From a purely stock movement, Biocon has not done anything for the last couple of years. I am not able to understand why simply from the data which seems positive. Have been holding for several years – in fact it was the Biosimilar’s story that attracted me in the first place

Posts in category Value Pickr

Digispice – play on the rural economy (14-11-2023)

SUMMARY OF Q3 CONCALL

-

Company now has a network of 1.3 MN adhikari and have presence in 2.4 lakh villages and 6500 blocks. Company now wants the adhikari network to become a financial services network.

-

Strong headwinds are there in the AEPS segment

-

Service fee revenue has grown 9% on YoY basis and 2% on QoQ basis.

-

Company started out building Spice Money as a network to deliver basic cash payments. Now the company is moving on from just a cash payment business to a multi-product business.

-

Collection business is now contributing to 13% of the company’s GM. The GTV has grown 59% on a YoY basis from 4300 crs to 7000 crs. Bill payments is also seeing a significant ramp up YoY from 516 crs to 1043 crs and 20% growth QoQ.

-

Banking services, the company has started selling CASA accounts. Opened around 43000 accounts vis-a-vis 57000 accounts. The float however is continuing to increase.

-

Credit is also an important business line for the company. Company has dispersed over 73000 loans aggregating to around 222 crs.

-

Fundraising the company will think of after a few quarters once the business model stabilizes around not just being an AEPS centric business but a few more products.

-

Company hired BCG to work with them to define the strategy for next 5 years.

Disclosure – Invested

Rajesh’s portfolio (14-11-2023)

Mercury EV-Tech has formed an in-house assembly line for the 2W & 3W products where production of 2W has been started with brand name of “EZ” and “Smart”. The Company has introduced this model in market with 130+ dealers network PAN India. Company owns an 18-acre land where it has started setting up in-house facility for manufacturing key components like battery, chassis, motor controller, brake shoe, CED paint and already operational assembly line. The company’s mission is to continue towards a responsible and green transportation journey with innovative and advanced Make-in-India electric mobility solutions. It aspires to provide all-inclusive service and charging stations across the nation to push the market towards a clean energy alternative.

As per Annual Report FY2023: The Company already have land bank of Rs 30 Cr.

Pricol limited – OEM automotive (14-11-2023)

Pricol Q2FY24 Concall Notes:-

• Revenue breakdown DIS 65%

ACFM : 35%

• FY26 Guidance of 3600 crores organic sales maintained unless any

catastrophic geopolitical event

• Slow down in ev 2 wheelers due to fame subsidaries ( Loss of sale)

• DIS sales 65% comes from 2 wheelers

• If and when there is need promters will incrase stake in the company

• Steadily increasing margins continuing to aiming for 13.5% ebidta margins

• New products ususally contribute by around 20%

• Revenues from MOU ventures to start contributing from FY26 ( most of them being exclusive in nature)

• EV two wheeler contributing 7-8% of volumes ~ Value contribution is a bit higher

• 8/10 ev two wheeler’s TFT display is from pricol

• Two wheelers Average mechanical DIS cluster costs 300 rs vs 1250 electronic ( Can go up till 2500 rs avg)

Sula vineyards – pioneers in indian wines (14-11-2023)

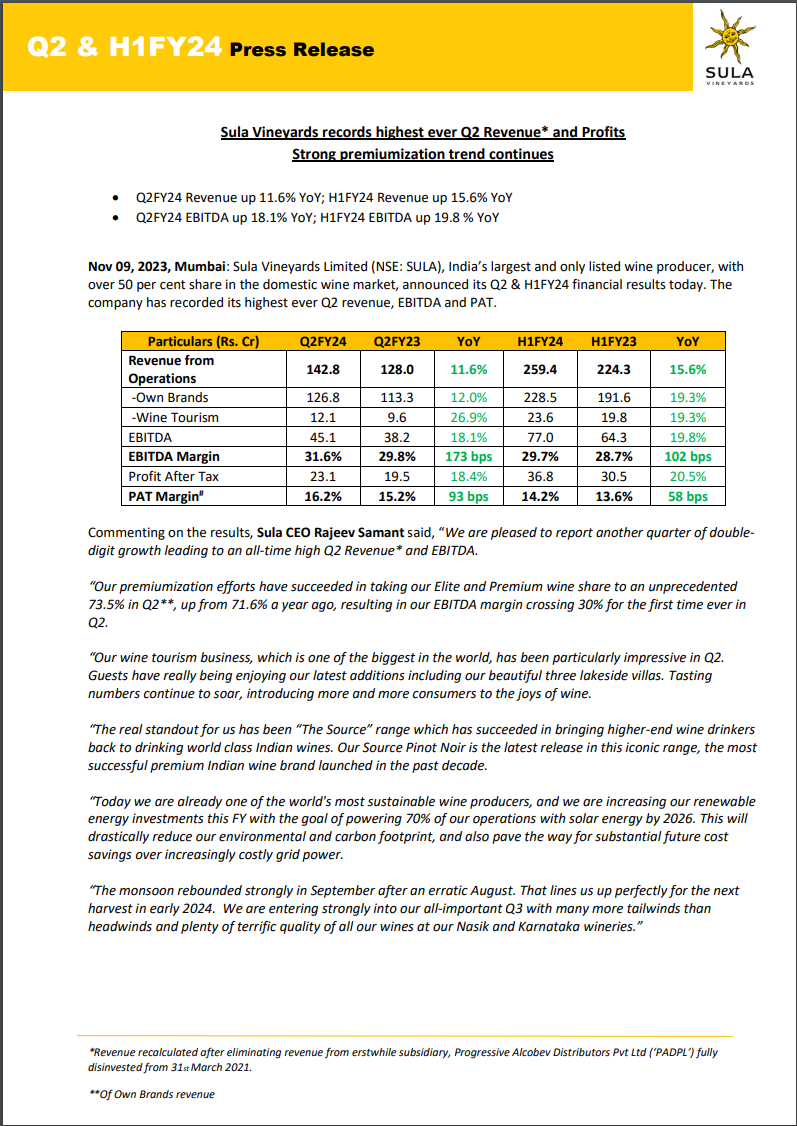

Sula Vineyards Limited, India’s largest listed wine producer, has achieved its highest-ever Q2 revenue and profits, showcasing robust growth and a continuation of the premiumization trend.

Financial Highlights:

- Q2FY24 Performance:

- Revenue increased by 11.6% YoY, reaching an unprecedented level.

- EBITDA rose by 18.1% YoY.

- The EBITDA margin crossed 30% for the first time in Q2.

- PAT grew by 18.4% YoY.

- Premiumization and Market Share:

- The company’s premiumization efforts increased Elite and Premium wine share to 73.5% in Q2, up from 71.6% a year ago.

- The EBITDA margin surpassed 30% due to this premiumization strategy.

Financial Details:

- Q2FY24 Financials:

- Revenue from Operations: Rs. 142.8 Cr (11.6% YoY growth).

- Own Brands Revenue: Rs. 126.8 Cr (12.0% YoY growth).

- EBITDA: Rs. 45.1 Cr (18.1% YoY growth).

- EBITDA Margin: 31.6% (173 bps increase).

- PAT: Rs. 23.1 Cr (18.4% YoY growth).

- PAT Margin: 16.2% (93 bps increase).

- Consolidated H1FY24:

- Revenue from Operations: Rs. 259.4 Cr (15.6% YoY growth).

- EBITDA: Rs. 77.0 Cr (19.8% YoY growth).

- EBITDA Margin: 29.7% (102 bps increase).

- PAT: Rs. 36.8 Cr (20.5% YoY growth).

- Premiumization and Market Share:

- The company’s premiumization efforts increased Elite and Premium wine share to 73.5% in Q2, up from 71.6% a year ago.

- The EBITDA margin surpassed 30% due to this premiumization strategy.

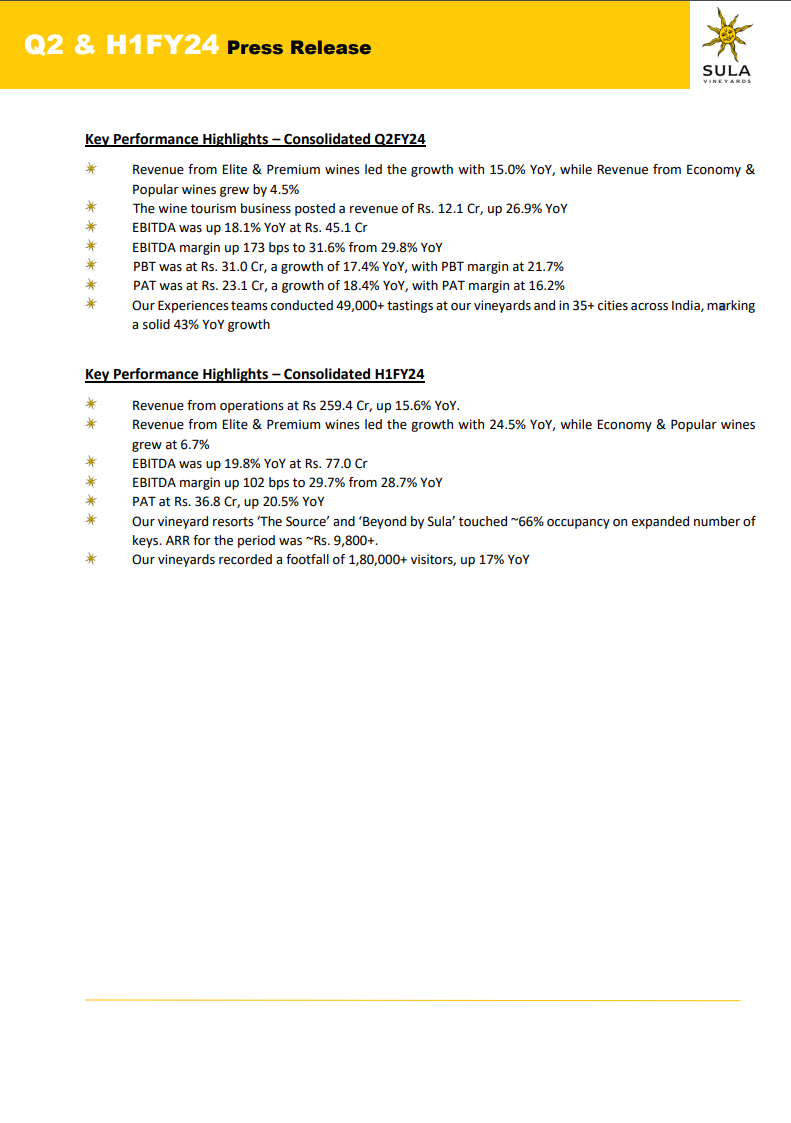

- Wine Tourism:

- The wine tourism business showed substantial growth, with revenue up by 26.9% YoY in Q2.

- The CEO highlighted impressive numbers in tasting events and the popularity of new additions like lakeside villas.

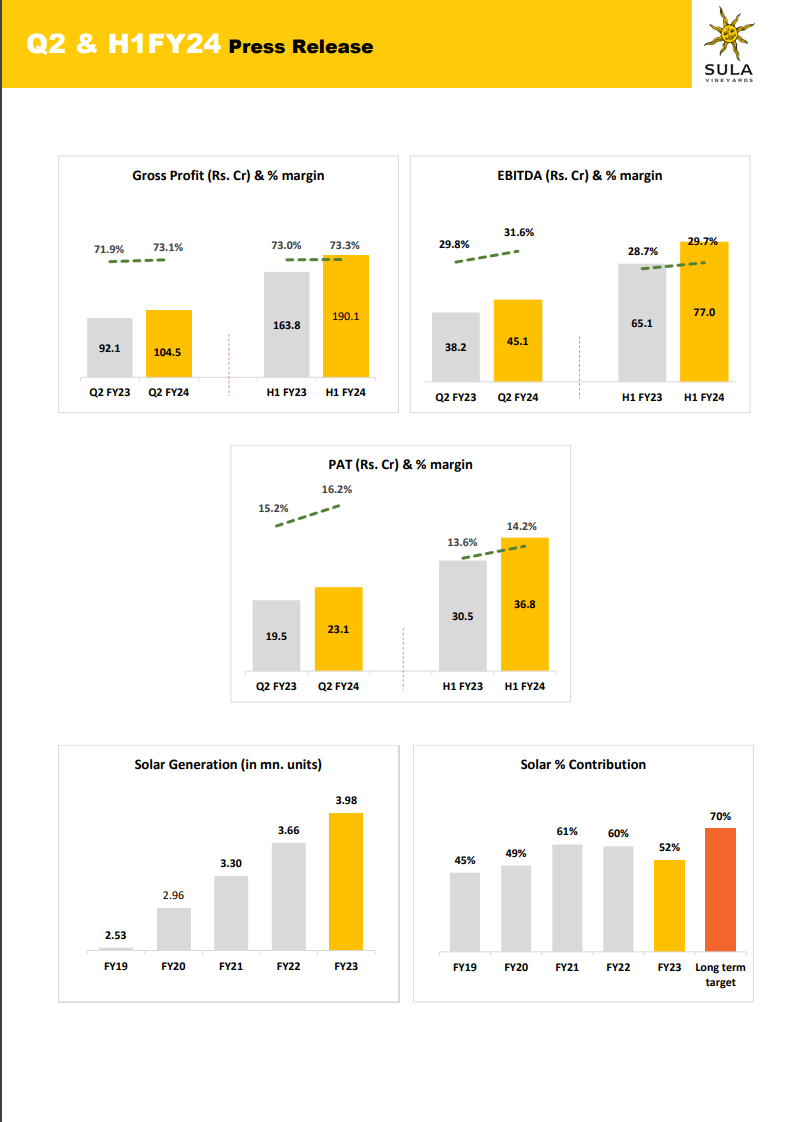

- Sustainable Practices:

- Sula Vineyards aims to be one of the world’s most sustainable wine producers.

- Plans include increasing renewable energy investments, with a target to power 70% of operations with solar energy by 2026.

- Future Outlook:

- The strong rebound of the monsoon in September bodes well for the upcoming harvest in early 2024.

- The company is optimistic about entering Q3 with favorable conditions and maintaining wine quality across its wineries.

Other Highlights:

- The Elite & Premium wines drove growth, recording a 15.0% YoY increase in Q2.

- The wine tourism business contributed significantly to revenue, with impressive numbers in tastings and visitor footfall.

- The vineyard resorts ‘The Source’ and ‘Beyond by Sula’ showed strong occupancy rates.

- The company’s sustainable practices and renewable energy goals were emphasized.

Hitesh portfolio (14-11-2023)

Hey sorry but I don’t understand the question and exactly what is it that you need my views on! If you could simplify it in a few sentences it would help

Caplin Point Laboratories (14-11-2023)

Yes, the management gave couple of reasons for both receivables and inventory days. They have answered this in the concall at length. Please refer the below video. The CFO/EBIDTA ratio is still better than most pharma companies.

Caplin Point Laboratories Ltd Q2 FY24 Earnings Concall

Disc : Invested at lower levels and biased.

Note: Skip to 21:00 to hear the question and answer

Multi-Disciplinary Reading – Book Reviews (14-11-2023)

Woah, truly epic in scope with a deceptively innocuous title. Thank you for reading and summarizing this book.

I have very belatedly recognized the importance of history – unfortunately the subject was treated in school as just a chronicle of events or propaganda. But history is the most reliable way to get an appreciation of the base rates of the key outcomes of a situation; and hence useful for investing as well. Kissinger (who is by far the most brilliant and a renowned ‘applied’ historian) said history teaches you to compare the current with analogous situations in the past. He said (or so I think) he would always prefer a historian to an intelligence analyst when he was in office.

Historians often come with substantial hindsight and WYSIATI biases. E H Carr in his celebrated lecture “What is History?” deals with these biases beautifully.

In any case I need to read this one for sure.

Hitesh portfolio (14-11-2023)

In an attempt to try and think about an investing conundrum in a clearer way, I have written down my thoughts (sort of a journal) in the note below. Would appreciate thoughts/perspectives.

–

I have been thinking of a situation – as value-conscious mid & small-cap investors, we buy companies after extensive research and when they do work out, sell when we think it’s overvalued and end up making, let’s say 3x or 4x over a period of few years. In all likelihood, these stocks go up a further 50%,100% or 200% and that too in a matter of weeks/months. If I was this investor, I would definitely feel like a fool waiting out 5 years for a 3x-4x return and then miss a further 100%, 200% in a matter of weeks/months. This would lead me to think – how do I play the “Greater Fool” game and maximize the selling price each time?

Firstly, what is the “Greater Fool” game? I think a phase of greed, because stock prices are increasingly detached from fundamentals. So in order to win at this game, the next question would be – at what level of greed will the stock reach its top? Certainly a question which cannot be answered?

Even if we find a way to identify the top, what guarantee is there that there will be sufficient liquidity to exit timely? Also, doesn’t this state of mind come in the way of level-headed thinking – an important aspect for success in investing?

As an example, I think it’s fair to say that the probability that an investor in 2011 could correctly predict a Mayur Uniquoters going from a P/E of 7-8x to a P/E of 20x is much higher than predicting where it can go from there? So unless we’ve identified an outlier (and hence would give it a longish rope), the discipline to sell when we think it’s overvalued is important? Else, not much has to go wrong to lose significant amounts of money in such investments (even with a stop-loss?), because they are prone to sharp corrections?

Isn’t this Mr. Market’s ultimate test – to test how firmly investors stand by the core investing principles? Only those who have the discipline to consistently do so are successful across market cycles?