and to advance the vision of the National Policy on Electronics (NPE) 2019, the government introduced three schemes in April 2020. The schemes include the Production Linked Incentive Scheme (PLI), the Scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS) and the Modified Electronics Manufacturing Clusters Scheme (EMC 2.0). These initiatives were launched with the aim of promoting domestic electronics manufacturing, attracting investments, and creating a favorable ecosystem for the growth of the ESDM sector in India.

- The current government with a view to boosting investments in railways, power plants, construction, housing and other industrial activities; since electrical steel is applied in diverse items viz. transformers, ballasts, motors, pumps, fans, windmill generators, and various other industrial purposes

Competitive Advantages and Intensity:

- Rejection Rate of the product: Amba Enterprises claims to have maintained a zero percent rejection rate and has not received any customer complaints to date. This achievement reflects the company’s unwavering dedication to providing superior products that meet the highest standards of quality and customer satisfaction.

- Highly experienced track record: AEL has a long track record of over two decades of operations in transformer core lamination activities.

- Long-Term Relationship: Over the years, the company has established long-term relationships with its customers and reputed suppliers.

- Quality Certifications:

Financials:

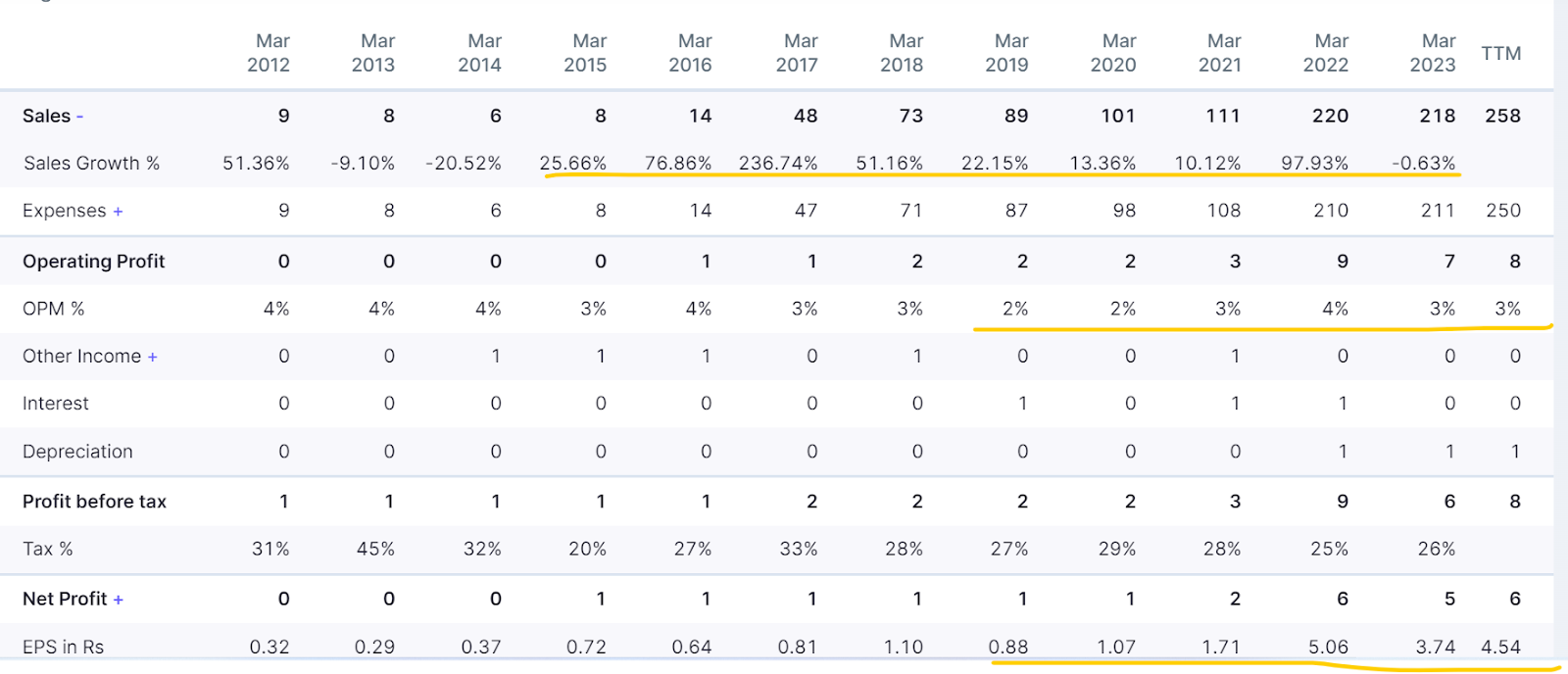

- Consistent Sales growth and Margin improvement: In the last 5 years ,it has grown at a cagr of 28% with improvement across margin from 2 to 4%.

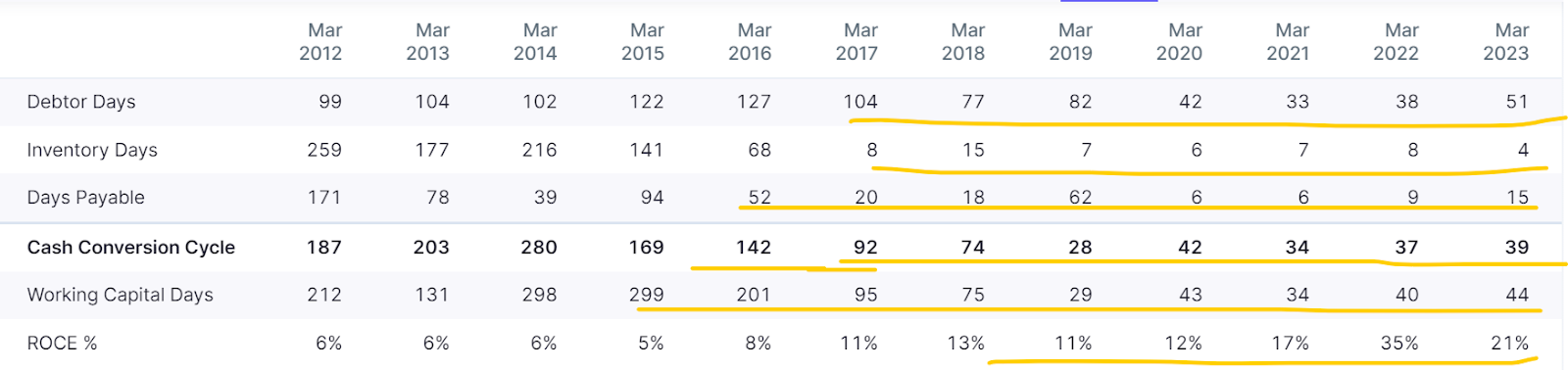

- Working Capital Management: There has been consistent improvement in debtors days, inventory days and days payable have increased.Along with this, we can see that the cash Conversion cycle has improved and company is managing the capital efficiently.

- Improving ROCE: Improving working capital has improved the ROCE from 6% to 21%.

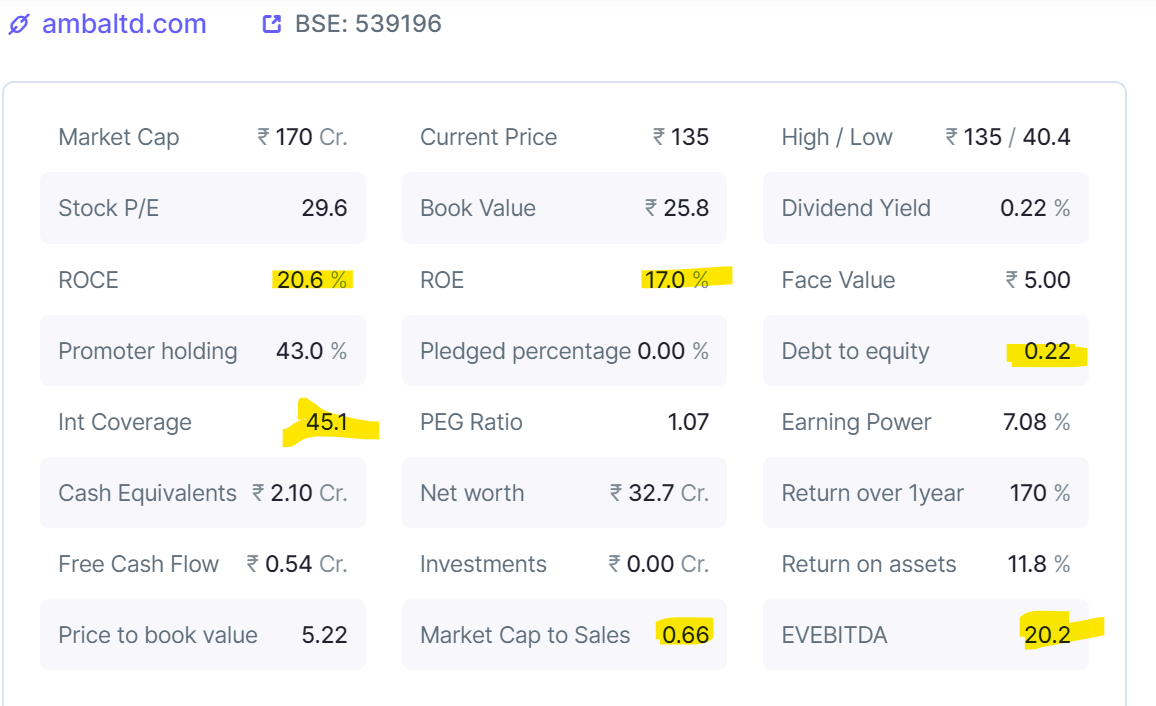

- Valuations: Checking Market cap to sales is still at 0.66x, looks attractive from 2-3 years perspective.

Risks:

- Competition: AEL operates in a competitive environment with a large no. of organized and unorganized steel players operating in the market

- Low Margin product: For the company, steel is the primary input material. Hence, any fluctuations in the steel prices would have a direct bearing on its turnover and profitability.

Management:

- Experienced promoter and a technocrat: The overall operations of AEL are looked after by Mr Ketan Mehta, who took over the charge of the company in 2006 as the MD. He possesses an extensive experience of over 25 years in the field of electrical steel stamping & lamination activities. Moreover, he is also assisted by the second line of management possessing relevant experience in the said field.

For more such companies, follow me on my blog or twitter.

Disclaimer: Invested and Biased