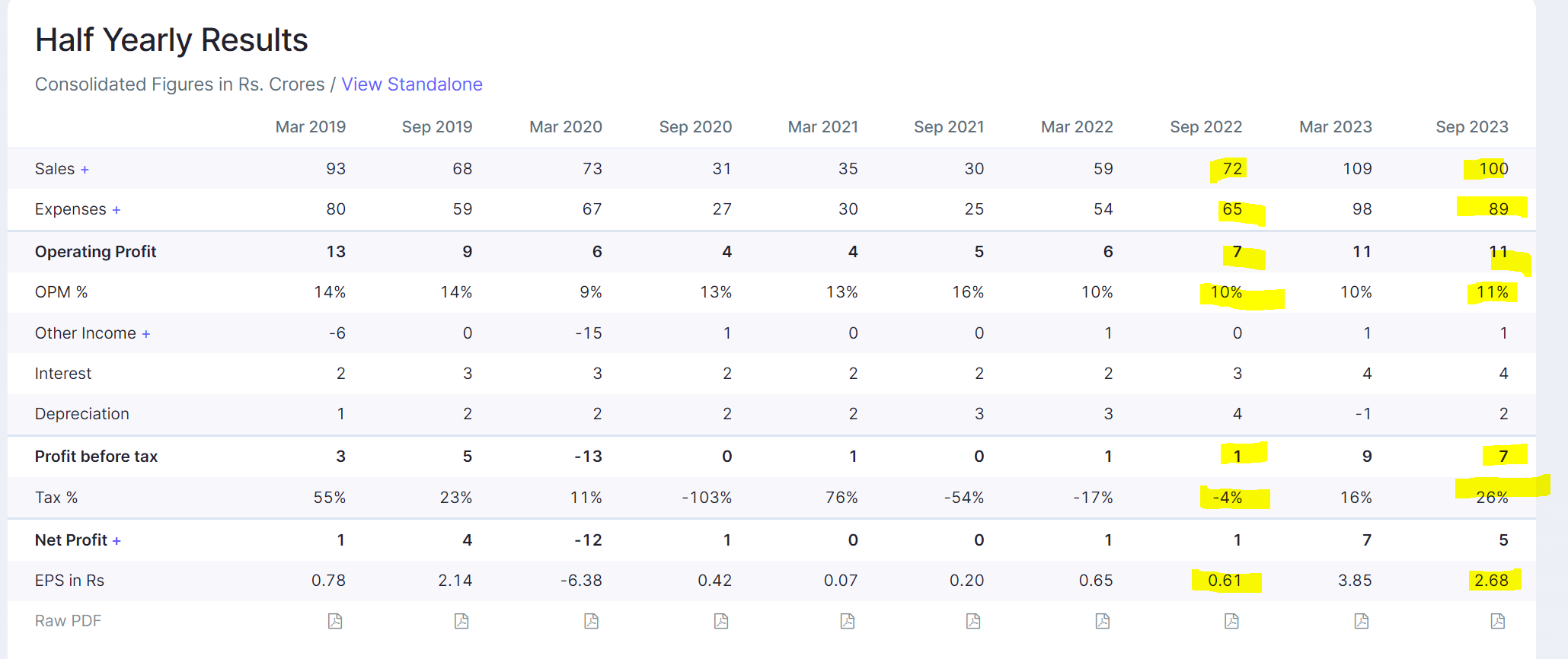

Exceptional Half yearly result, Company is on the right track. Long way to go…

Disc . Invested

Exceptional Half yearly result, Company is on the right track. Long way to go…

Disc . Invested

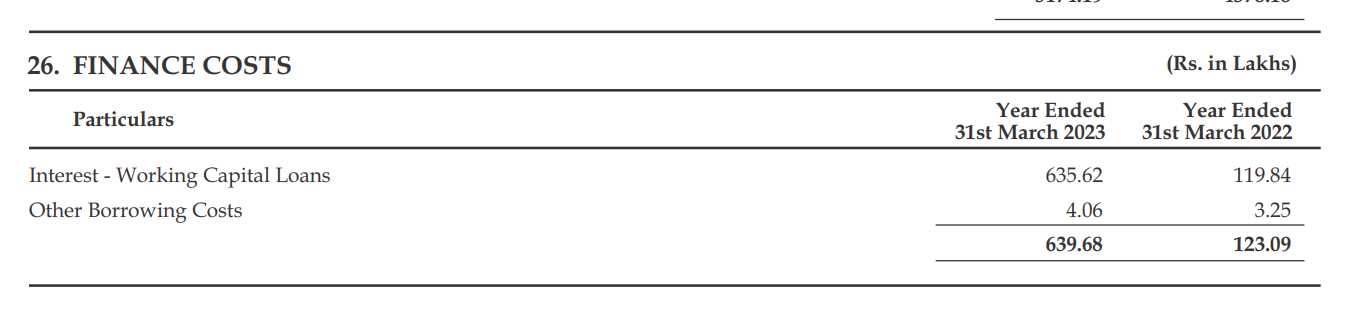

I believe the reference was to Working Capital Loans. See Note 26 in the latest Annual Report as an example.

The short version of my answer is – without any disrespect to the Chairman, I think interest costs have risen simply because interest rates have gone up worldwide – and most definitely in the U.S. I don’t think it mattered whether the reference rate was LIBOR or SOFR. For detailed response, read on.

The interest on most Corporate Loans are charged as Reference + Spread. Earlier, this reference rate was LIBOR. So if LIBOR was 0.5% and the bank decides a spread of 1%, the loan would be quoted at a floating rate of 1.5% (LIBOR being the floating component). Recently, LIBOR has been abandoned and has been replaced by the Secured Overnight Funding Rate (SOFR). More on why LIBOR was abandoned here: What Is Libor And Why Is It Being Abandoned

You can check out recent history of SOFR rates here: Secured Overnight Financing Rate Data – FEDERAL RESERVE BANK of NEW YORK

This clearly show that SOFR rates have moved up from around 0.5% in early 2022 to 6% today. My point is that even if LIBOR was somehow retained in wide global use, interest cost would have gone up because LIBOR will have also risen with the general interest rate increases around the world. Anyway, if it’s any consolation, SOFR forward rates indicates a softnening towards 4% (Source), although it might take a while.

To summarize my personal understanding – any sort of leverage or working capital loan has become quite costly. Energy costs are another reason quoted. All of this aligns with the information from the Management that many of their Competitors aborad had to shut down.

Overall, what is the impact on Ambika?

Increase in Interest Costs from 2-5 Crores to 10-12 Crores. Although that’s a sizeable increase, not much can be done by the company. All the firms in the industry will be suffering from the same issue.

Increase in Energy costs. According to logic provided in this Hindu BusinessLine article, the increase in Energy costs for Ambika could be as much as Rs. 5 Crores. Again, similarly all players in the industry would be facing the same issue. You can find many articles, including this one, where Indian Yarn Manufacturers are protesting the increase in unit prices and even stopping production.

What can/will Ambika do?

The increase in Working Capital cost can be partially or fully offset by passing it on to the customers. I don’t think it’s easy to do that when demand scenario is stagnant. I expect it would be possible once demand picks up, whenever that happens.

Ambika is installing Solar Panels to mitigate the rise in energy costs. According to the Chairman, the company has spent 40 Crs. to install Solar Panels that produce 8.33 MW of power and this will provide them with an IRR of around 10 Crs. per year. In gross for the coming year, 63 Million units out of 78 Million units required for production will be via internal energy generation (Wind and Solar power). The future plan is to take care of the entire energy requirement for production through internal energy generation. (See Chairman’s speech from the 40:23 mark)

Ultimately, in my mind, these minor cost increases are short term pains and not long term detriments. Ignore and move on.

Company maintains their presales runrate, however they weren’t able to launch any new project in Q2 as a result of which most sales came from Life Republic. On reported numbers, they are guiding for 1500 cr. revenues in FY24 and 2000 cr. in FY25. Concall notes below

FY24Q2

Disclosure: Invested (position size here, sold few shares in last-30 days)

Results were muted. Revenue declined. I guess it was expected because loss on the events side of business. Let’s wait to hear mgmt commentary.

Hi, can you please add the source also? It will be useful for everyone if we can start adding more details to the guidance.

Yes ofcourse there is an impact, I meant Basilic’s resukts weee solid despite the strike and despite the fact that over 80% of their business is foreign led and largely skills based.

Phantom on the other hand has a sizable India business too, and so it should be less impacted than Basilic was.

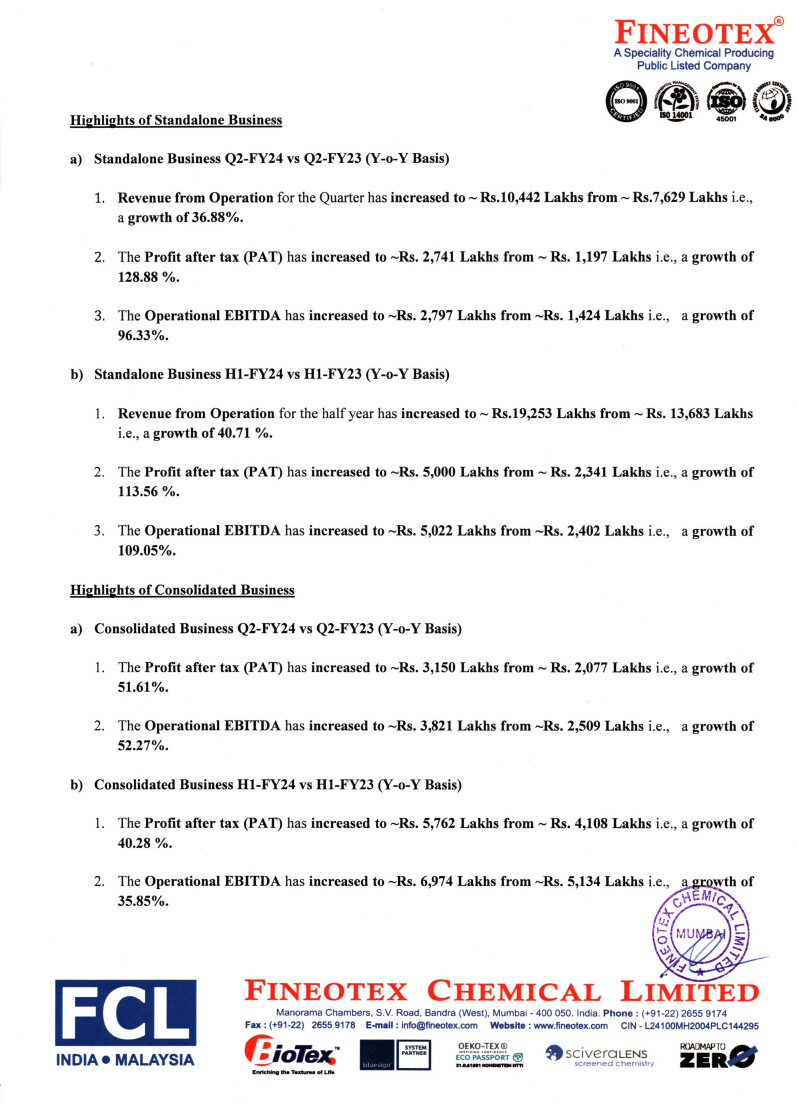

Fineotex Chemical Limited – Standalone and Consolidated Business Performance Highlights Q2-FY24

Standalone Business – Q2-FY24 vs Q2-FY23:

Standalone Business – H1-FY24 vs H1-FY23:

Consolidated Business – Q2-FY24 vs Q2-FY23:

Consolidated Business – H1-FY24 vs H1-FY23:

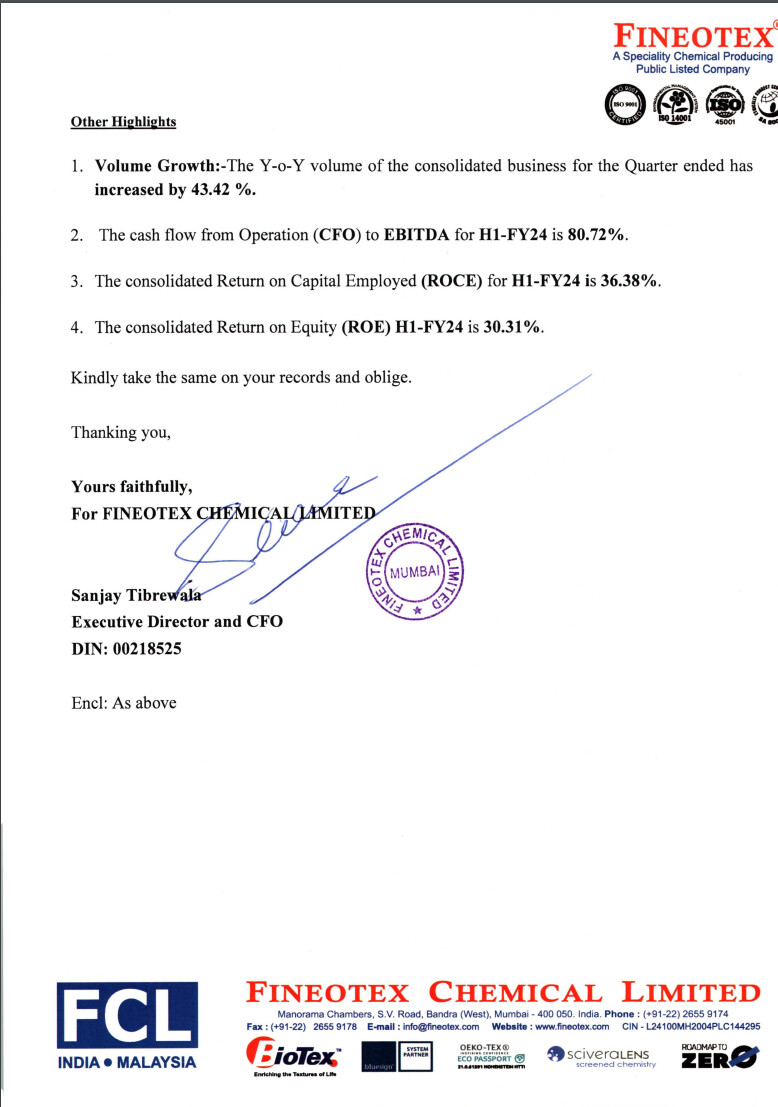

Additional Highlights:

XBRL, PDF, and Excel are all widely used formats for reporting financial information. However, they have different strengths and weaknesses.

XBRL

Excel

Comparison table

| Feature | XBRL | Excel | |

|---|---|---|---|

| Machine-readable | Yes | No | No |

| Consistent format and structure | Yes | Yes | No |

| Efficient processing and analysis | Yes | No | No |

| Interoperability | Yes | Yes | No |

| Easy to create | No | Yes | Yes |

| Easy to read | No | Yes | Yes |

| Portable and versatile | Yes | Yes | Yes |

| Can include images, charts, and other multimedia content | No | Yes | Yes |

| Can be used for complex calculations and analysis | Yes | Yes | Yes |

| Easy to share and collaborate on | No | Yes | Yes |

| Efficient for processing large amounts of data | Yes | No | No |

drive_spreadsheetExport to Sheets

Advantages of XBRL

Conclusion

XBRL offers a number of advantages over PDF and Excel for reporting financial information. It is more accurate, consistent, efficient, and interoperable. However, it is important to note that XBRL requires specialized software to create and read.

Which format is best for a particular reporting need will depend on the specific requirements of the users. For example, if users need to be able to easily share and collaborate on reports, then PDF or Excel may be a better choice. However, if users need to be able to process and analyze large amounts of data quickly and efficiently, then XBRL may be a better choice.

Radiant Cash Management Services Limited (RCMS) Ventures into Fintech with Acemoney Acquisition

Overview: RCMS, a prominent financial entity, has unveiled its strategic move into the fintech domain through the acquisition of a majority stake in Acemoney, a leading Kochi-based fintech company. The Board of Directors at RCMS has granted approval for the definitive agreement, signaling the onset of a significant collaboration.

Acquisition Details:

Founders’ Vision:

Strategic Positioning:

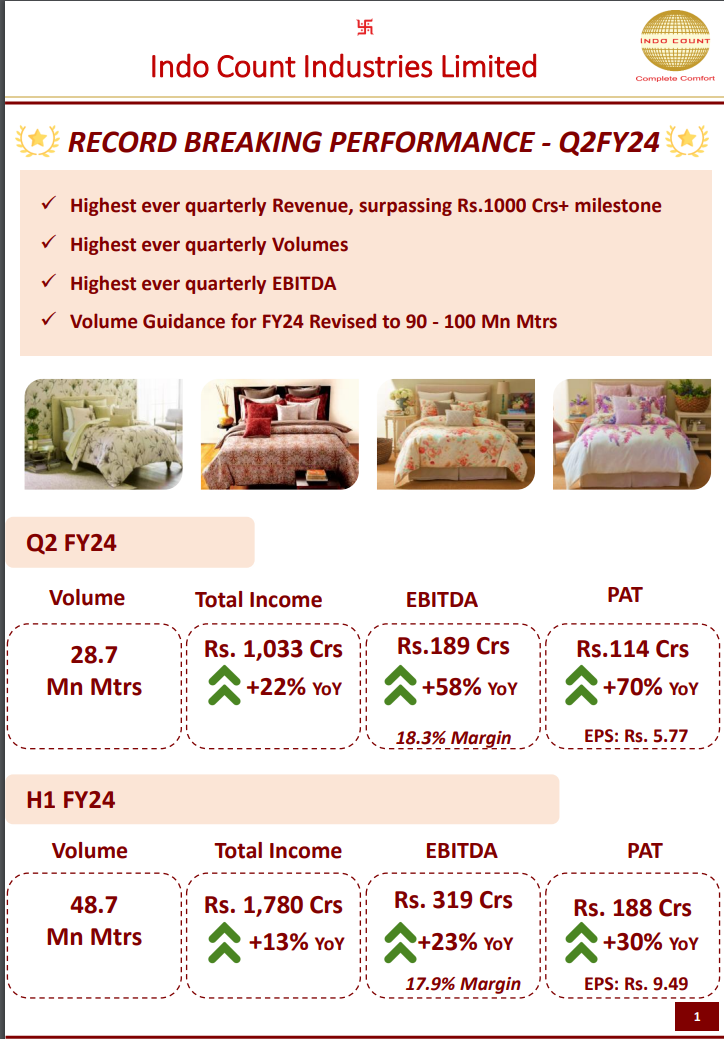

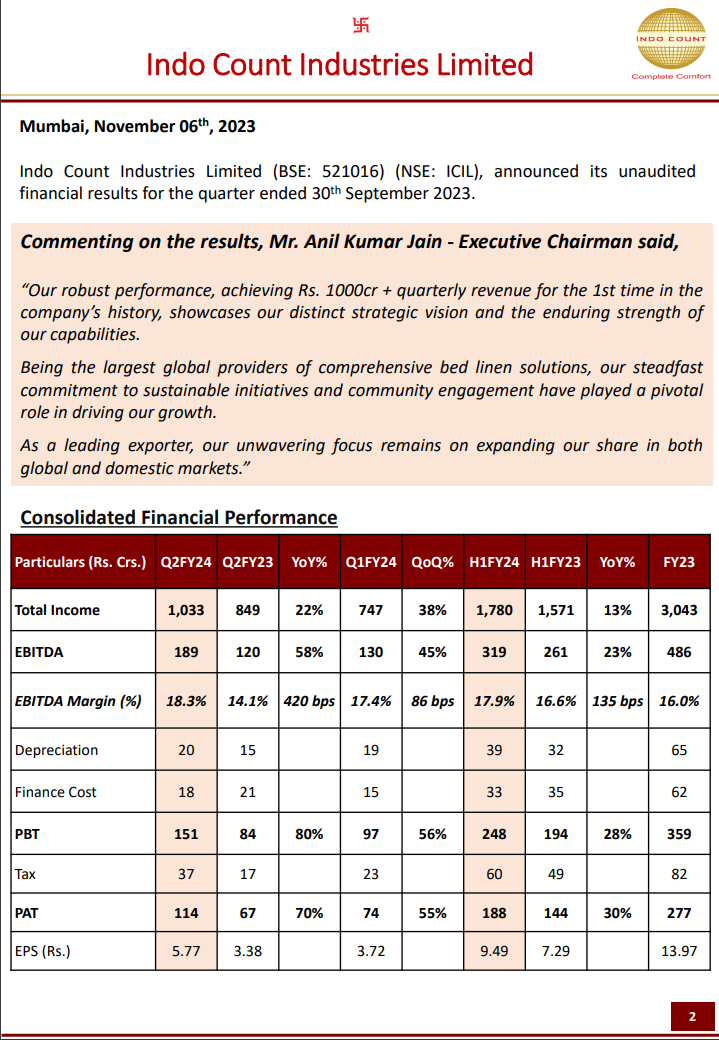

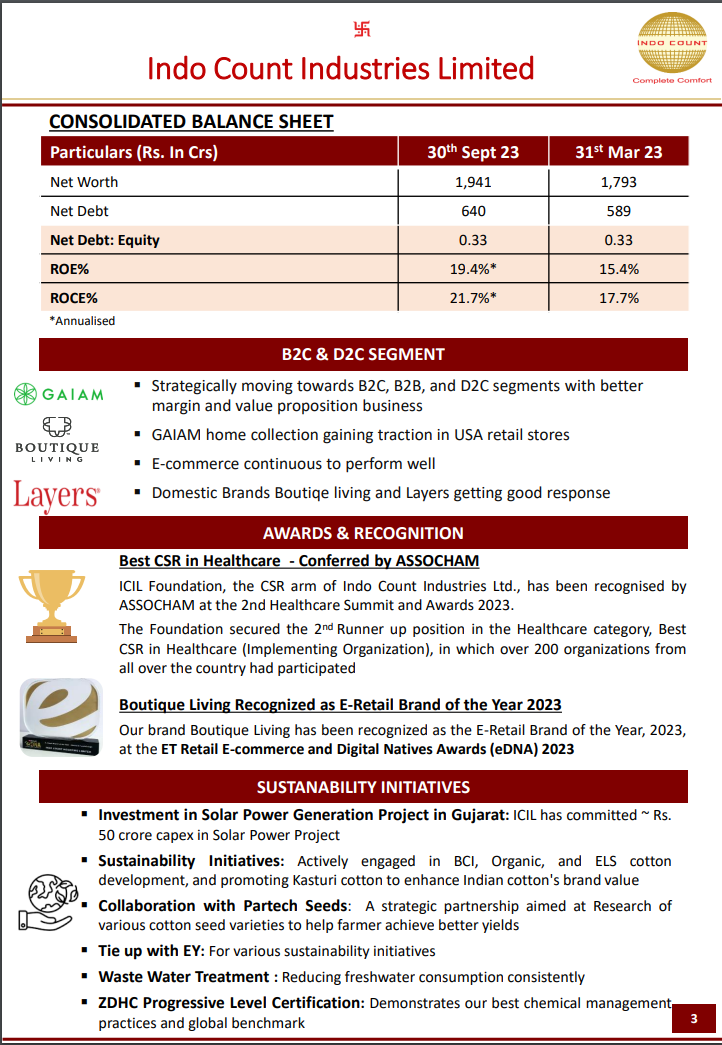

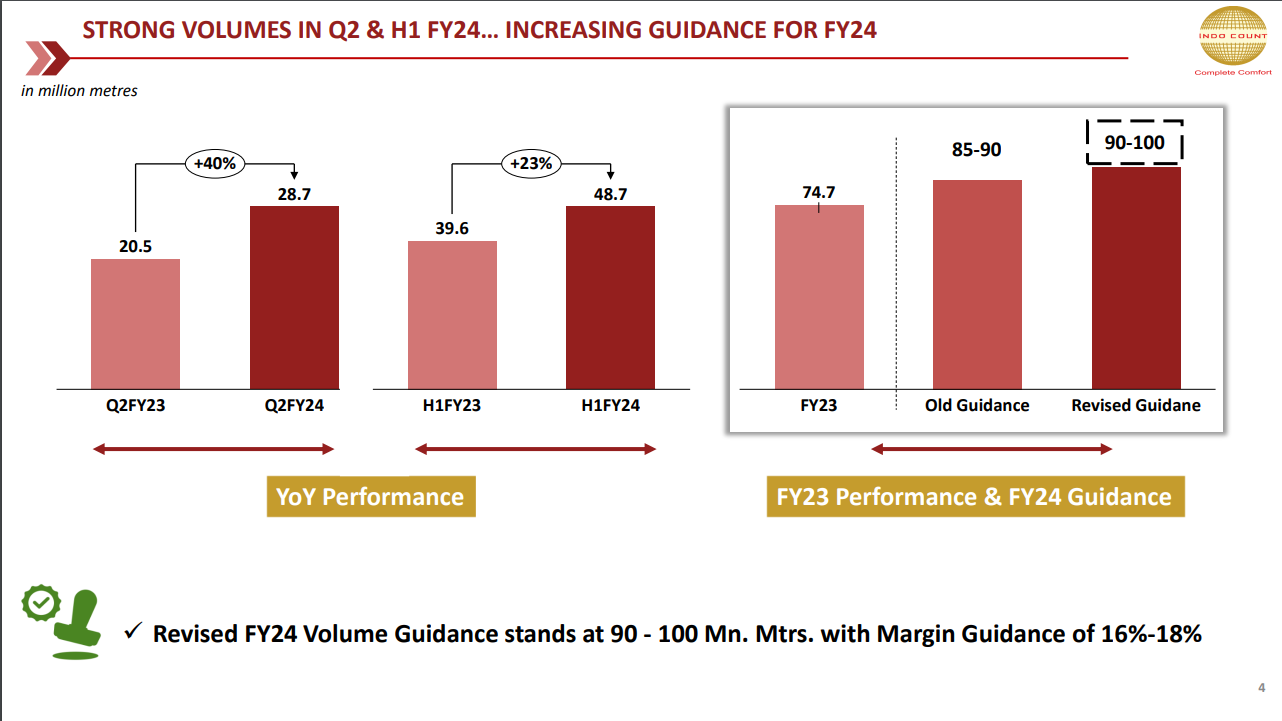

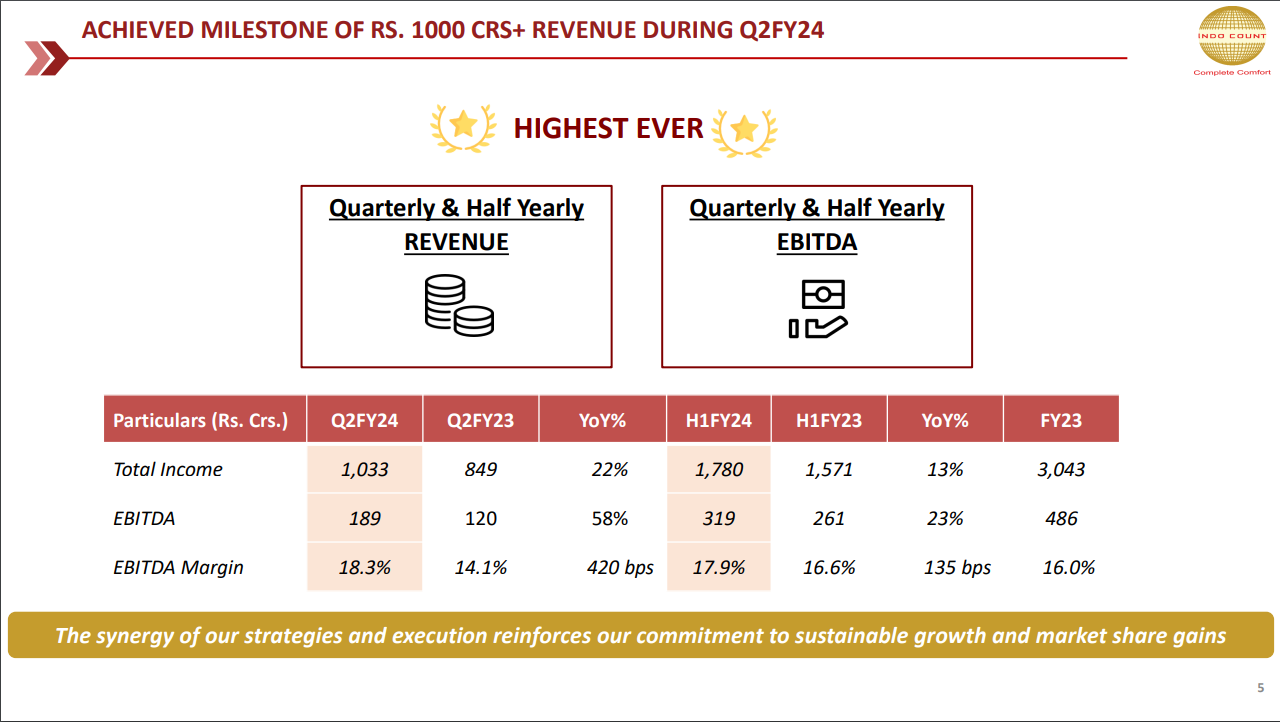

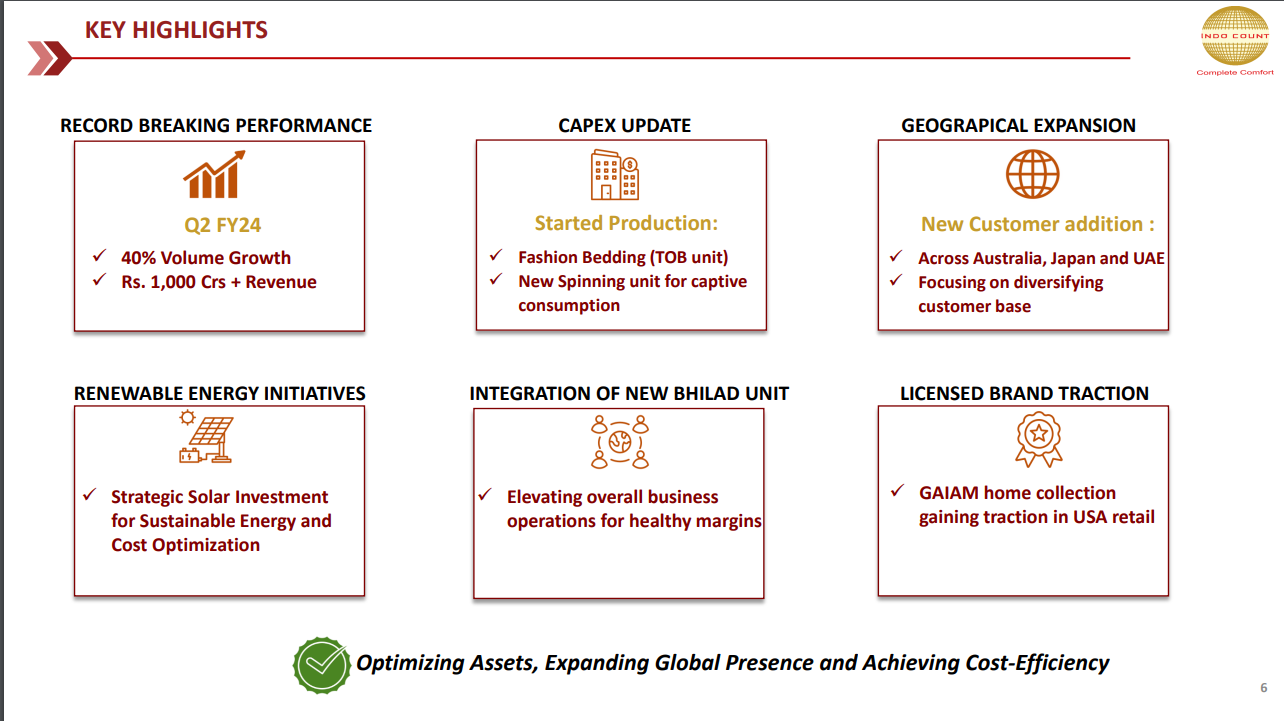

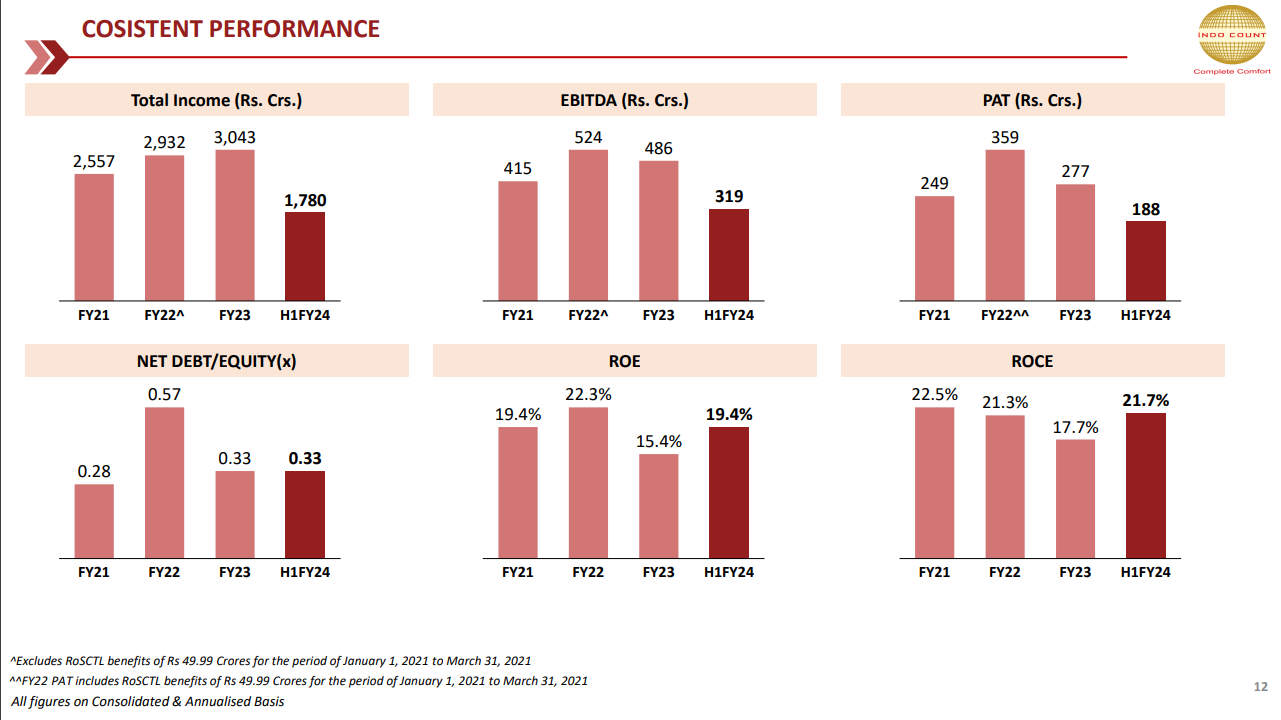

Indo Count Industries Limited: Record-Breaking Q2 FY24 Performance

Key Financial Highlights:

Consolidated Balance Sheet (as of 30th Sept 23):

Strategic Initiatives:

Segmental Highlights: