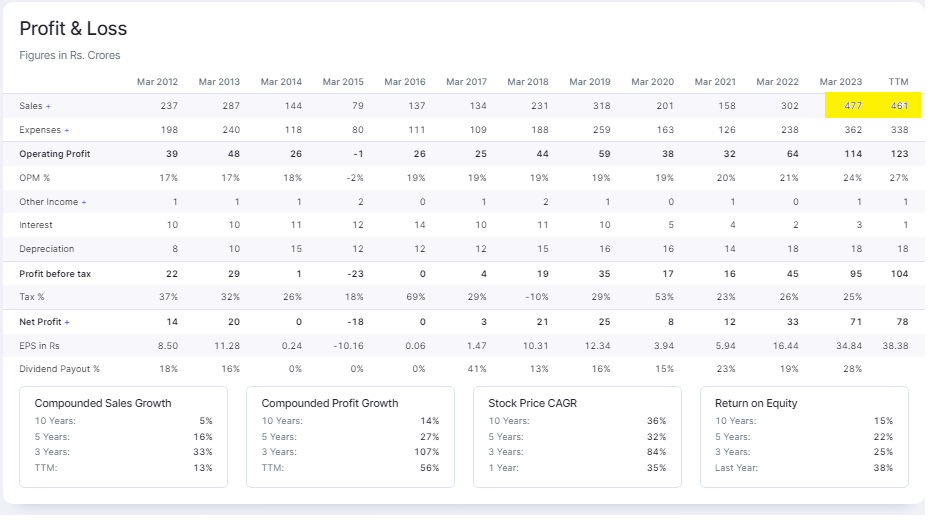

Steelcast: The company aims to reach at least Rs. 1,000 crores of sales over the next four to five years.

Right now company is doing 400 odd crores

Steelcast: The company aims to reach at least Rs. 1,000 crores of sales over the next four to five years.

Right now company is doing 400 odd crores

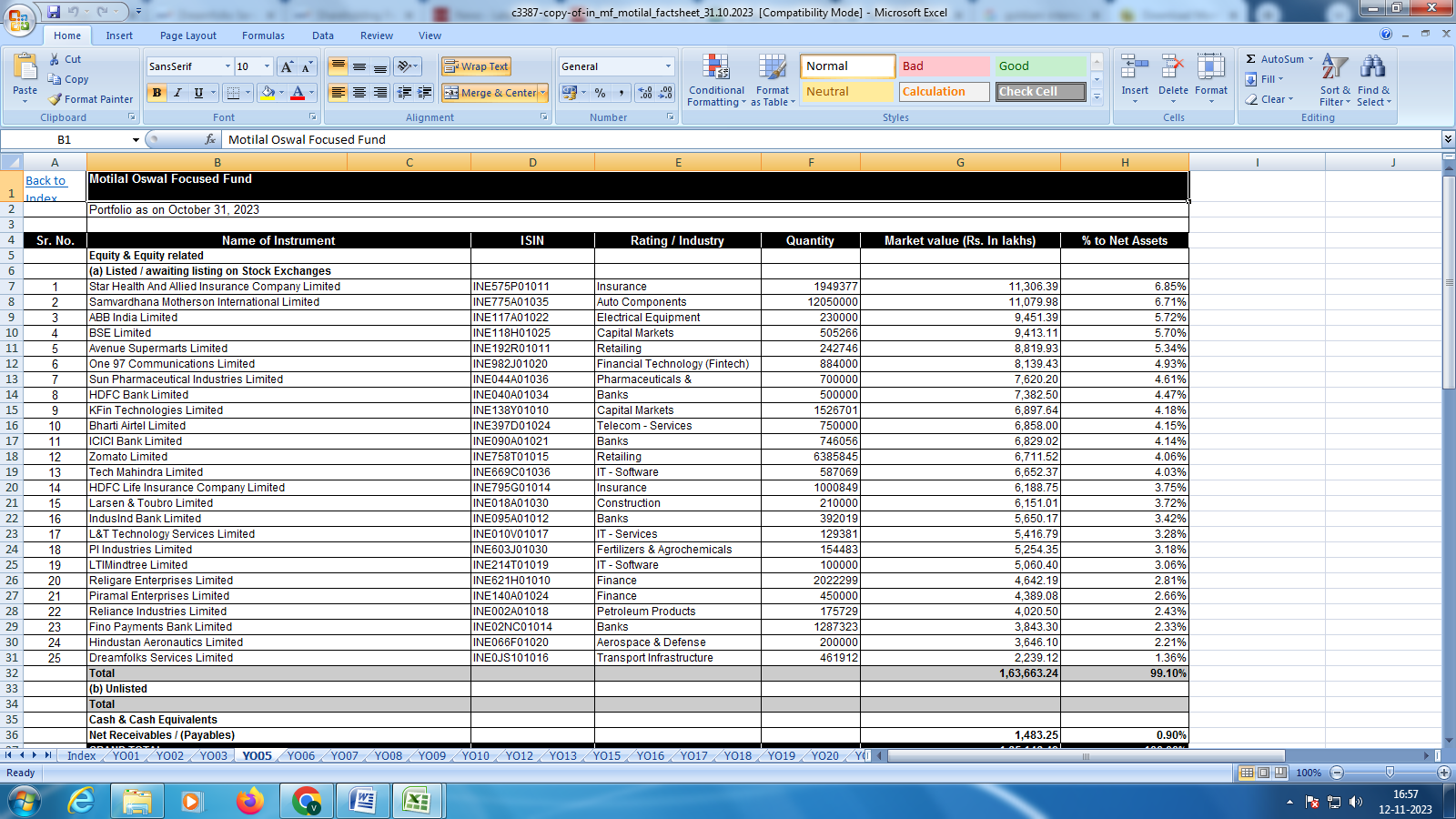

Motilal Oswal Focused Fund bought 461912 shares of Dream in the month of Oct 2023…

Moderator may delete this post if thinks it doesn’t add any value…

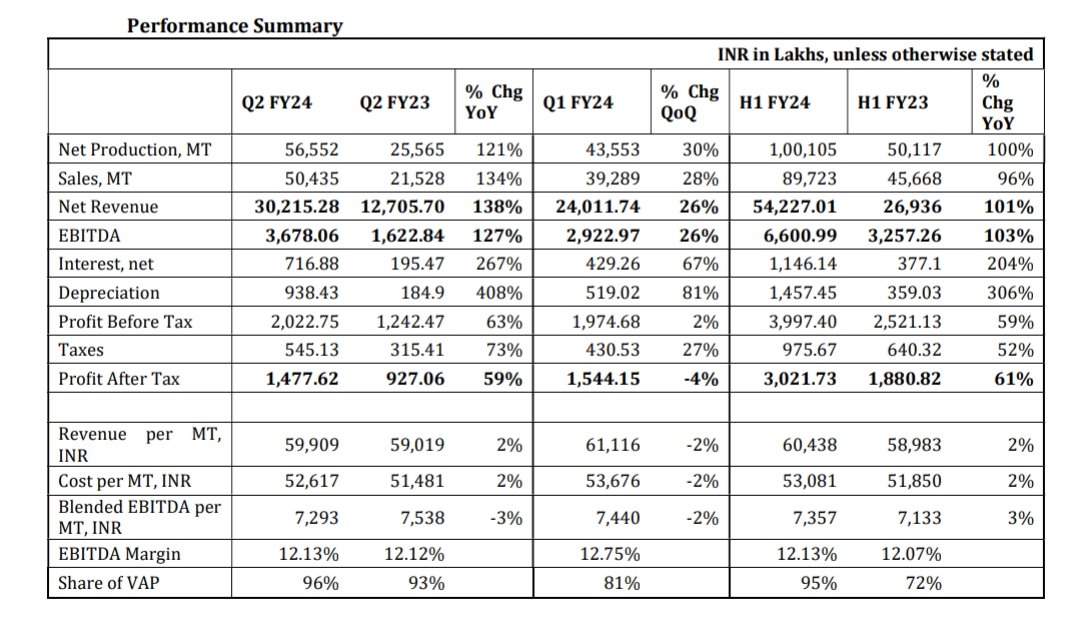

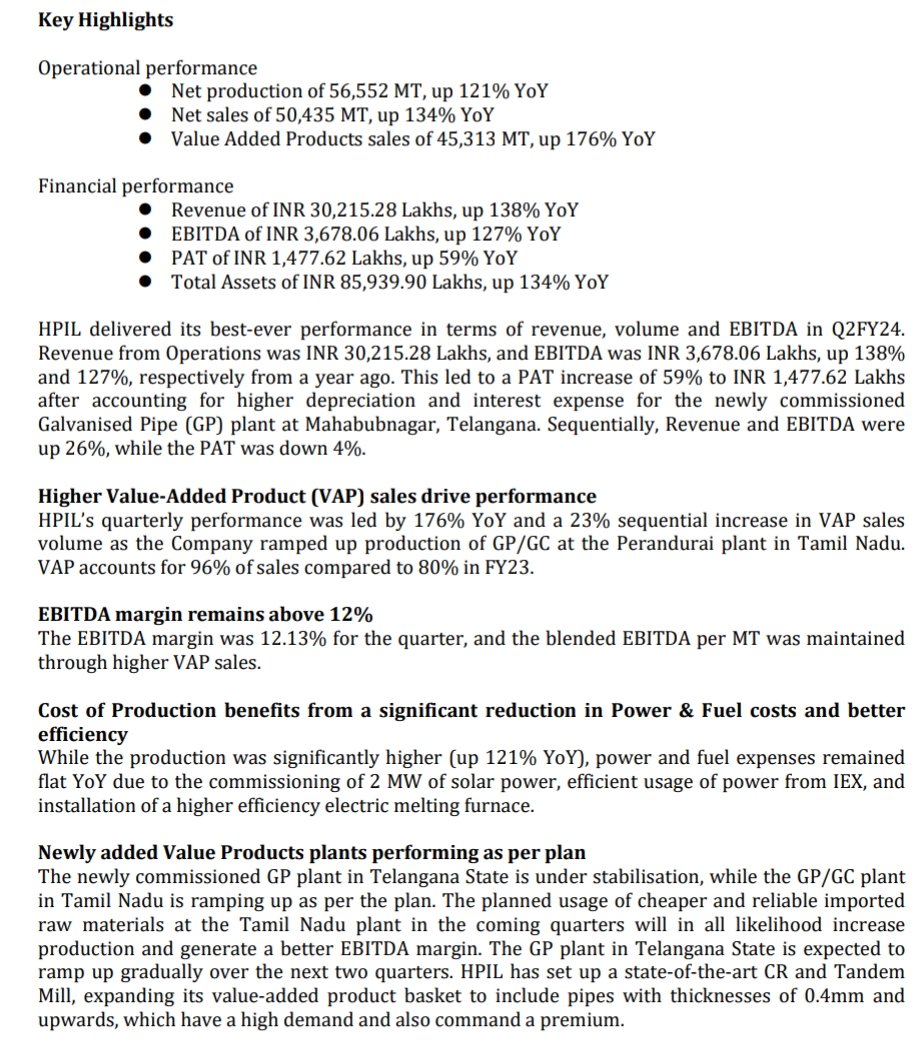

My Take on Q2 Results:

Not so WoW Results, but justified a deep look ![]()

-Revenue up 138% YoY n 26% QoQ

-EBITDA up 127% YoY n 26% QoQ

-EBITDA Margin at 12.17% vs 12.78% YoY vs 12.17% QoQ

-PAT up 59% YoY n -4% QoQ

-OCF weak -60.8 Cr vs -23.8 Cr

Looking weak,

But a deeper look ![]()

Why PAT Growth lower?

-High Int & Dep Exp (Cauz of Capex)

Why Int Higher?

-Weak OCF (last 1 year -ve CFO)

Interesting things:

-Volume Growth is much higher 134% YoY n 28% QoQ🔥

-Value added share increased to 96% from 93% YoY

-VAP Volume increase by 176% YoY n 23% QoQ

-Realisation Growth is flat (Not selling product at depress price, to show good Revenue Growth)

-Highest ever volume & sales number

-Power & Fuel cost flat, even though FA doubled (cauz of Solar)

-Capex is ramping as per plan

-Will import cheaper RM to expand EBITDA Margin

About Weak OCF?

-Hariom is telling us that we need 2-3 Quarters time to improve CFO because of too much Capex, they need to maintain product, product mix & supply chain to stabilize

Weak CFO has led to high borrowings in B/S & high interest exp. impacting PAT

First ever presentation released:

Let’s analyse it:

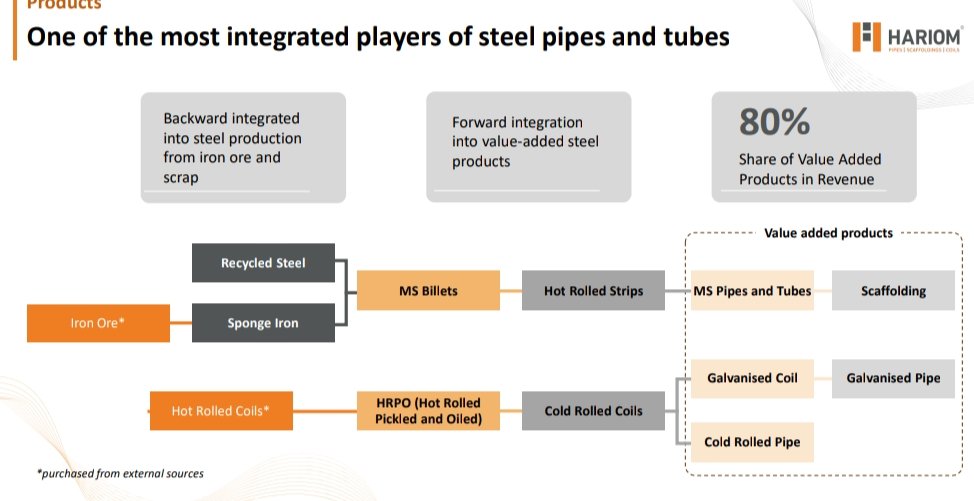

Value Chain

-Backward integrated steel production

-Forward integrated into VAP steel products

-More than 95% VAP sales

-Reason behind high EBITDA Margin compared to other players

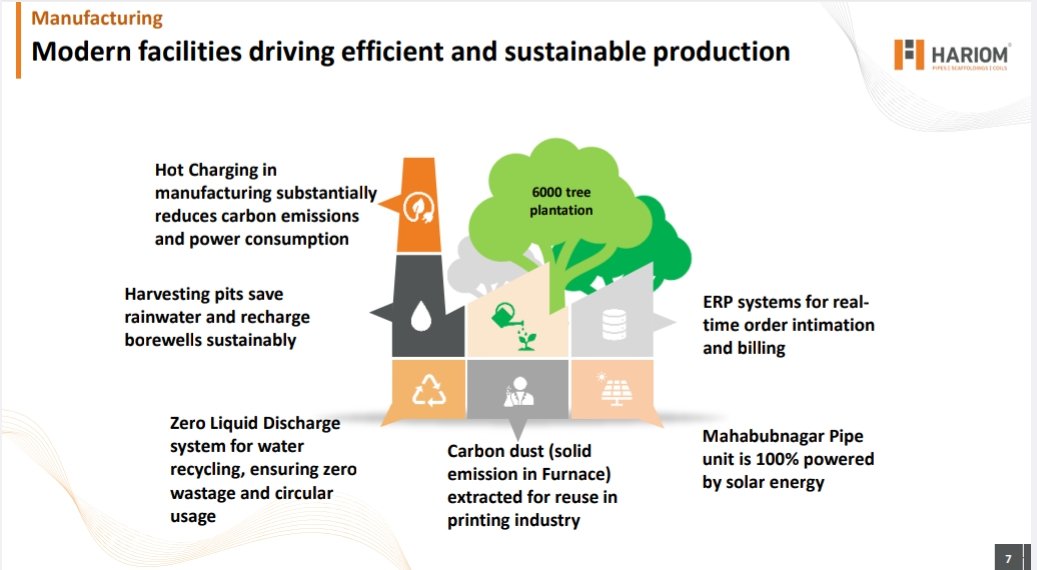

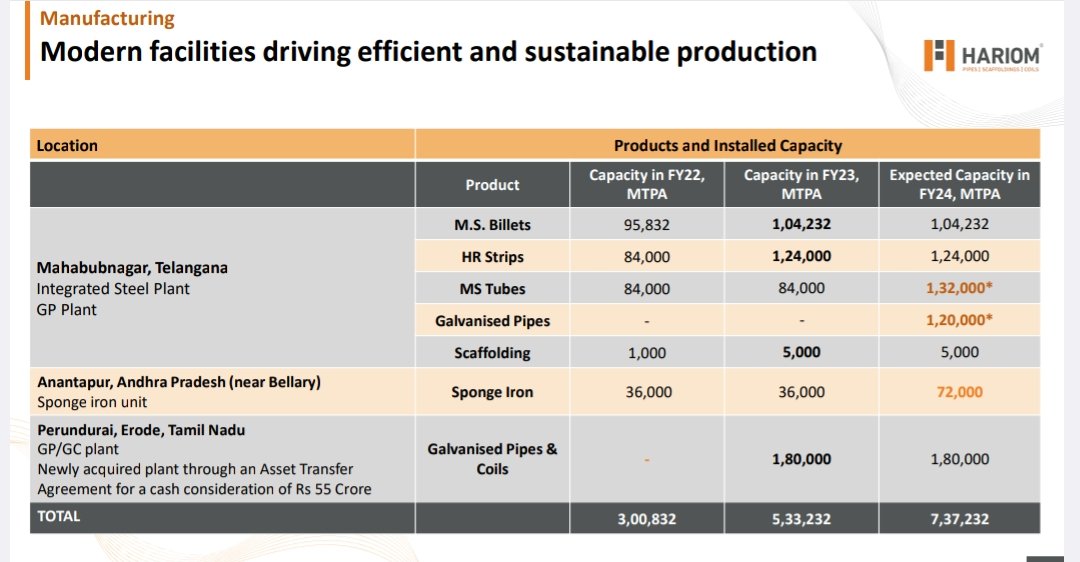

Modern & Sustainable use of technology for production

-Capacity expanded more than doubled from FY22 base thorough acquisition & capex

Hariom has:

-250+ Product specification

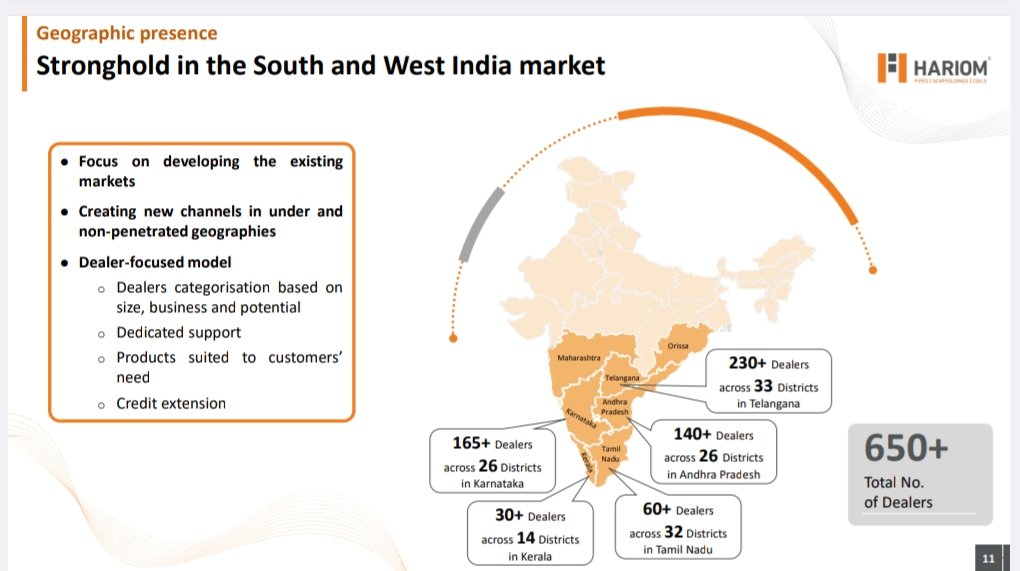

-1500+ Dealer network and POS

-Strong presence in South & West Market

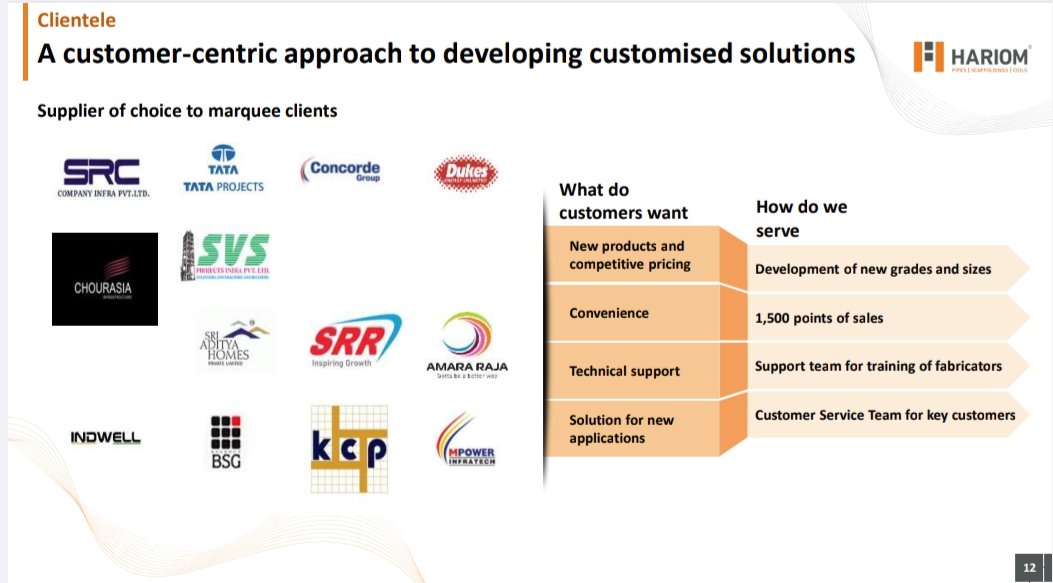

Customers:

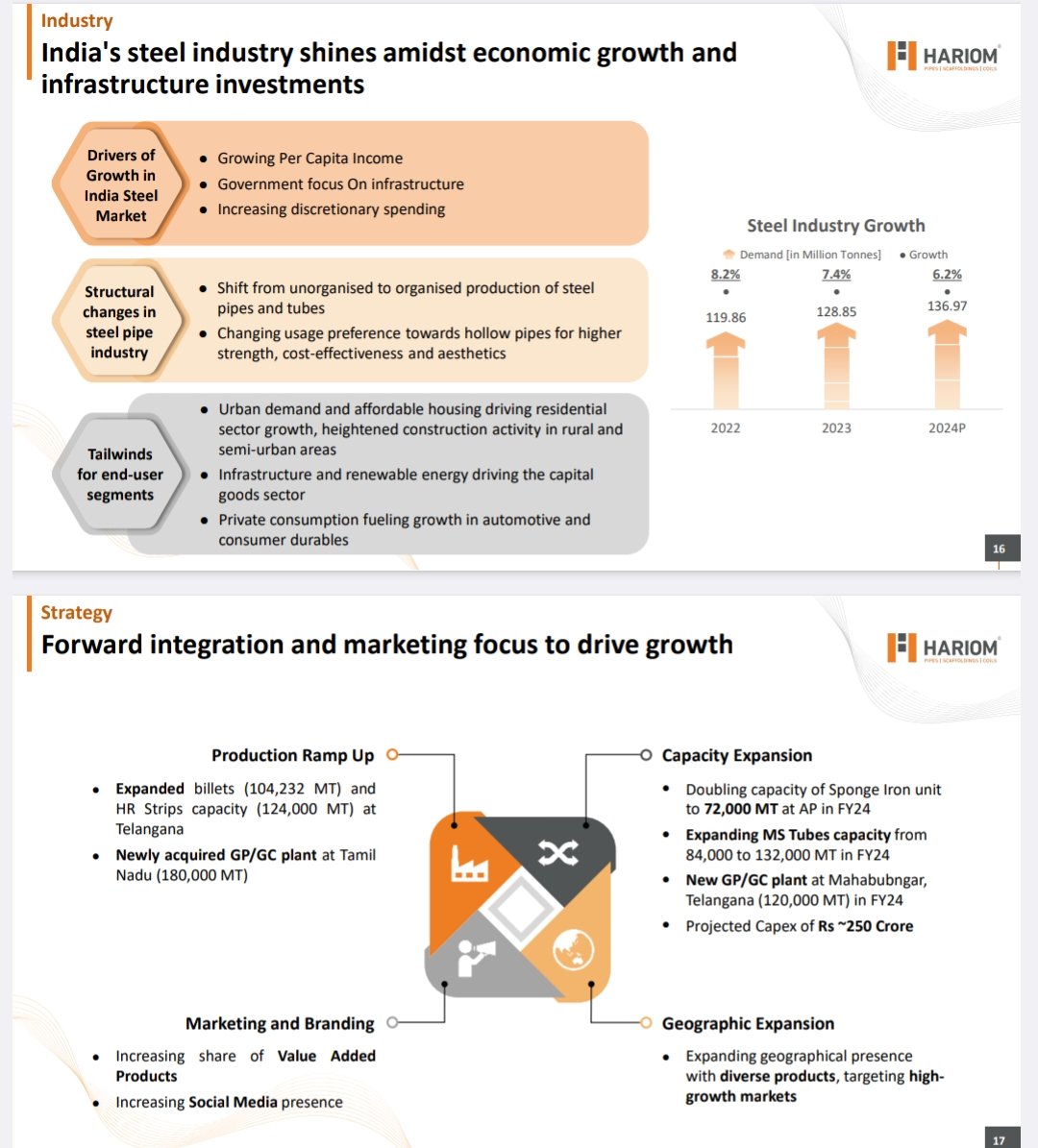

Guidance:

-Goal to reach 2,500 Cr revenue by FY26

Achieve thorough:

-Improving product portfolio

-Grographical expansion

-Capex led growth

-Marketing & Branding

-Industry tailwinds

My look:

-Results look neutral to average in hindsight as CFO -ve, Borrowing up, no margin expansion, high dep & low pat growth but

Management is saying:

-Wait & give us 2-3 Quarter to stabilize & things will look much better after that

Also, all the long term triggers are intact

-Grographical expansion + Power cost flat + VAP mix improving + Industry cycle + sales growth + importing RM to improve GP Margin

All good… will wait & give time to Hariom to show their true growth…

No Recommendation

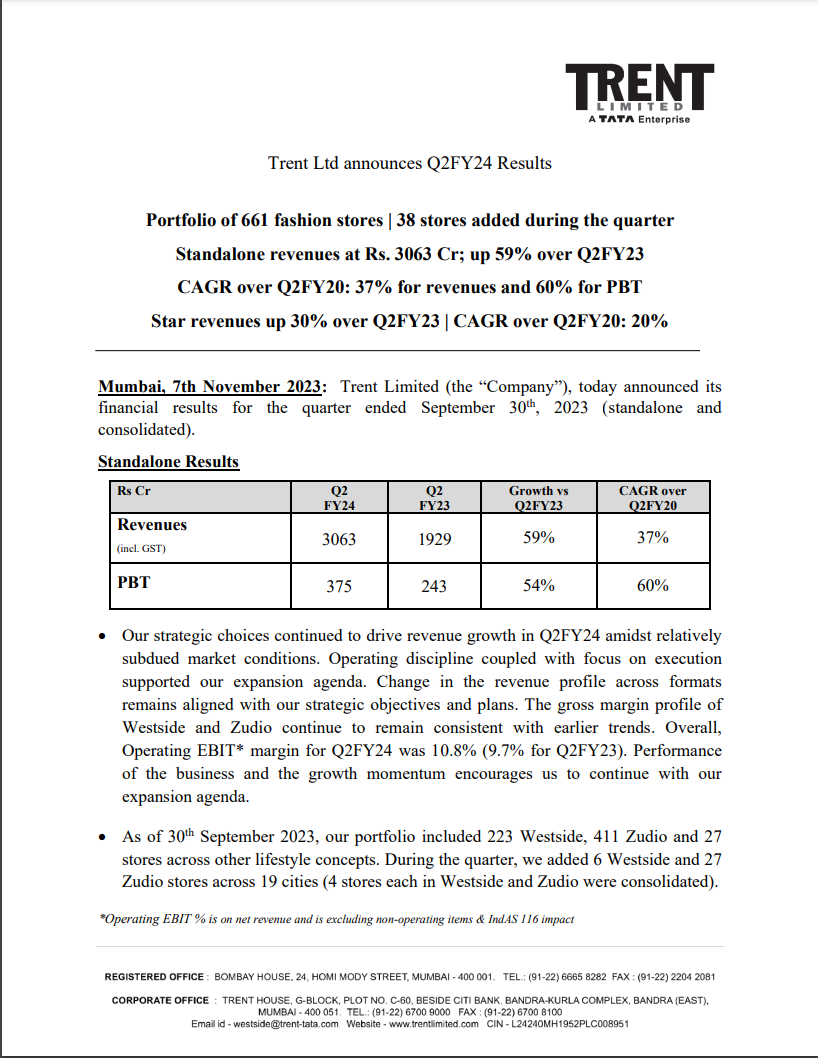

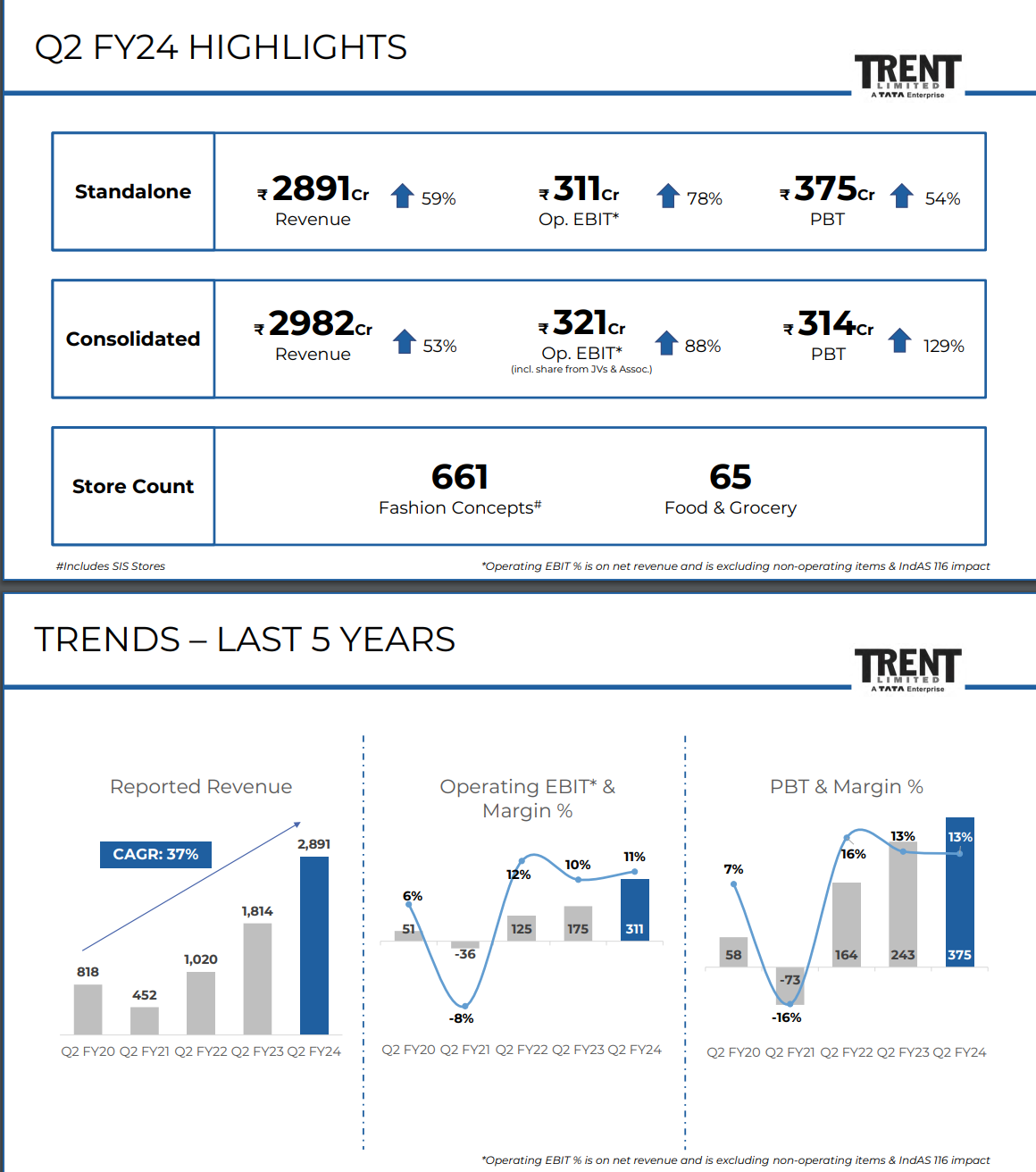

Standalone Results:

Trent Limited’s strategic decisions and operational efficiency have contributed to revenue growth, even in challenging market conditions. They have been focusing on expanding their store network and maintaining consistent gross margins. The Operating EBIT margin for this quarter stood at 10.8%, up from 9.7% in the same period last year, which is a positive sign. The company’s performance and growth trends support their plans for further expansion.

As of September 30, 2023, Trent Limited’s portfolio included 223 Westside stores, 411 Zudio stores, and 27 stores across other lifestyle concepts. In this quarter, they added 6 Westside and 27 Zudio stores in 19 different cities.

Their fashion concepts have seen strong Like-For-Like (LFL) growth, with a focus on offering consistent value and a unique product range to customers. Emerging categories like beauty and personal care, innerwear, and footwear have also gained popularity and now contribute over 19% of the company’s standalone revenues.

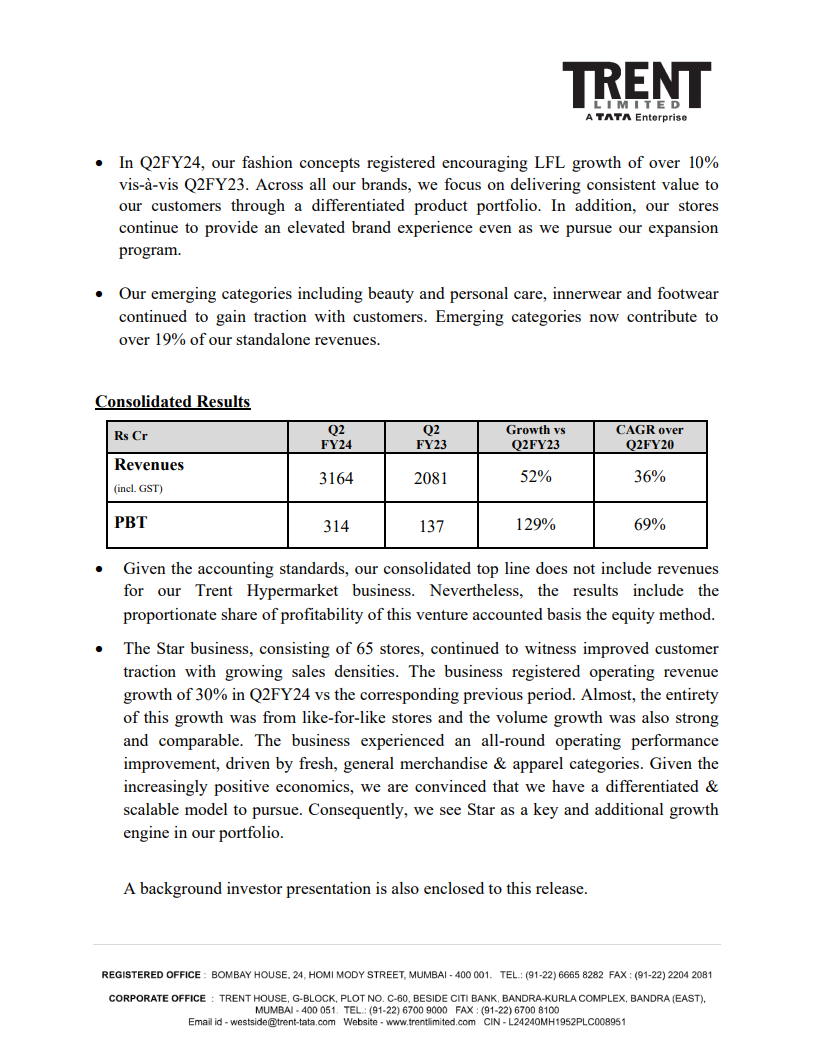

Consolidated Results:

Even if we assume it’s bcs festive season shifting to the next quarter.

Results are flat even if we compare them with Q1 of the last year. It might be the case of in general slowdown compared to last year as peers too had similar result.

We need to know from which are key states it generates revenue from ?

Hello Sir,

Tommy Hilfiger has had 2 brand licensee in India

Titan For watches

Arvind Fashion for Clothes

And now Brand concepts for bags

They Haven’t Changed any of their Brand licensing agreement

but lets see

The steps to onboard the licensing brand is very stringent

you have to make sure that you manufacturing process is complied with the Social and Product Quality Standards

The audit is carried out at regular interval and product Quality check is being undertaken by them at regular interval

So if you don’t mess up in the following fronts

they don’t cancel or refuse the renewal of license

they designs of Handbags for Spring season (Next March) is also already approved by tommy

The anti thesis prevails as mentioned by you

I’m looking forward to the renewal status by Abhinav Kumar Sir on 16th

Lets hope for the best

Mas financial services ltd give 20-25% guidances for next 5 years…

What if tommy license not renew…

@Venky_Thiriveedhi

nice explanation,

Let me give my take so what happiness is my understanding is the real cash received is in the beginning and the end of the project and in between is all revenue recognition or very small payments.

Like i get 20% as advance now as and when I complete a %of project I am supposed to recognize revenue but I have a understanding that in reality you actually dont get a lot of money in between.

and the best part is in the end till the time I dont get the payment I dont deliver the product, just think about this way that the entire movie gets delayed or is put on hold so it creates a risk for the entire small ecosystem, in this case both parties always try to come up with best solution which benefits both like in ayalaan movie phantom has the distributing rights. (so the possibility of receivables being downsized is also low)

Another thing is suppose I can recognize revenue at 20% completion of a project but by the quatre end I could only do 18% then in this case I am supposed to recognize revenue in next quarter, so by next quarte If I complete 40% I get to recognize entire thing.

another possibility to highlight is since % of work completed is subjective phantom might say I have done 20% of work and recognize revenue but client might not agree and pay in this case the entire thing becomes unpaid revenue but this effect should normalize in the subsequent quatre

BASILIC

In phantom case you work in preproduction so what %of work is done is itself a subjective matter for the company hence the revenue recognition is a bit tricky but in basilic case who work in post production has 15cr of receivable and 15cr of other asset on 53cr balance sheet 56%

PHANTOM

In phantom case 78cr of balance sheet out of 96cr which is 80% is in other current asset, receivable, inventory this is because the delay of ayalaan movie if I adjust that then their receivable+ inventory are just 40% of balance sheet

This 30cr of other current asset and 18cr of inventory will be recognized as revenue (please correct me if I am wrong here) once ayaalan movie releases (30cr of other current asset) and millstone/product is delivered (18cr inventory) so 49cr is what we are taking about.

Of course the balance sheet has been deteriorated + ayalaan successful/timely release is must, so we have to monitor things closely, expecting H2 to be better.

Basilic does not show this berceuse they work on small projects(post production) in phantom case they take like 6motnhs to 9months for a particular project (pre production)

Disc- I would exit this stock if I get to know about any significant developments without a intimating plz invest at your own risk, invested