Borosil Q2 FY24 concall notes:

Before getting into concall details it’s important to understand various verticals in the business of Borosil limited:

- What I like about Borosil is, Shreveer Kherukha gives a very detailed update on all the verticals in his opening remarks and spends almost 15-20 minutes giving the overall update about the business. (+1 here for the management style).

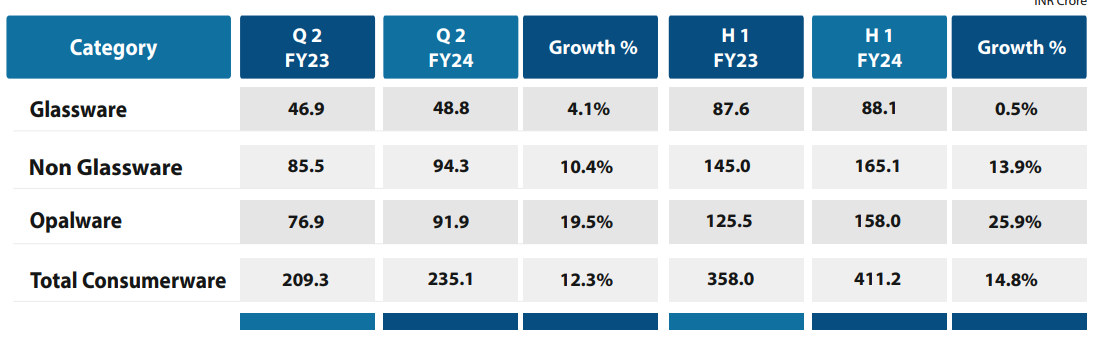

- Consumer business

- Glassware

- Non glassware

- Opalware under Larah

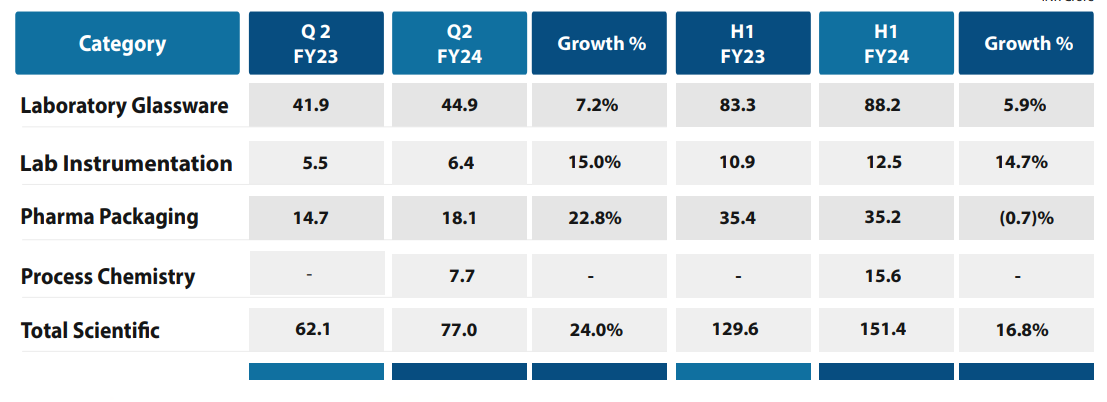

- Scientific business

- Laboratory glassware

- Laboratory instrumentation under Labquest

- Pharma packaging under Klasspack

- Process chemistry under Goel scientific (recently acquired)

- Scientific business will be demerged and will be renamed as Borosil Scientific Limited, 3 shares of scientific limited will be given for 4 shares of holding Borosil limited. Ex spin off date is 12/5/2023.

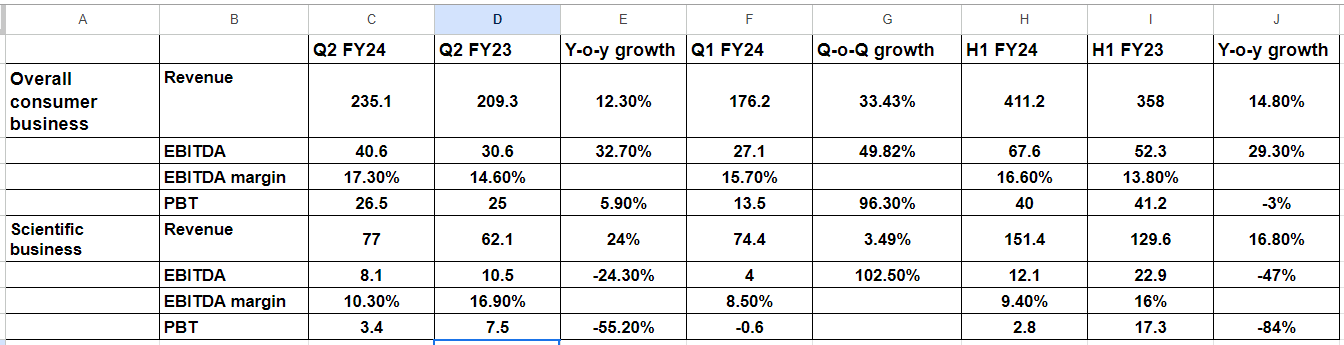

Financials

Segment wise revenue:

- Lower EBITDA in H1 is due to the account of following:

- Last year there was an exceptional gain of 5.1 crores due to insurance claims.

- This year there is one time expense of 2.8 crores towards the acquisition expenses.

- Lower profit is on account of:

- Higher depreciation to the tune of 20 crores due to the opalware furnace plant opening at Jaipur plant.

- Also the income from investments is lower by 2.8 crores this year compared to last year.

Consumer business updates:

- Opal ware capacity is running at 75-80% utilization, this is after upgrading the capacity to 84 tons per day from the previous 42 tons per day. Management expects increase in profitability with the 20% remaining sales, and expects to reach 100% capacity in fy25.

- Good growth seen across all ranges and channels (trade or large format retail). Several new products have been launched in the recent past. Roughly 20-30 new designs are launched every 6 months.

- Borosilicate presswork capacity of 25 tons per day will commence from Q4 fy24. Maximum capacity they can make it to is 42 tons per day in the same plant. Any new capacity be it opal ware or other things should be coming in a location.

- EBITDA margins should increase due to the operating leverage getting kicked in. H1-24 16.6% vs H1-23 13.8%.

- No capex planned for FY25, only maintenance capex.

- Diwali sales are neutral, that is nothing too exciting nor depressing.

- 10-15% of sales are coming from exports, focus is on domestic business now as realizations are higher.

- Current debt is about 215 crores and most of it is on consumer business.

Scientific business updates:

-

EBITDA margins: H1FY24 9.4% vs H1FY23 16%. This is due to losses in Labquest & Goel scientific.

- In labquest there are upfront costs for growing the technical team and R & D expenses are more than proportionate than the increase in revenues. Management expects this to take 2 years to normalize. The expenditure here is on people which needs to be upfront, once they become experts and deliver with the knowledge they gained over initial periods margins will start expanding. There is no gross block like consumer division here and is the reason for attractive return on capital.

- Goel scientific: this is due lower sales & higher fixed costs. Management expects this to stabilize once the synergies are put into place.

- Klasspack: Again due to lower sales(lower pharma packaging demand) & increased direct costs could not be passed on to customers. Things are improving in Q2 & should be even better in Q3.

-

Klasspack: Domestic sales are not good, export sales looking good. Two domestic customers had challenges. Lot of capex has been done in this segment but the capacities are very low at this point of time (around 40%). Lat 1.5 to 2 years are on a rough patch, focus is to improve on this to a state where they were 1.5 years back.

-

Goes scientific: Business acquired around early May. Ramping up on the process and expects another six months for the complete ramp up to align this with the Borosil setup. Focus is to expand the sales from this vertical (south India – no sales team, Hyderabad is a big market). Margin profile should be on a similar range as lab glassware vertical, but this is going to happen once the sales potential reaches.

- Acquired with a cost of around 50 crores, current capacity can do 100 crores of sales. Current sales are at around 50 crores.

-

Tubing facility capex is deferred by a year.

Other updates:

- Company spending around 40cr to set up a 6.5 megawatt solar project in Rajasthan, this should help save about 6-7cr of power cost per year.

- Tax rate for this & next year will be 25%.

What to look for in coming quarters?

- What kind of valuations Borosil limited and Scientific Limited shares get traded after the demerger?

- Margin expansion in the consumer business. Already improvement seen, should continue to improve further.

- Keep an eye on scientific limited business performance. Margins took a hit recently.

References:

- Q2 FY24 results: https://www.bseindia.com/xml-data/corpfiling/AttachHis/5759bd6c-6fac-4c14-9ed6-9ca15c7e958e.pdf

- Conall transcript: https://www.bseindia.com/xml-data/corpfiling/AttachHis/f7a1948c-bb4c-4a95-ac5c-599efe46033e.pdf

- Presentation : https://www.bseindia.com/xml-data/corpfiling/AttachHis/f58f2fd7-89f9-452f-95cb-3228761f3d1d.pdf

Overall I feel consumer business continues to do well with improvement in margins, whereas scientific business is facing headwinds and needs to be observed how management can sail this and turn around this vertical.

Disclosure: Currently forms about 3.5% of the portfolio. Might sell scientific business after listing and convert the same to consumer business.

| Subscribe To Our Free Newsletter |