Its around 10 crores.

Posts in category Value Pickr

CFF Fluid Control Limited – SME (29-11-2023)

My biggest worry is negative cash flows. What’s your take on that observation? Along with the investor presentation, the management should hold regular con calls for better visibility. Thanks.

Manappuram Finance (29-11-2023)

(post deleted by author)

COSMIC CRF LIMITED – sme (29-11-2023)

Can you please share the financial impact this litigation could have on the company ? If you are aware about it.

Akash Portfolio (29-11-2023)

I have taken a position in Indian Renewable Energy Development Agency (IREDA).

Detailed analysis on IREDA by a reddit user is in the link below.

Risk factors according to the same user.

https://www.reddit.com/r/IndianStreetBets/comments/184xa9b/comment/kaz2c5i/

I think IREDA is a good proxy for renewable energy projects in areas of solar, wind or green hydrogen. I generally avoid lending financial companies and PSUs but this one appears to have better prospects and is growth oriented.

VST Industries: Puff full of power? (29-11-2023)

@Amit2saxena

Thanks for seeking my view. My view may be negatively biased due to my exit and investment in competitor ITC.

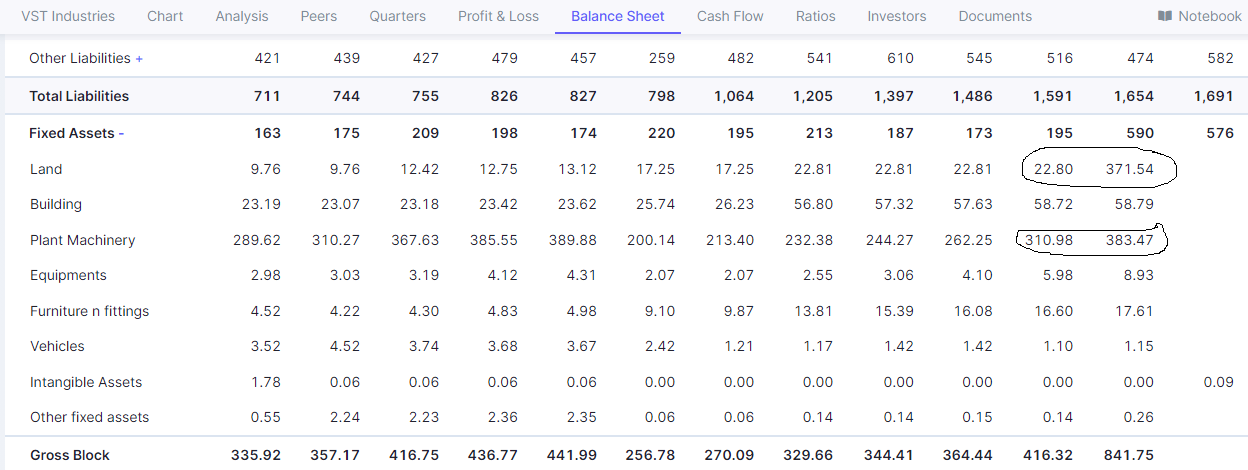

As correctly pointed out by you, the company spent around Rs 350 Cr for purchase of leasehold land. As per screener data Rs 350 Cr are utilised for purchase of land while around Rs 73 Cr is addition in Plant and Machinery which I assume normal mainteance and growth related expense.

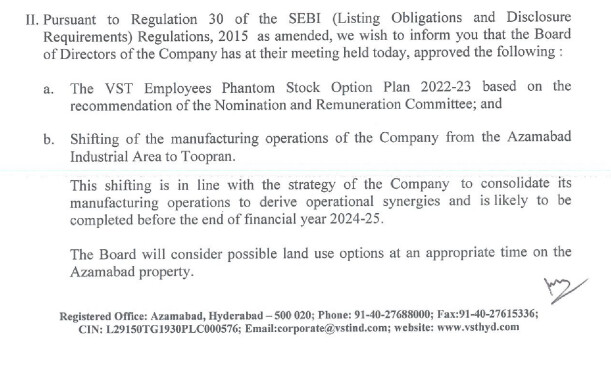

I also gone through Q2FY24 results which has following comments in the covering letter.

From this, it appear that company management intend to integrate its operations at one place and likely gain from synergy. Further, it is likely to release Azamabad property in Hyderabad, which may be encashed in future. Hence, to take a view only on purchase of land and infer that management is misallocating capital may not be correct in my limited understanding. One need to see action of management, specificially about land encashment/utilisation of Azambad in Hyderbad and how it share the benefit with the shareholders. In short term, such action would mean lower other income and hence lower dividend distribution, but in long term, it might be positive for the company.

Disclosure: I have exited from VST couple of years back and continue to remain invested in ITC. Hence, my view may be negatively biased. I have excellent track record in being wrong with my forecast. I am not SEBI registered advisor. I am suggesting any investment action in the company.

Laurus Labs – Can Business Transform to Next Level? (29-11-2023)

I think that is the nature of most businesses in this sector. However, I see Laurus to be a bit more aggressive in moving up the ladder and trying new things. If I look for the next Pfizer kind of companies in India, Laurus definitely comes in the radar.

The main concern is the cash burn in these activities. In that, I see two major streams of capital deployment:

-

Business model / product mix changes, requiring constant influx of capital, which can be expected and should be seen alongside the growth rate of company. I see Laurus having a good leg of growth coming ahead.

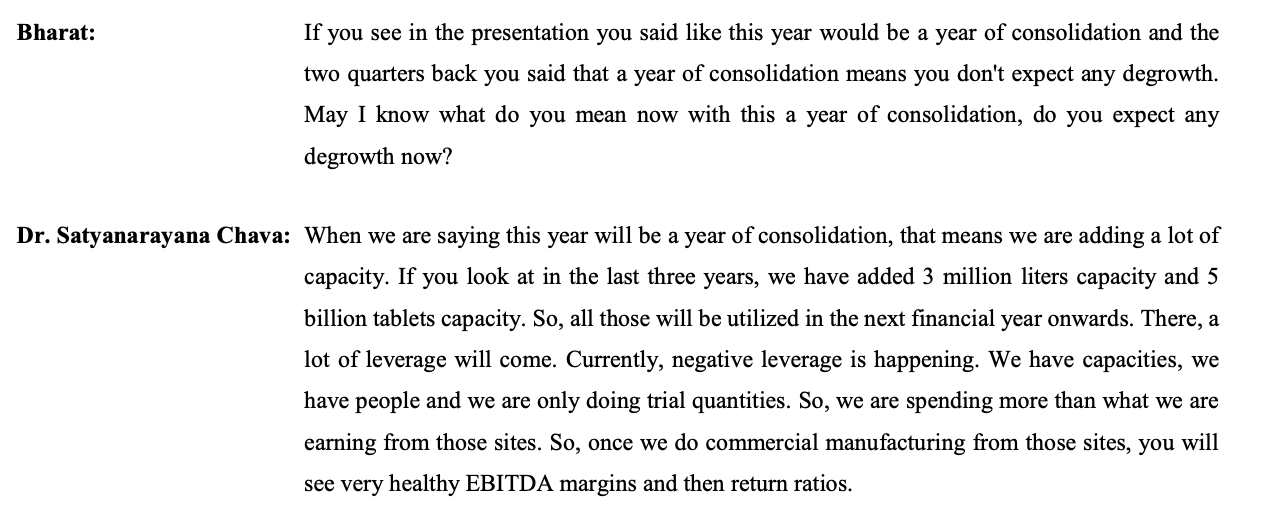

Their focus in CDMO is actually good. However, CDMO being a lumpy business can bring down the biz performance during lean period. Nevertheless, this is a good & necessary long term plan to match competition - Capex initiatives yielding fruition → This I am much keen to follow up since it has a twin benefit of improved revenue and margins (operational leverage). As per the mgmt, the demand looks good and inventory destocking should be over. So, there is a high likelihood that volume & capacity utilisation starts going up. Unless it does, we can’t expect the margins to move to a healthy level as mgmt mentions.

Snippet from earnings call below:

CFF Fluid Control Limited – SME (29-11-2023)

They have posted their investor presentation. Worth a look.

cff fluid control.pdf (909.2 KB)

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (29-11-2023)

As received from another sugar specialist friend

- This shortage is temporary, for 2-3yrs. And hitting non UP. UP mills will make bumper profits for 2-3yrs

- Gov has strong will to promote ethanol. And have incentivised ethanol investments. Some WTO mandate also. Gov won’t fck ethanol plants.

-

Smart are the players who are putting up dual feed plants. For max asset turnover.

… only Triveni, Balrampur. Dalmia. Dhampur - Industry will maximize its profits between sugar and ethanol. Whichever fetches them higher prices.

The only risk is disease and weather. For that, diversify amongst mills, don’t bet on single company!