Position Type

Remote

Posts in category Value Pickr

HIRING: Research Apprentice (09-12-2023)

HIRING: Research Apprentice (09-12-2023)

interested but have an issue with location because currently I am in New Delhi.

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (09-12-2023)

Unable to read as I’m not a subscriber. Know of any trick to bypass the paywall? Or if possible you can share the text here

Yash Portfolio Feedback (09-12-2023)

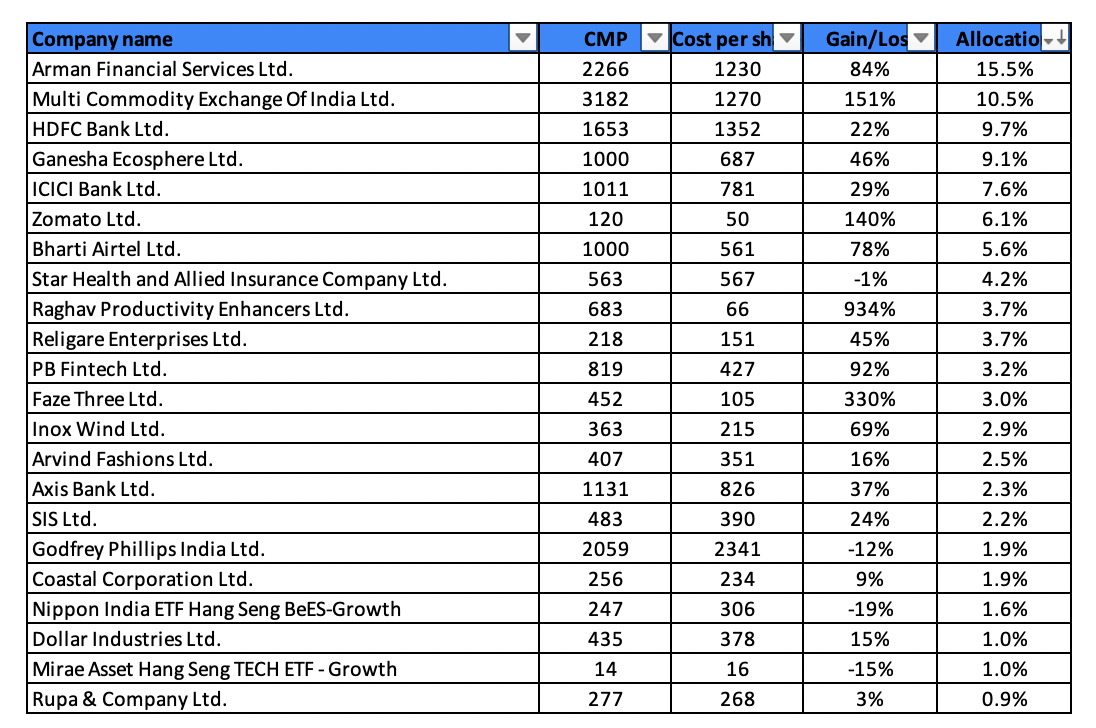

Been a busy few months. Definitely some froth in smallcap space; hard to find long term ideas where the risk-reward is better than the banks. Following changes made to the portfolio:

Additions:

-

Arvind Fashions: Bought this back post the Sephora sale and relatively splendid quarterly results (compared to peers). Same thesis as posted earlier in the thread Yash Portfolio Feedback – #16 by yrm91. 3 out of 5 brands that the company now operate are splendid and hugely profitable while the other 2 are a work-in-progress. Since the time I exited, the company has also done fantastic work on the Working Capital side. I expect 12-15% revenue growth here and think fair value is >2x P/S (even including minority stakes) vs 1.2x today.

-

Bought Inox Wind: Cyclical Turnaround bet. The wind energy has gone through a horrific 5-6 years which started with a few regulatory changes and aggressive bidding on the part of power developers. This has also led to industry consolidation; only those players who could support the companies could survive. Wind power capacity addition slowed from 4GW to <2GW over the last 5 years. In the recent past, govt has put more emphasis on the wind power sector. Number of initiatives such as 1) 10 GW annual project tendering commitments, 2) Pooled power tariffs, 3) Hybrid Policy & 4) Green Open Access are expected to lead to a revival of the industry. I expect capacity additions to grow 3-4x in the next 3 years. By FY27, Inox Wind could be executing ~1GW of projects annually. This would translate to revenues of 7500cr and EBITDA of ~1000 cr plus the stake in the asset light O&M subsidiary. These numbers could translate into a M.Cap of 20-30k cr by FY27 for the consol entity.

-

Added Godfrey Phillips: Credit @harsh.beria93 for this one. A low risk medium term opportunity. Company is a beneficiary of the Russia-Ukraine war which has re-oriented trade toward India. Bulk of the revenue growth of the company is due to exports which have scaled 3x in the last 2 years. Domestic high margin business has also recovered smartly from Covid. Good place to park money while I look for new ideas.

Sells:

- Indiamart: Was shocked at the supplier additions number in the quarter gone by. They were the result of both higher attrition and lower gross additions. The lower gross addition is especially concerning given the large investment the company made on the distribution side in the last 18 months. These could still be temporary aberrations based on recent prike hikes. However, I prefer to wait on the sidelines to confirm that. Long term value creation here has to come from volume growth and any data points that put a doubt to that is a big blow to the thesis. Supplier additions recovering to 5k would cause me to relook again.

General thoughts: A lot of positions are now starting to slip into sell territory on account of valuations where expected returns fall below 10%. These are Raghav Productivity, Faze Three, even Inox Wind and MCX post the large rallies. On the flipside I am struggling to find many pockets of opportunity other than the large banks. Rural economy related stocks is an area that I have started looking at. General pessimism can be seen here which is reflected in the stock prices. Inflationary pressures easing as well as election related short term income boost could see a rural recovery in the next year. Some bit can already be seen in rising 2W volumes. However, there are a lot of discretionary consumption stocks in this universe: underwear companies (already owned), apparel companies (VMart), rural focussed FMCG companies (Bajaj Consumer, Emami), tractor companies, etc that are available at reasonable valuations.

Ranvir’s Portfolio (09-12-2023)

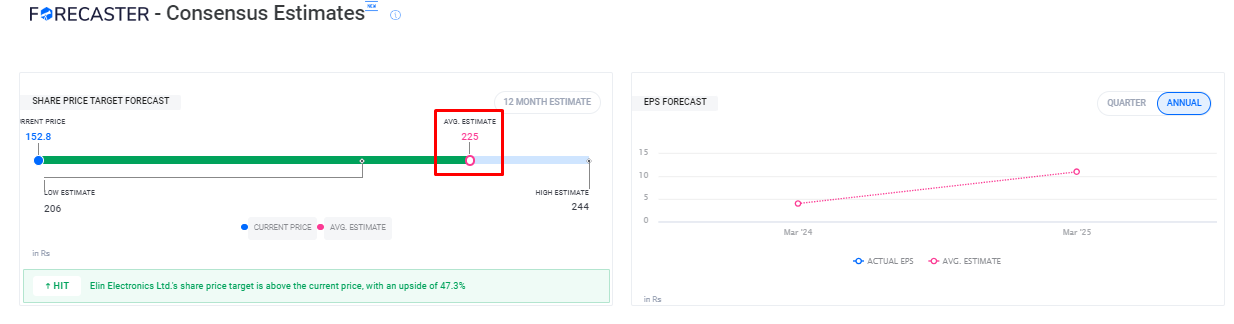

Hello Ranvir…above quote was, around end of October, related to elin electronics.

do you still hold Elin ? do you still hold the same views ?

If i remember correctly Elin’s Q2 results were due in Novmeber.

Further at below link certain broker has updated EPS.

Based on updated EPS, it still gives promising target.

What would you opine…ELIN has consolidated enough by now ?

D-Invested

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (09-12-2023)

Would love to see everyone’s comment on this

Praj Industries (09-12-2023)

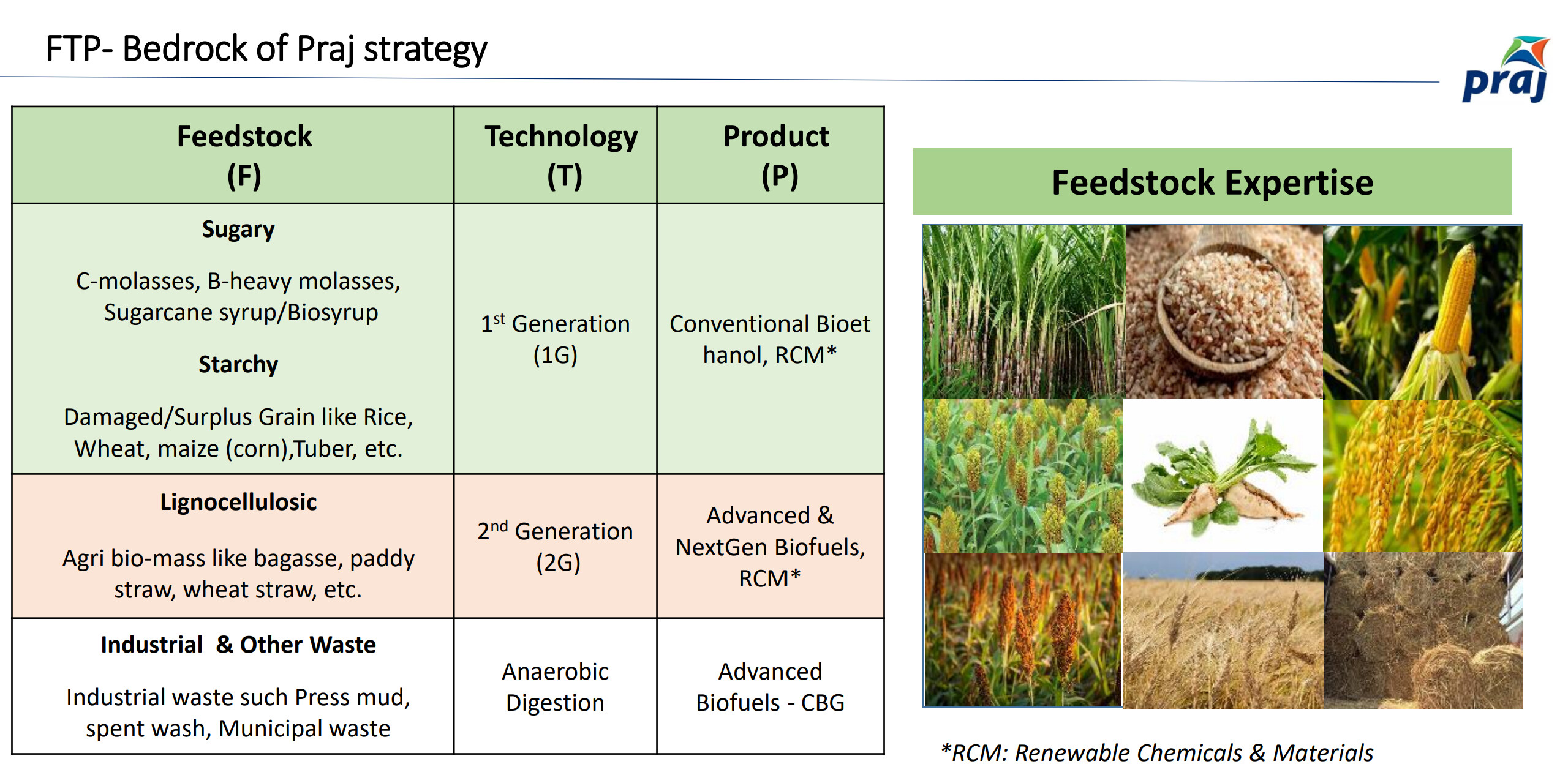

Let’s assess if the market’s – “The world has come to an end” reaction makes any sense.

From what I understand so far, the only thing that has changed for now is the source of ethanol, Praj is not a sugarcane producer it makes machines, machines to extract ethanol irrespective of the source. In fact, this might boost sales as grain-based ethanol producers will require more machines to fulfill the demand and to continue meeting E20 targets.

Borosil Limited (09-12-2023)

I can’t comment on the whether there is further price decline in store for BL or not, but happy to share the way I have done a quick back of the envelope assessment on what this means as an investment (I am assuming the split has been done in a rational manner and am not commenting on why the split is as is)

-

First the split in equity shares is reflective of the book value of the equity shares (and not the market value). I assume we should see this split when we see shareholder’s equity in the independent balance sheet of the two companies. Current book value is Rs 68.57.Based on this, the Price-Book ratio for these two companies are likely to be quite different given the different nature of businesses. Consumer durable companies seem to have a wide range on Price-Book – somewhere between 6-14 (Havells, TTK, Blue Star, La Opala). Based on the closing market price and the share of book value as per the split, this would result in a 9.6 price to book for BL (Consumerware business). For the Scientific business it is more difficult to find comparables – but seems to be somewhere between 2.5-4 (AGI Greenpac, Tarsons) which would imply somewhere around Rs 95 (this is the value of a share before the swap ratio – so not the expected listing price which needs to be adjusted upwards for the 3 shares of Scientific for every 4 shares of BL. So prima facie there does not seem to be crazy differences with the way the market has priced it

-

For my investment decision, though I would need to build a more detailed P&L / cash flow for each business – which will only be possible once they separate out the accounts – from which I could do a DCF / get a forward PE ratio. However, the company does share PBT numbers (as well as segment wise assets to do a rough forward PBT/PBT assessment) enabling a basic back of the envelope calculation. At a very rough FY24 PBT margin of 12% for Consumerware (assumes a significant improvement in 2H. Unfortunately 2H FY23 was a struggle due to lack of capacity on Larah so difficult to know long term PBT margin), the FY24 PE would be ~50. You can then form a view on whether this is high or low – given the comparables, stage of business they are in, etc. Similarly, assuming a 9% PBT margin for Scientifc for FY24 (which is much lower than long term margins as per management – investments in Technologies, Klasspack demand challenges) – it works out to a FY24 PE of ~40 for Scientific at Rs 95 (pre swap ratio) – which definitely feels high – but could be argued is expecting a turnaround as investments start benefiting the business

I am less concerned about fall in price of BL (there is a price at which it would start making sense to buy more) – but face a similar quandary to you in terms of what to do with Scientific. What seems to be transpiring is that Shreevar Kheruka will probably remain as the CEO of the Consumer Business as they have announced Vinayak Patankar as CEO of Scientific. However this is a whole other discussion if that is of interest.

Hope this helps. Happy to be corrected on methodology if I have got it wrong or other more appropriate approaches exist

Disc. Invested for a long time and likely to be biased. Not a registered advisor – the above is just my approach and not meant as advice

Real Estate (cycle) – Will pessimism give birth to multibaggers! (09-12-2023)

Thanks, But I wanted to ask how one can analyze the unsold inventory.

Eg: If the unsold inventory is high that means demand is less

or If the unsold inventory is high that means the company is ready with the inventory and in the next few quarters, we can see the numbers converted into the books of the company

Bajaar.me : Create customized screeners (09-12-2023)

I witnessed very good movement in stocks filtered out from your screener specifically in ‘Long Term Reversal’ and ‘Waiting for history to repeat’. Kindly let me know what is the criteria to add the stocks under ‘Waiting for history to repeat’ screener beside relative gains. Is there any fundamental reversal coming in these stocks or only technical reversal is seen? Further, kindly add the date of Long Term Reversal stocks, if possible so that early entry can be taken. However, you have provided a very good screener to the investors community. Thanks ![]()