Interesting article

However the same thought process a decade ago…

Doing the same thing and expecting different results?

Interesting article

However the same thought process a decade ago…

Doing the same thing and expecting different results?

This article is behind a paywall. Is there any discussion on inventory build up by market, at least for the large ones like MMR, NCR and Bangalore?

Here is an observation about Crisil’s cyclicality. Every few years Crisil’s PE re-rates to ~57 and then reverts to mean. We could be near the top of the cycle right now.

Disclosure: I hold shares. No transactions in recent 90 days. Not a recommendation.

Snapshot

About Company

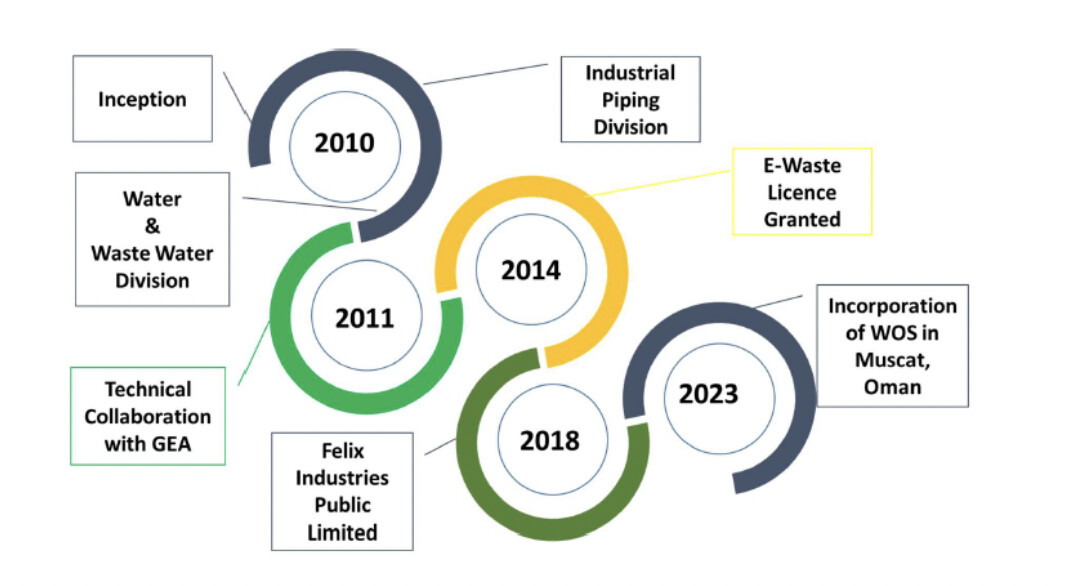

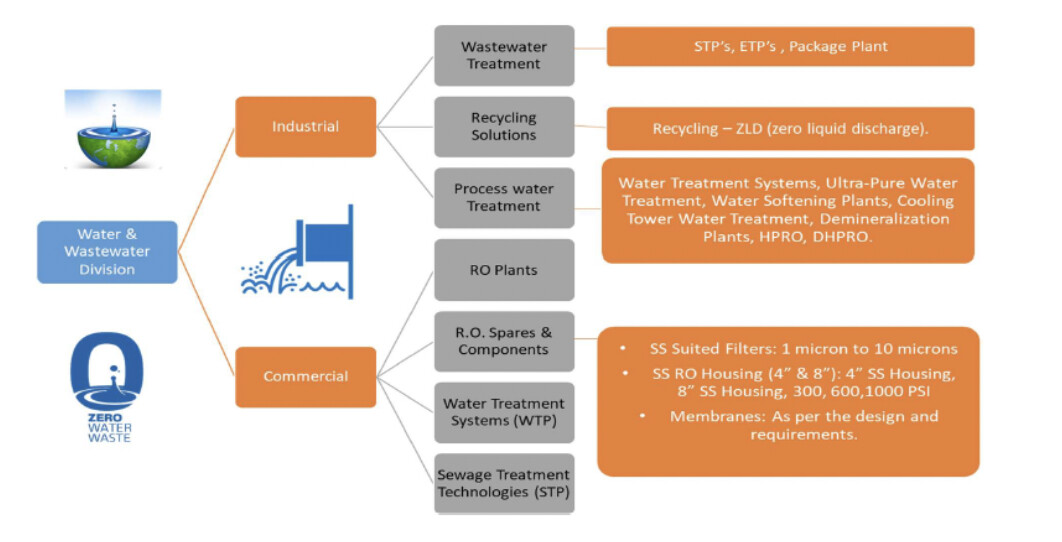

Felix Industries Private Limited, established in 2012 in Ahmedabad, Gujarat, is an environmental conservation company focused on “Recycle-Reuse-Recover-Reduce.” Led by Mr. Ritesh Vinay Patel and Mr. Sagar Samir Shah, it operates in sectors like Water and Waste Water Recycling, Industrial Piping, Nano Products, and E-waste Recycling.

The company provides water treatment solutions across various industries and is a significant player in industrial piping and e-waste recycling, with one of India’s largest processing capacities. As a government-approved e-waste handler, Felix manages all aspects of e-waste recycling at its Gandhinagar facility. The company aims to expand its reach in waste-water and e-waste recycling both domestically and internationally.

Product Portfolio

Water & Waste Water Engineering: The company specializes in Water Cycle Management Solutions. This encompasses the entire spectrum from producing and supplying drinking water to the collection, treatment, recovery, and recycling of wastewater.

Industrial Piping Division: This division is focused on Anti Corrosion and Thermoplastic Pipes, Fittings & Accessories. The products are manufactured by Astral Poly Technik Ltd and include a range of materials like C-PVC, U-PVC, PVDF, PP-H, HDPE.

E-waste Recycling: The company undertakes the management of e-waste throughout its entire life cycle. This includes activities from collection to recycling and material recovery, ensuring sustainable disposal and processing of electronic waste.

Spec-Chem Division: The company provides advanced solutions in the form of Nano Membrane Technologies. These technologies areinvolved in specialized chemical processes or treatments.

Clients

Management

Mr. Ritesh Vinay Patel: He is a Chemical Engineer with six years of experience in the Water & Waste Water Industry. His expertise includes project management, government approvals for water and waste water management, and business development in this sector.

Mr. Vinay Patel: Has over 40 years of experience in environmental work. He has been a Senior Administrator, handling environmental rules, research, and making sure industries and government reduce their impact on the environment. He has worked with the Gujarat Pollution Control Board (GPCB) and has experience in dealing with water and hazardous waste issues. His work has helped industries and the government follow environmental laws better. Mr. Patel has also worked on international and national projects in this field.

Mr. Sagar Samir Shah: Holding an MSc in Sustainable Waste Management, he has two years of entrepreneurial experience in the E-waste Industry. His skills include sustainability, strategic planning, finance management, and business leadership focused on waste and environment conservation.

Mrs. Shweta Samir Shah: She has a Bachelors of Commerce degree. Her experience and qualifications have not been specified beyond her academic degree.

Mr. Janesh Kundanlal Vyas: With a Bachelor of Engineering (Chemical) degree, he has over 30 years of experience in the Water and Chemical Industry. His areas of expertise include corporate and division management, business and market development, project and engineering management, and technology development.

Mr. Kashyap Hasmukhlal Shah: He holds an MSC in Applied Chemistry and an MBA in Marketing, with over 20 years of experience in the Chemicals sector. His experience extends to the manufacturing of basic metals and chemical products.

Mr. Raxesh Chandravandan Satia: With a Bachelor of Commerce degree, he has over 15 years of experience in the Textile Industry. His roles include directorships in various clubs and partnerships in business ventures.

Growth Triggers

Strengths

Recycling and Recovery Rates: Of the total e-waste generated, only about 12.5% (approximately 6.5 million tons) is officially documented and recycled to the highest standards. This low percentage indicates a significant gap in e-waste processing and recycling, representing a substantial opportunity for companies in this sector.

Regional Variability in Waste Management Systems: The effectiveness of e-waste management systems varies significantly by region. In India, where Felix Industries Limited operates, 65 cities generate more than 60% of the country’s e-waste, and ten states contribute 70% of it, with Maharashtra leading. Such specific data can guide strategic decisions regarding service locations and targeted marketing.

Potential for Innovation and Expansion: The need for tailored e-waste management systems in different regions opens avenues for innovative solutions. Felix Industries Limited can leverage this need to develop customized approaches, potentially expanding its services to various regions, especially within India where e-waste generation is significant.

Challenges

Working Capital Requirement: The company faces a significant risk due to its high dependency on working capital for daily operations. If it struggles to secure adequate working capital promptly and on favorable terms, there could be a detrimental impact on its operations, profitability, and growth. The risk intensifies if the company experiences insufficient cash flows, delays in funding, or challenges in obtaining funds from alternative sources under favorable conditions.

Accounts Receivable Cycle: The company’s long accounts receivable collection period increases its vulnerability to client credit risks and market fluctuations. This situation could lead to potential write-offs, increased provisions for receivables, and higher working capital needs, adversely affecting the company’s financial stability and operational results.

Regulatory Approval Risk for E-Waste Facility Relocation: The company’s expansion and relocation of its E-Waste facility hinges on securing necessary regulatory approvals. Any delay or failure in obtaining these permissions, particularly the Consent to Operate (CCA), could adversely impact the company’s business plans and financial stability, as part of its funding is dedicated to this project.

Customer Dependency: A substantial portion of the company’s income is derived from a limited number of large clients, with the top five clients being particularly significant. This client concentration poses a risk, as their decisions, influenced by factors beyond the company’s control such as management changes, mergers, economic shifts, or government funding variations, could impact the business.

Recent Updates

30st Oct 2023: The company has entered into a Joint Venture Agreement (JVA) with Mr. Divyanshu Varma to form a new Joint Venture Company (JVC) named M/s. Rivita Solutions Private Limited. Felix acquired 50% stake in JV company.

8th Nov 2023: The company has acquired an additional 1% stake in M/s. Rivita Solutions Private Limited, a JV Company, in accordance with the conditions set by ONGC for bidding in a project. The total stake now is 51%.

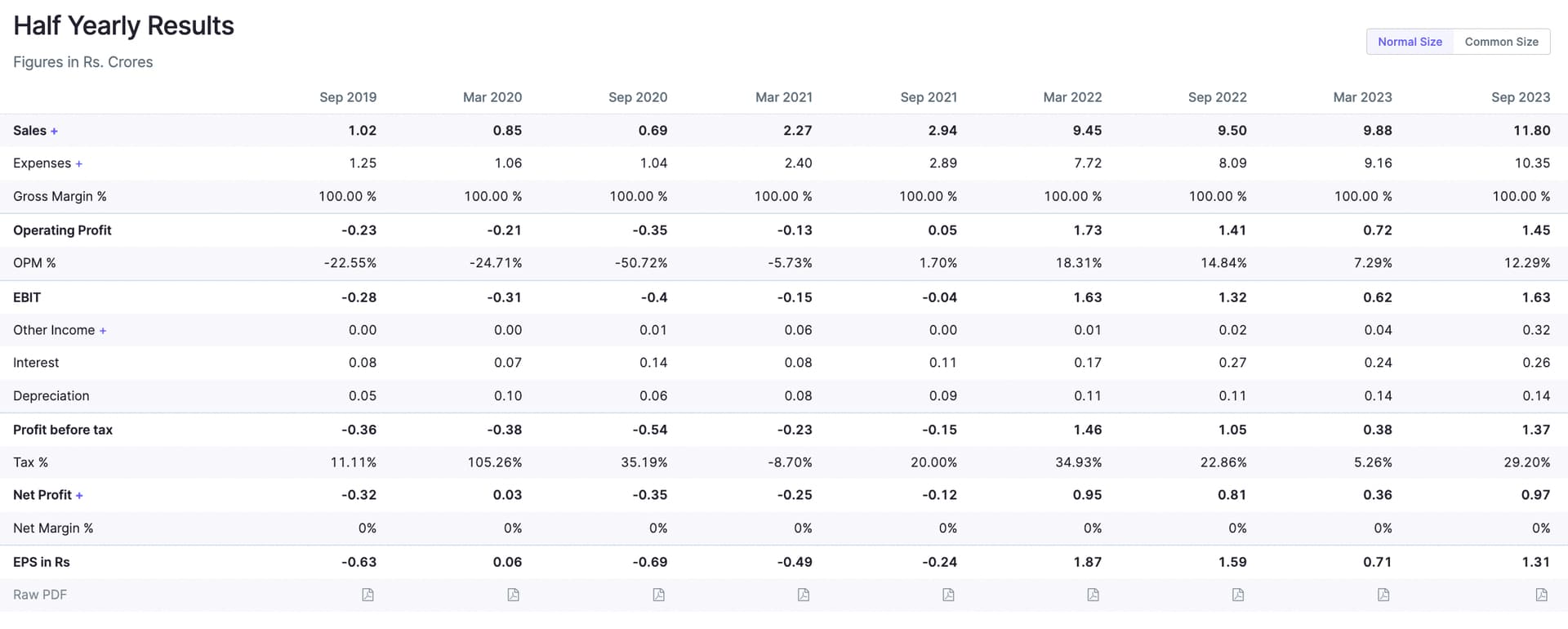

For H1FY24,

Sales were up 11.8 cr in Sept 2023 v/s 9.5 cr in Sept 2022.

OPM contracted from 14.84% to 12.29% during the same period.

EBIT increased from 1.32 Cr to 1.63 Cr during the same period.

PAT was up from .81 Cr to .97 Cr, however EPS contracted from 1.59 to 1.31 during the same period.

Both the Sales and Profit have grown north of 25% over the last 5 years.

Total Addressable Market

India water and wastewater treatment market size was estimated at USD 1.56 billion in 2022. During the forecast period between 2023 and 2029, the size of India water and wastewater treatment market is projected to grow at a CAGR of 10.05% reaching a value of USD 3.03 billion by 2029.

It seems like an interesting idea to study if the mgmt can walk the talk.

Disclosures & Disclaimers

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.”

“Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.”

“The securities quoted are for illustration only and are not recommendatory.”

“I did not trade in any of the companies mentioned in my post thirty days before its release. Neither do I intend to take any positions in the companies mentioned in this post during the subsequent five trading days.”

“This should not be construed as a recommendation to buy or sell securities or be considered investment advice or a research report.”

“Before making any investment decisions about the companies mentioned, investors must consult with their investment advisor or undertake due diligence on their own accord. I do not assume any responsibility for any financial gains or losses that may result from any investments made based on the information contained herein.”

“All information presented is already public and errors may happen because of human oversight.”

Ayush Agrawal

Research Analyst

SEBI Registration No. INH000013013

First Floor, B.P. Complex, Baldeobagh, Jabalpur, Madhya Pradesh, 482002

Email: themicrocapinvestor@gmail.com

Number: +91 9425412028

I was relooking at my thesis in light of the market correction, and I am not very concerned.

IMO ‘Banking for the unbanked’ may only be a market entry strategy, as they are super keen on retaining acquired customers even at low-interest rates.

I won’t be surprised if, in a few quarters, they operate like any other HFC, which may mean lower margins for high-quality customers.

Next steps: Convinced on the macro story. Have to build conviction from a customer’s POV which is a little difficult given that Aavas primarily operates in Tier-2 cities (If anyone has advice here, I will owe you one!)

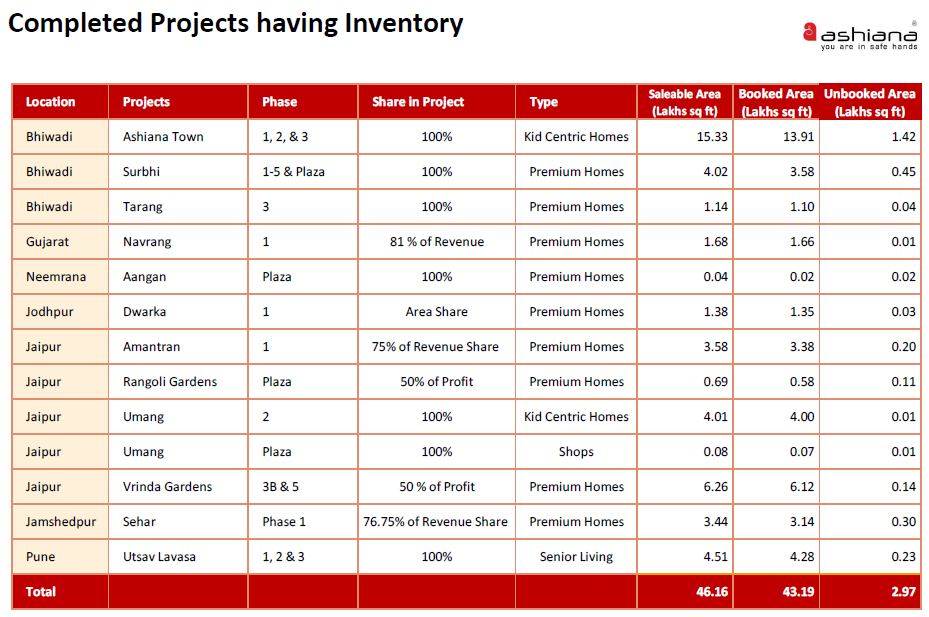

Unsold Inventory in generally reported in the Earnings Presentation. Below is the snippet from Ashiana Housing’s ppt. If you track the numbers Q-on-Q, you will be able to determine the increase and decrease.

How can one view the increase in the inventory level of the company?

Hi Value Pickr

Took a break from the log because of bad health. Will come back tomorrow with an improved entry ![]()

Borosil Q2 FY24 concall notes:

Before getting into concall details it’s important to understand various verticals in the business of Borosil limited:

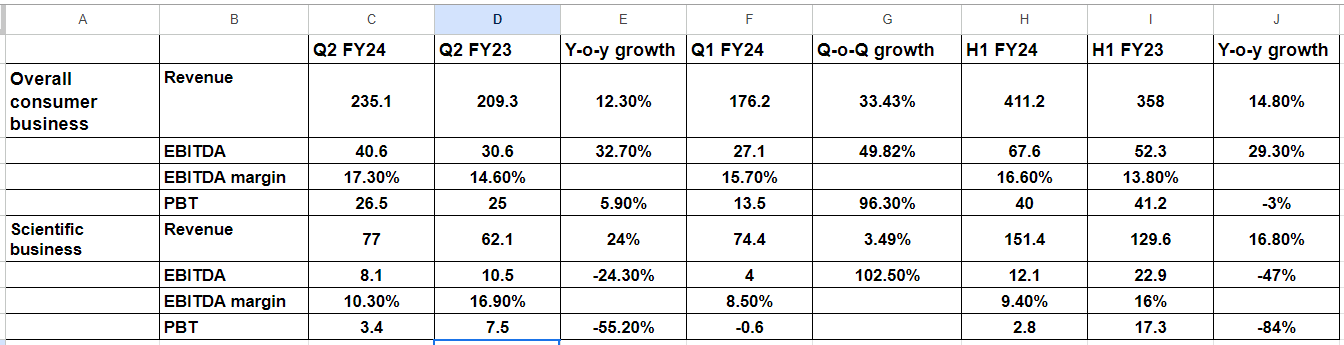

Financials

Segment wise revenue:

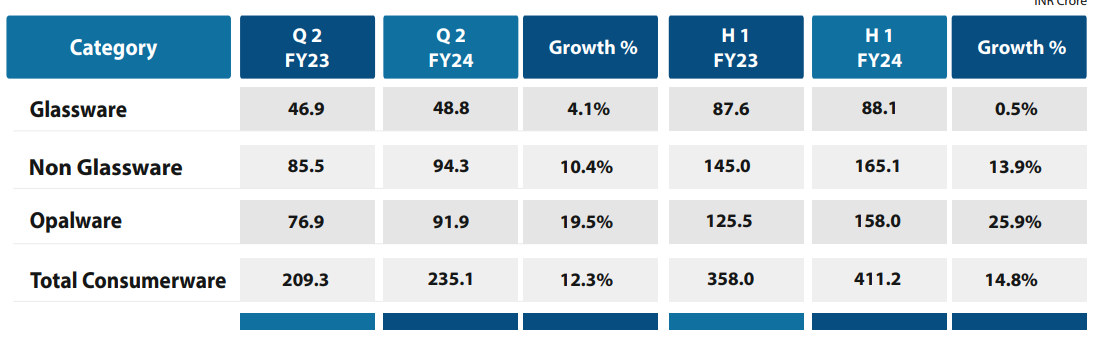

Consumer business updates:

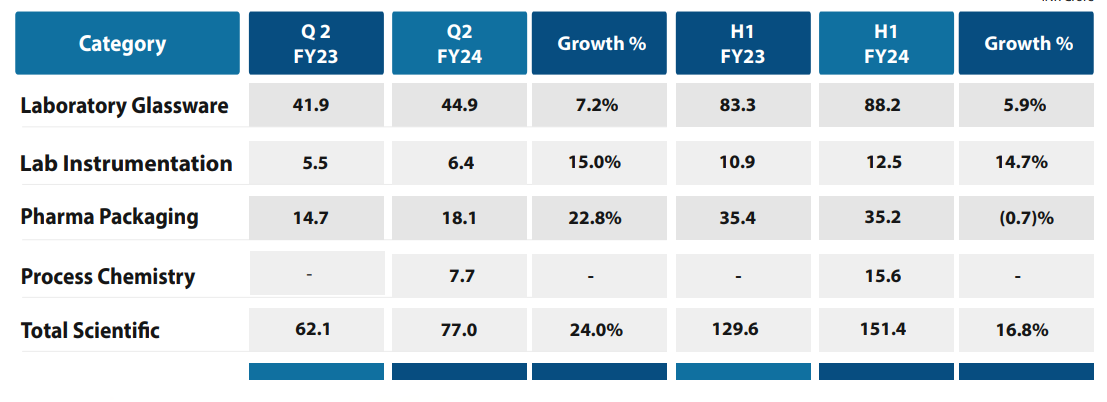

Scientific business updates:

EBITDA margins: H1FY24 9.4% vs H1FY23 16%. This is due to losses in Labquest & Goel scientific.

Klasspack: Domestic sales are not good, export sales looking good. Two domestic customers had challenges. Lot of capex has been done in this segment but the capacities are very low at this point of time (around 40%). Lat 1.5 to 2 years are on a rough patch, focus is to improve on this to a state where they were 1.5 years back.

Goes scientific: Business acquired around early May. Ramping up on the process and expects another six months for the complete ramp up to align this with the Borosil setup. Focus is to expand the sales from this vertical (south India – no sales team, Hyderabad is a big market). Margin profile should be on a similar range as lab glassware vertical, but this is going to happen once the sales potential reaches.

Tubing facility capex is deferred by a year.

Other updates:

What to look for in coming quarters?

References:

Overall I feel consumer business continues to do well with improvement in margins, whereas scientific business is facing headwinds and needs to be observed how management can sail this and turn around this vertical.

Disclosure: Currently forms about 3.5% of the portfolio. Might sell scientific business after listing and convert the same to consumer business.

I was replying to a thread elsewhere and I realized that when you invest direct, you not only have to beat the index, but you also have to outperform an active mutual fund.

Of course, the learning, excitement and joy of doing direct is still a bonus.

Also came across this: