Please can someone elaborate on what basis should we plan our exit in this stock, how to keep a track of it and plan your exit as it is cyclical.

Thank you.

Posts in category Value Pickr

Jindal saw – Another beneficiary of India’s growth story (30-10-2023)

Praveen’s Portfolio (30-10-2023)

Thanks for your thoughts on your portfolio.

Do you feel that XPRO India is expensive at current valuations of 50PE around

CL EDUCATE – Less Down side and unlimited upside (30-10-2023)

Had an insightful meeting in Delhi with Career Launcher management last week.

- CUET exam : more the states where central govt comes in power, more the adoption of CUET entrance exam. Currently a 11cr biz, can scale to 100 cr + in coming years. Opening centres in smaller towns with teaching in the regional language can be a big moat. CUET is not tested only in English.

- Demerger of Martech being evaluated even now as was asked on last investor call. Management understands the ROCE benefits by focusing only on edtech.

- Student mobility: by offering the test prep + admission counselling services into colleges worldwide, CL can achieve geographic expansion as well as cover whole spectrum of counselling, visa etc. This cross sell opportunity can be big in the future.

- Buyback ends on Nov 28th.

- With a net cash balance sheet of 100 cr + cash in a 420 cr mcap co, promoter is continuing to evaluate opportunities to use this cash

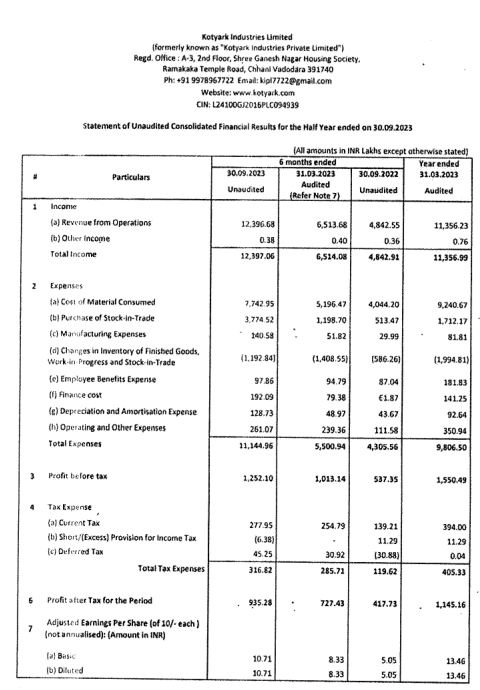

Kotyark Industries – Only Listed pure Biodiesel Player (30-10-2023)

yamuna is not yet consolidated

Also execution is not linear when i spoke to few biodiesel players. It is as per OMC schedule.

Disc : hold no position yet, evaluating

RACL Geartech Limited (30-10-2023)

in the area mentioned (paint shop) yes but the remaining field was still vacant. No civil works nothing yet. The yellow area (paint shop shed) had Civil work and steel columns setup already.

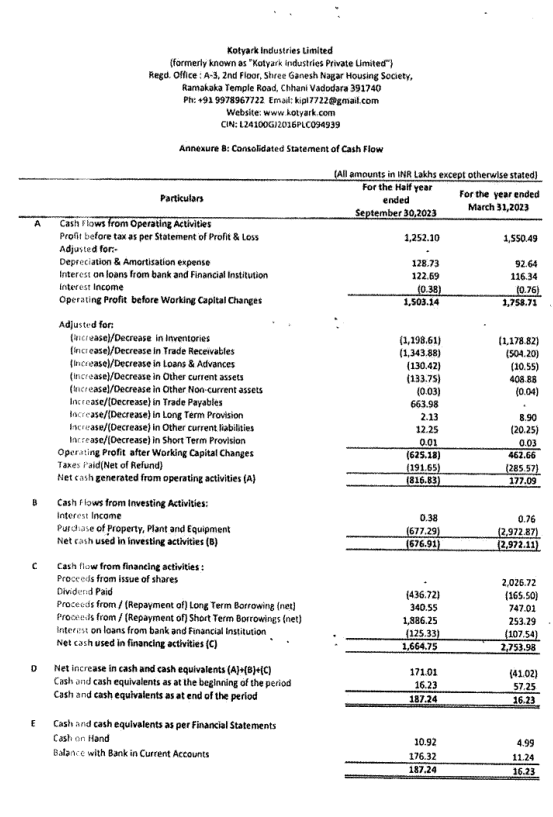

Kotyark Industries – Only Listed pure Biodiesel Player (30-10-2023)

I do not think Yamuna is the reason. Company had announced two tender wins for Q1 and Q2. Even excluding Yamuna those tenders should have led to revenues of 270 crs (116 crs + 154 crs) for Kotyark standalone in H1. Against this expectation, the revenue was reported at Rs 124 crs. Goes to say that winning tenders doesn’t necessarily translate into revenues.

Also the CFO resignation is a dampener. In the last 15 months this is the fourth resignation of a KMP. Two company secretaries resigned within 3 months of each other (one in Jul 2022 and the other in Oct 2022). The earlier CFO resigned in Aug 2022. Goes on to say that the promoters might not be that easy to work with or there is something else behind the scenes.

Disc: exited my position today

Kotyark Industries – Only Listed pure Biodiesel Player (30-10-2023)

From All time high to 16% down.

Kotyark has a wild day.

Profit & Loss looks good but Cash flow doesn’t look good.

Sales in current Half is more than PY whole year.

Reg_30_outcome_of_BM_30_oct_30102023134804.pdf (nseindia.com)

Capex is completed as per Balance Sheet.

Working cycle is absolutely stretched and funded by ST borrowings resulting in the increased Finance Cost.

NP ratio is lower.

Net Profit Ratio:

| H1 FY24 | H2 FY23 | H1 FY23 |

|---|---|---|

| 7.54% | 11.17% | 8.66% |

On Another Thought, the consolidation with Yamuna might be the reason.

Yamuna had high sales with very low margins.

I don’t know whether the related party approvals in AGM have already impacted the P&L in H1, but they shall definitely impact margins of H2.

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (30-10-2023)

If we compare batteries with Hy FuelCell or Hy ICE for mobility space.

The batteries have clearly won the race. With my limited understanding , Hy FC or Hy ICE wont be able to compete with batteris anytime soon.

Battery enjoys The economy of scale and chinese scale of manufacturing.

But both are fundamentally different technologies and Hy FC & ICE becomes necessary/advantageous over battery, for specific applications.

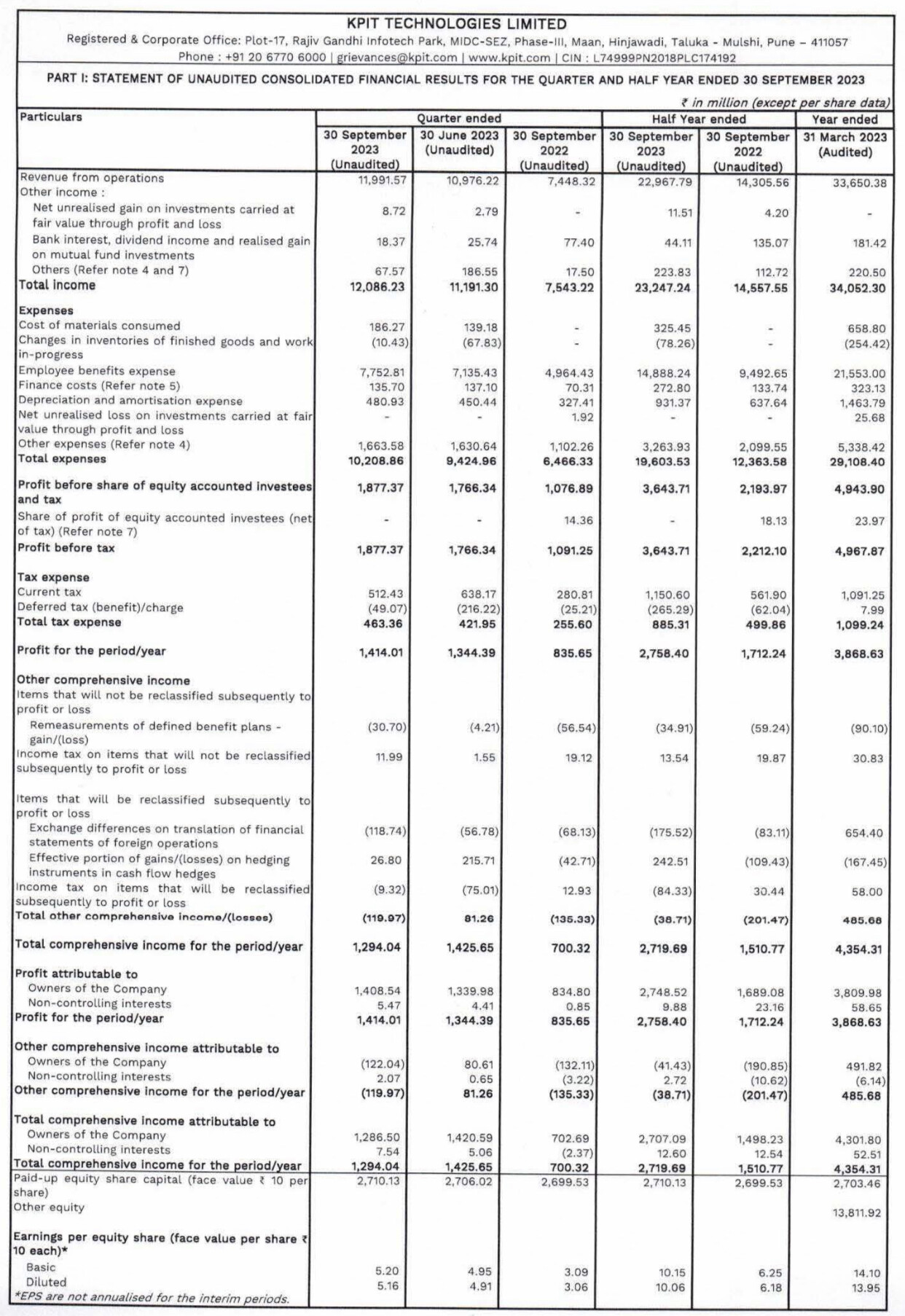

KPIT – CASE (connected, autonomous, shared, electric) – Focused Automotive Play (30-10-2023)

While LTTS results were flattish, KPIT delivers yet again. Keeps shining in the ER&D category