I fail to understand why post demerger announcement price is being affected…???

Posts in category Value Pickr

Avanti Feeds (21-11-2023)

A lot of competition from shrimp in Ecuador…I dont think this will go up for some time

Avanti Feeds (21-11-2023)

Q2FY24 Results

Comparison of performance for six months ended 30/09/2023 with six months period ended 30/09/2022

Revenue (Consolidated)

- The total income decreased to INR 2,898 crores from INR 2,930

- The PBT increased to INR 270 crores from INR 197 crores (mainly due to decrease in the raw material costs and increase in other income)

Standalone Results

FEED DIVISION

- The total income increased to INR 2,415 crores from INR 2,352 crores in half-year ended FY23 due to increase in feed sales and other income.

- The PBT in HY FY22 increased to INR 212 crores from INR 130 crores in the corresponding period of the previous year, mainly due to decrease in raw material costs and increase in other income

SHRIMP PROCESSING DIVISION

The gross income for six months during FY24 was INR 491 crores as compared to INR 583 crores in corresponding six months’ period of the previous year. A decrease of INR 92 crores in the gross income during first six months of the FY24 is mainly decrease in quantity of sales by 1,144 metric tons

The PBT in six months FY24 is INR 63.60 crores as compared to INR 63.10 crores in the six months ended in FY23. The marginal increase in PBT is due to decrease in cost of raw materials consumed at ocean freight rates.

- No additional provision made to compensate for recall of the products (all the earlier provisioning is used up, 0.99 cr left )

Note : As regards the product liability claims for bodily injury caused by consuming company’s contaminated product under the recall, the company has submitted a revised claim for the claims received and settled by the company to the insurance company. The surveyor has confirmed that the claim will be processed by insurance company on or before 30th November 2023. Since the liability has been covered under the commercial general liability insurance policy, no provision has been made in the financial statements of the company.

Projections for the rest of the year

Feed :

On the basis of estimated shrimp production in 2023, the estimated feed consumption is about 10.5-11 lakh metric tons. The company’s feed sales during the previous year FY22 was about 5.41 lakh metric tons as compared to 4.73 lakh metric tons in FY21, an increase by 68,000 metric tons. However, the company’s estimated shrimp feed sales were 4.97 lakhs metric tons in FY23, down by 44,000 metric tons when compared with FY22. The company’s estimated production in sale of shrimp feed in the calendar year 2023 is about 4.9 lakh metric tons at the same level as in the previous year, when

the total Indian feed consumption is down by 15%. The company has been able to maintain its production and sales, though there was overall decrease in the country.

SHRIMP PROCESSING & EXPORT:

The countries vannamei shrimp exports in terms of value declined in FY23

compared to FY22 by 8.11% from $5,234.36 million to $4,809.99 million. The country’s overall exports of frozen shrimp in quantitative tons for FY23 was 7,11,099 metric tons as compared to 7,28,123 metric tons in FY22, a decline of 17,024 metric tons representing 2.34%. The company’s shrimp exports during the FY23 was about 12,497 metric tons as compared to 12,836 metric tons in the FY22, a decrease by 339 metric tons. It is estimated that the export during the FY24 would be around 12,000 metric tons.

- New Processing Plant and Cold Storage unit at Krishnapuram, East Godavari District with a capacity of 7,000 MT p.a. (Expecting commercial operations by Mar’2024 )

New Initiatives

- PET FOOD : Entering into JV with Bluefalo Pet Care Company Limited Thailand (51% by Avanti and 49% Bluefalo) – Market research is in progress about the demand for Pet products in Indian market (Aiming to launch to market by 1st Jan 2025)

- FISH FEED : Huge shortage in the domestic market , most of it is being exported to address this issue working on initiatiative to make it locally for captive consumption and sell in export markets, market research is in progress, an agreement is signed for tech. transfer with Thai Union Feedmill

Raw Material prices are stable , may go down in coming months due to new crop is coming into the markets

52 week highs and all time highs strategy (21-11-2023)

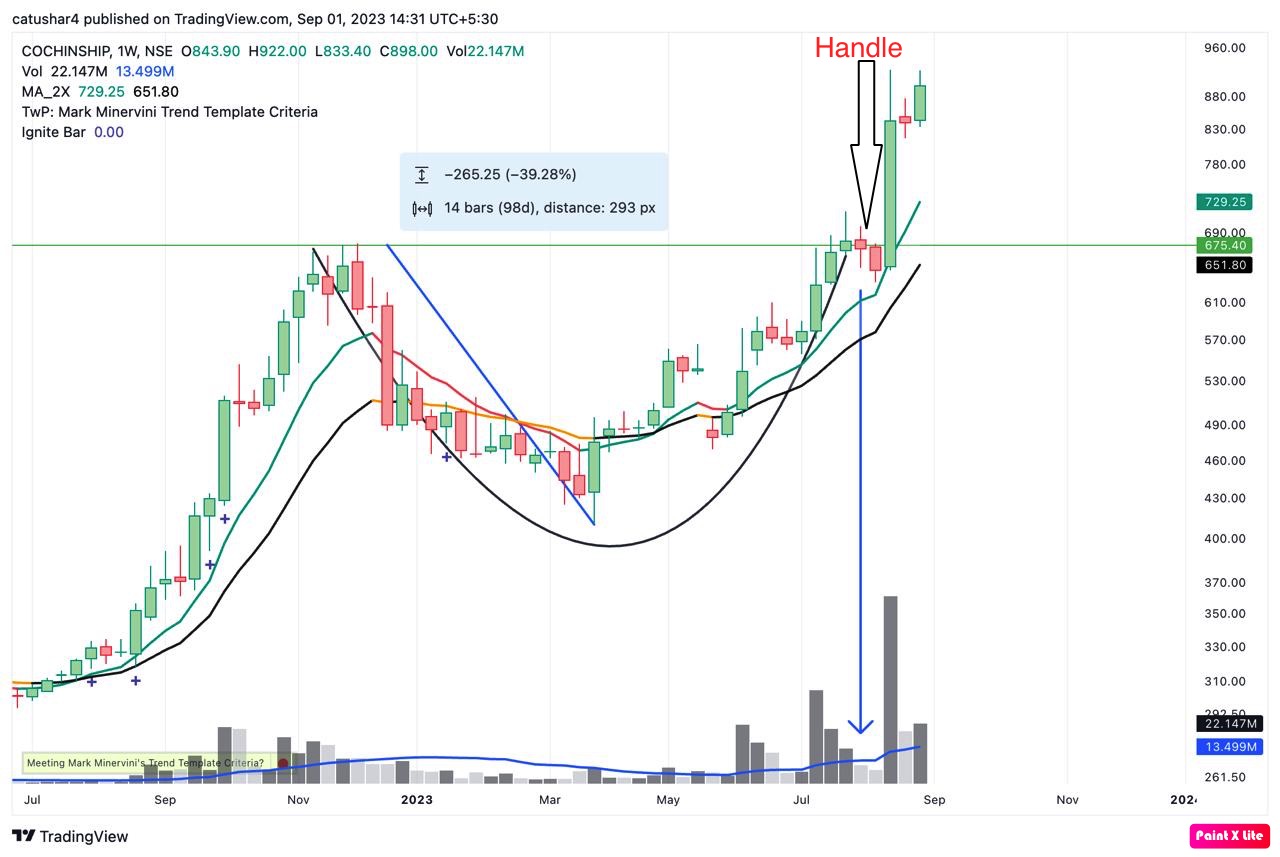

I have joined this esteemed forum last week, thus I had an opportunity to see various charts being posted on this thread. I saw some charts with ‘cup with handle’ pattern. So, thought of sharing one of an old chart wherein this pattern was formed.

Mr. William J. O’Neil’s in one of his best sellers explained this pattern. Thus, it is a small effort to bring out his book’s points vis-a-vis the description in the instant chart :

- The depth should range from to the low of 12 to 15% range to upwards of 33%. However, in the chart it is around 39%.

- Pattern must form a ‘U’ (ranging from 7 to 65 weeks) to make sure that weak hands are out of the stock. Also, it do not come to the attention of the speculators. In the given chart the U is of 35weeks.

- The handle of the cup should take more than one or two weeks to form and should have a ‘shakeout’. In the chart the handle took 2 weeks with shakeouts.

- Volumes may be dried up near the low’s in the handle’s price pullback phase. Observe the volumes in the chart (marked it with blue arrow).

- Lastly, and a very important pointer to keep in mind is that the handle should be above the stock’s 10 WMA, as the handles that forms completely below the stocks 10 WMA are weak and failure-prone. Further, the wedging up or the side way handles have a much higher probability of failing when they break out to a new high. In the given chart the ‘Green” curve is of 10 WMA.

What is your real return? (21-11-2023)

What is the logic behind looking at currency depreciation? I understand it could be relevant for folks living in the US and investing in India but otherwise can you explain how it would impact the general investing public? The inflation adjusted return makes sense but then i think that taxes and dividends should also be accounted for.

Cupid Ltd – Helping the world play safe! (21-11-2023)

Thank you so much for the detailed notes. Just a few queries, would really appreciate if you could point in the right direction

- I tried looking up Mr Halwasiya to understand the business he was referring to in point # 1 of your notes. Will really appreciate it if you could help.

- The contract manufacturing in Point #9 is for the male or female condoms and is it for the same market leader in the us that’s referred to in Point #7

Thanks in advance.

Regards

Disc:invested

KPIT – CASE (connected, autonomous, shared, electric) – Focused Automotive Play (21-11-2023)

(post deleted by author)

Ranvir’s Portfolio (21-11-2023)

Sula Vineyards Q2 highlights –

Sales – 142 vs 128 cr, up 11.6 pc

EBITDA – 45 vs 38 cr, up 18 pc (margin @ 31.6 vs 29.8 pc )

PAT – 23.1 vs 19.5 cr ( up 18 pc )

Sales breakup –

Sale of Wines – 126 vs 113 cr

Wine Tourism – 12 vs 9 cr

Sale of Elite and Premium wine sales ( > Rs 700/bottle ) @ 73 vs 71 pc YoY. Elite and premium sales grew by 15 pc, while economy and popular sales grew by 4.5 pc YoY

The Source – brand doing really well

Company conducted 49k+ tastings at their vineyards and 35+ cities across India – up 45 pc YoY

Popular and Economy segment facing heavy discounting and intense competition

Institutional shareholding (FII + DII) @ 36 pc now

In Q1, Q2 – CSD sales more than doubled

India’s per capita wine consumption currently @ 25 ml vs 850 ml for China. In Europe, it is > 2000 ml

Grape harvest likely to be robust leading to supply security

Currently, the Wine Tourism is primarily happening from Nahsik facility. Aim to set up a similar resort near the Bangaluru facility as well. Availability of land is not an issue

In UP, Haryana – 90 pc of sales were from Noida, Gurugram. Company now actively trying to expand into smaller cities

Sales contribution from Maharashtra in first half @ 48 pc vs 54 pc last year

Current Gross Margins @ 78 pc – company very happy with the same

Company’s is gradually losing mkt share in the economy segment because of its premium focus

Disc: holding, biased, not SEBI registered, hoping for buoyant Q3 results

What is your real return? (21-11-2023)

Asset allocation between equity and debt / gold is touted because it slightly minimizes the portfolio drawdown. And if there is less drawdown, it is psychologically easier to follow through the plan. But, logically for psychological comfort one takes in less return.

One way to visualize and stick to equity is this:

- Dividend payout (in Rs) of Nifty has never had a drawdown of more than 10%. I evaluated for past 15 years. It is probably the same when extended over longer period.

- Decently diversified equity portfolio increases its dividend at an approximate rate of 10 to 15%. Nifty has about 10%. Whereas, debt / government securities have zero growth rate of interest income.

- If you have Nifty 50 as your portfolio or a coffee-can portfolio and live on dividend income. Then it is an extremely stable source of income, even during market crashes and panics (including Global financial crisis, Covid crisis etc.). The only caveat is that you don’t re-shuffle your portfolio a lot.

Krishca Ltd : A SME offering steel strapping Solution (21-11-2023)

Thanks for the correction. Will delete this post shortly