Thanks for sharing

Kovai’s PAT margin should be better in FY25 with better margin from Education segment & peaked out depreciation.

NH is interesting with prespective of health insurance integration.

Thanks for sharing

Kovai’s PAT margin should be better in FY25 with better margin from Education segment & peaked out depreciation.

NH is interesting with prespective of health insurance integration.

Plus, after October lot size being reduced. I understand that main board would happen sometime after that. Real price discovery would perhaps happen on main board.

did any1 attend the agm ? If yes can you pls share the notes

Agree… sector is right… but many such equity buy/sell transactions being done to favor promoters… these transactions are as per the SEBI guidelines of pricing etc… but current valuation is too high. investors coming in now… will surely be at risk of loss…

Looking at trailing might not be ideal in this business in particular. They have had a very bad FY24 due to multiple reasons and lead to abnormal PAT and PAT margins. Earnings were depressed. If you get a good sense on the forward numbers and estimates, valuations are still inexpensive. I dont know exactly what the FDC forward numbers would be like, but my sense is that the forward PE for Jagsonpal is still low compared to peers.

Yes, pls send me a direct message as we won’t like to crowd this thread with my rant ![]()

My investment philosophy prioritizes quality, resilience and longevity of a business with strong management at helm. So if a certain business or company doesn’t pass that filter, I don’t look any further. So in that respect I can’t comment on numbers you have posted as I don’t track or research this sector.

Hi All,

New to this forum and relatively new to the investing world (I began actively investing around June-2021). Over the last 3.5 years, by reading books, annual reports, and multiple other public documents and material, I’ve been trying to sharpen my investment thesis. Posting it below for feedback and comments:

Goal: Which company to invest in and why?

Thesis:

Financial Robustness

• Debt = 0

• Interest Coverage > 10

• ROCE (EBIT/(NWC+NFA)) > 25%

• Revenue Growth CAGR over last 5 years > 15%

• PAT Growth CAGR over last 5 years > 15%

•Average OPM over last 5 years > 10%

•Cumulative FCF over last 7 years > 0

•Cumulative OCF over last 7 years > 0

•Inventory Days < 90

•Receivables Days < 90

•Cumulative PAT over last 7 years =~ Cumulative OCF over last 7 years

Business Metrics

• Is it a monopoly/Oligopoly/Duopoly?

• Market share in industry? Is it growing?

• Does the company have pricing power?

• Is pricing regulated by the government?

• Is the volume growing over time?

• A qualitative aspect of volume growth over time? New markets? New products? New customer segment? Change in product lineup?

• Does it have enough capacity to meet the increasing volume?

General Metrics

• Age of company in the public markets

• Management Quality

• Reputation among stakeholders (customers, suppliers, employees, shareholders, partners)

Industry Metrics

• TAM (Global, Local)

• Industry Growth Rate

• Convergence Pattern among players in Industry

• Customer Power/Fragmentation

• Supplier Power/Fragmentation

• Competition in Industry

• Threat of new entrants

Strategy Metrics

• Is it a turnaround situation?

• Is it an M&A Junkie?

• What is the company moat? What is its competitive advantage?

• How is it allocating capital?

• How much is annual Capex spend? As % of revenue?

• What is the growth strategy? What is the sustain strategy? Are both sustainable?

• Is it a volume play or a value play (Mass vs Luxury)?

Valuation Metrics

• Average PE Ratio over last 5 years < 30

• Current PE Ratio < 30

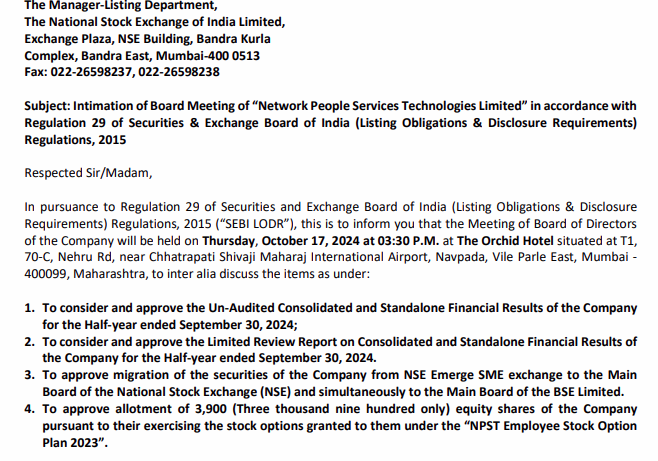

Likely to move to the NSE and BSE mainboard soon

I had gone through this transcript, What I believe is margin% should not fall but declining or rising steel prices can lead to a change in absolute revenue and profit number.

In fact, I think the clarification is an indeed an acceptance that the media numbers reported did indeed take place, just that the numbers may or may not be recorded in this quarter.