What I meant is:

If something is sold almost free then getting revenue growth is the easiest part. Isn’t it ? So there is not much to be impressed by the revenue growth rate of DFS. Unfortunately, the revenue for DFS is an expense item for card issuer. So we have to keep his concerns in mind and how he will react to his expenses growing out of line from his core business.

Posts in category Value Pickr

Dreamfolks services limited( DFS) (05-11-2023)

Chembond Chemicals- A Perfect Misvalued Bet (05-11-2023)

Any take on the Q2FY24 performance?

Revenue has stagnated for last 5-6 quarters but operating margins are improving. What could be the other income component as that is significant this quarter.

Cupid Ltd – Helping the world play safe! (04-11-2023)

Next Conference Call, with the new Management Team, will be held on 09 Nov 2023 (Thursday).

If someone can take short notes and post here, it would be great.

Thank you in advance.

Also it seems that indeed, Mr. Garg will be retained in capacity of Senior Advisor, which is icing on the cake.

Krishca Ltd : A SME offering steel strapping Solution (04-11-2023)

Primarily due to the expenses related to setting up the 2nd plant. I might be wrong but thats what i understood from the cash flow statement.

Titan Biotech Limited (04-11-2023)

Good report on protein hydrolysate market, nice to see Titan biotech having a significant global market share in this niche market.

Disclosure: Not invested (no transactions in last-30 days)

SmallCap Hunter : Trying to find the dark horses with triggers (04-11-2023)

Anyone tracking IFL enterprise ltd. Recently they have won loads of export orders for paper supply . They also have signed on Australian firm for joint venture .loads of positives but stock price falling . Any views

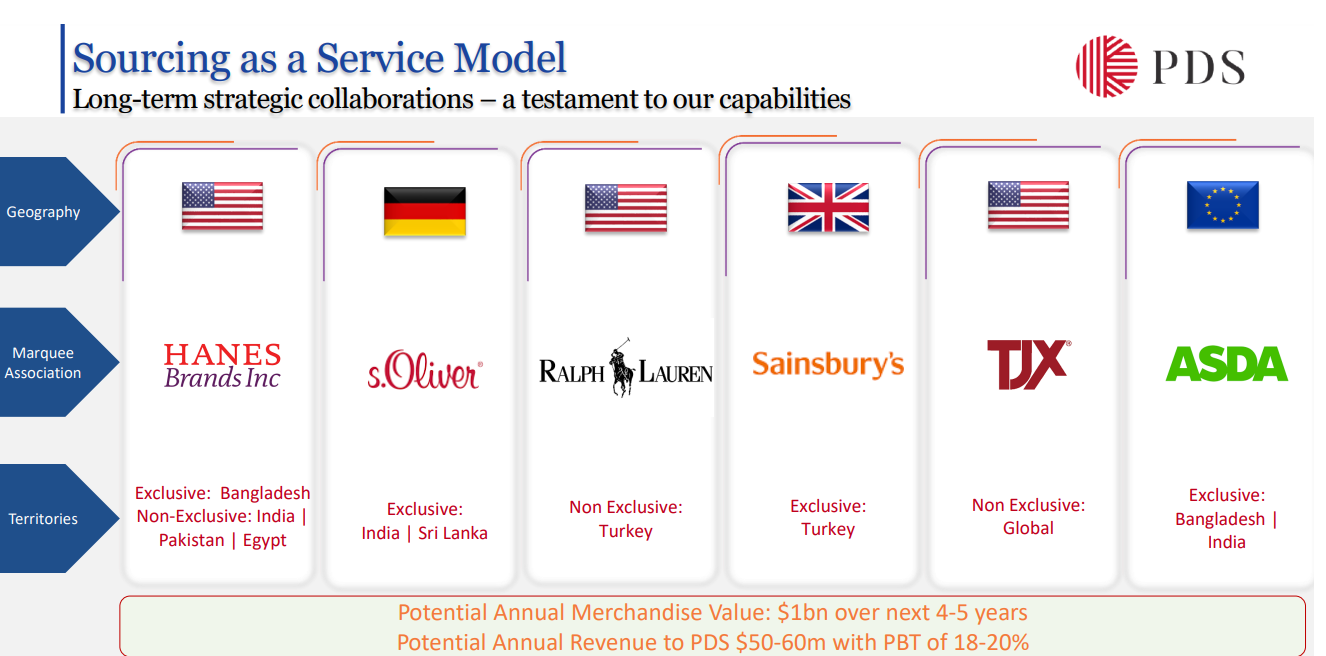

PDS Limited – A platform for entrepreneurs (04-11-2023)

Hi @Chins , Great write up on this company.

I have few questions on the numbers: If anyone can help here:

Design led sourcing segment:

Should One think it has happened because of JV turnaround of margins from negative to 4 – 5% margins ? 80 – 300cr pat in last 3 years ? Design led sourcing PBT are sustainable that means this 300cr PAT will be sustainable going forward ?

Coming to Brand Management and SAAS:

Brand Management → As you said it is 250-300CR EBITDA Opportunity.

SAAS → 200 cr PAT Annually.

How this numbers are achievable ?

For example: Attaching the below screenshot:

It says potential revenue of 350 – 450cr annually and PBT of 18-20% i.e 70 – 100 CR PBT.

Likewise, on Ted Baker monthly revenue is shown below:

Roughly if I take up monthly 50-60cr so annually it comes around: 350-400cr.

and PBT as – 35cr.

Based on current deals: SAAS and Ted baker deal ~ New offerings it is on annualised basis PBT of => 35 + 70cr => 100cr – 120cr PBT Annually.

Above are for Fy24/25/26 annually for current order wins.

For long term horizon: (Not looking on QoQ)

On 500cr-1000cr PAT in next 3 to 5 years.

According to me, this can be achieved with more deals. Current deals won’t make them achieve 1000cr PAT and their top 10 verticals needs to be scaled up. That needs to be seen. (More revenue from poetic gem etc…)

Huge respect for Pallak to create PDS like platform. His journey has been inspiring. Looking forward as Pallak said, company is at inflection point.

Below snapshot:

Thanks for writing the thread @Chins Your work on this has been amazing !!!

Anywhere my understanding needs to be corrected. Do correct me.

Thanks.

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (04-11-2023)

State textbook orders are savers for this company.

Aavas Financiers :: Banking on the unbanked (04-11-2023)

We need to give time to Aavas Housing. There are two challenges

A) New Management

B) Lack of systems in place (specifically IT system) , this is evident from the fact that Turnaround time is approx 10 days .

Both of these challenges are getting addressed.

What makes Aavas an elusive HFC , vis a vis it’s competitors is it’s Pan India presence and outstanding underwriting.

In fact, in the management call , Sachin sir has said that both the issues will get addressed.

Tech implementation would be completed by FY24 . This will make the complete functions seamless, this reducing the TAT. Company has engaged consultants of repute to solve this.

Guidance

A) Medium term -20 -25 %AUM growth and margin 5 percent plus.

B) LONG TERM DECADAL AUM -1LAC CR (Refer to Page 8 of Annual Report)

I am really very positive on Aavas .

Cera SanitaryWare Ltd (04-11-2023)

hi, @harsh.beria93 , You have been following this company from long time. I think , you also used to hold around 3% of your portfolio in 2020 around. From that time onwards, most of your posts have been positive and encouraging, but you have disclosed that you dont have investment in it anymore. I am curious to know, whats current position and what must be the reason to sell this company while continue following it with favourable posts. Are you considering buying it back? at todays valuations, how it appears to you?