Can any body who has technical know how advise regarding the significance of these patents and potential products or revenue which Company can generate in future or outcome of theses patents vis a vis existing technology…

Posts in category Value Pickr

Simple strategy with back-test results (24-10-2023)

Thanks for the write up. I completely agree with you. This was in no way a recommendation to solely use this method to invest in stocks, rather I was intrigued with the simplicity of the method and wanted to share with the group the results I got with back-testing.

Over the past years, I learnt and again that with my experience in the market, that there is no simple way or a defined way to make profits. I now normally use the best of the both worlds – technical and fundamental to invest. Technical analysis such as 52 weeks high, ATH, stage analysis, MM trend etc. gives me the ideas about the stocks which are in momentum and looking good technically which means that all the expectations are already built in the price. This is kind of stock screener for me. Once I have few ideas, then I evaluate all those stocks independently on my own valuation template which I have built over the years to find out if the stock is over-valued or under-valued along with many other parameters such as EVA, ROIC, reinvestment rate, ROIIC etc. Acquirer’s multiple is one of those parameters. This further refines the universe for me. After that I do some bit of qualitative research to understand the business and management quality and outlook. If the business is simple enough to understand, management is capable and it has good clientele and good competitive advantage, I then invest in that stock and then forget about it until technical charts give me major red warnings or sales / OPM starts falling down.

Windsor Machines Ltd (24-10-2023)

Market Cap : ~500cr

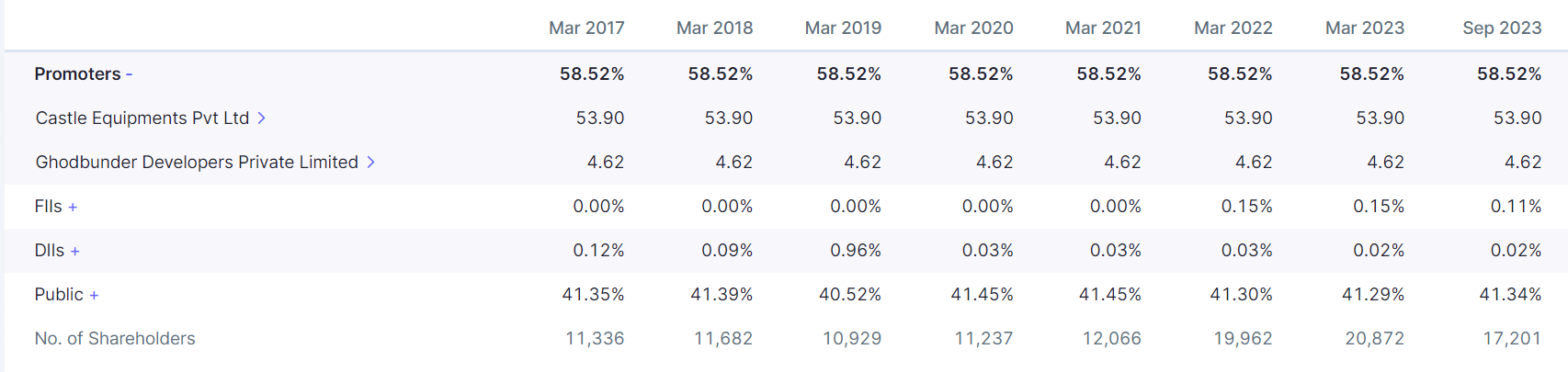

Promoter Holdings: 58.5%

Debt to Equity Ratio : <0.2

ROE = 1.65%

ROCE = 6.77%

Windsor Machines Limited was incorporated in 1963 as a private limited company under the name Windsor Engineering Pvt. Ltd. It became a public limited company in 1964

The company manufactures plastics processing machinery, including injection moulding machines, extrusion lines, and blow moulding lines. The company’s factory at Thane commenced production in 1964, and its factory at Vatva (Gujarat) started production of extrusion lines in 1985.

Windsor Machines Limited is a leading manufacturer of plastics processing machinery in India. The company exports its products to several countries. In 2023 the company tunred announced it’s 60th Annual Report.

Glimpse of About Windsor machine from the Annual Report 2023

We have always been a solution-based company for the last 60 years. From creating our first machine that redefined the plastics industry, we have grown into a Company that is touching everyday lives in more ways than one. At the onset of our journey towards the next half century, we are perfectly poised to create greater value for each interacting partner.

We are reckoned as one of the select few companies in the world, serving and supporting the varied needs of plastics processing industry across 65 countries with an installation base of over 30,000 cutting edge machines with latest technologies.

Our key business verticals include

- Injection Moulding

- Pipe Extrusion

- Blown Films Lines (All under one roof.)

Injection Moulding

Injection moulding finds extensive application in the manufacturing of automotive, white goods, construction, furniture, houseware, smartphones, tablets, laptops, connections, sensors, and various other electronic components. These components require a high level of precision and quality, attributes efficiently provided by injection moulding machines. As a result, injection moulding has become the fastest growing end user category during the projection period, with a commendable Compound Annual Growth Rate (CAGR) in excess of 10%.

Additionally, the increasing awareness regarding personal hygiene and the popularity of organic personal care products are anticipated to boost the consumer goods industry. Consequently, this positive trend is expected to drive the demand for Injection Melding Machines (IMM) in the production of various consumer goods.

Pipe Extrusion

The PVC pipes industry has been categorized into agriculture, building & construction, telecommunication, and other segments based on its end users. As of 2021, the agriculture segment held the largest market share, primarily driven by the rapid adoption of PVC pipes in agriculture irrigation systems. Additionally, the increasing focus on improving the agriculture sector through government initiatives and the growing preference for organic products are expected to further fuel the demand for PVC pipes in this segment.

Looking ahead, the building and construction sector is projected to witness the highest growth rate. This growth is attributed to the numerous advantages of PVC pipes in construction and building applications. The use of PVC pipes in roofing and flooring offers a safe and cost-effective solution, making them a popular choice in this industry. These factors collectively contribute to the continuous expansion of the building and construction segment within the PVC pipes market. The Jal Jivan Mission (JJM) to get potable drinking water to each home has exponentially increased the demand for the HDPE pipes.

Blown Film Extrusion Industry

The global blown film extrusion machine market is experiencing significant growth, driven by the increasing demand for packaging films in the food and beverages sector. Blown film extrusion machines are versatile and cater to both barrier and non-barrier packaging applications, making them highly sought-after in the industry. Additionally, these machines enable the processing of a wide range of polymers, further fuelling the expansion of the global blown film extrusion machine market.

The market segmentation of blown film extrusion machines is based on machine type, material type, application, and geography.

In terms of material type, the market is divided into LDPE (low-density polyethylene), HDPE (high-density polyethylene), LLDPE (linear low-density polyethylene), polyamides, and EVOH.

On the other hand, the application segment includes food and beverages, consumer goods, and pharmaceuticals. Within the food and beverage category, there are further subdivisions like bakery products, dairy products, and frozen food and beverages. Moreover, the global blown film extrusion machine market is classified into semi-automatic and automatic blown film extrusion machines based on machine type.

Company’s association with few of the market leaders in the world like Kuhne GmbH (Germany), and the acquisition of Italtech (Italy) has enabled us to build technological excellence and rise rapidly in the competitive world. As a leading machinery supplier with lowest running cost (per kilo of polymer processed).

Indian plastic machinery is growing at a pace which is double than the average growth at which the economy is growing and is the fastest growing capital goods sector. Strong growth projections in automotive, construction, infrastructure, white goods, rigid and flexible packaging and Government schemes requiring more plastic products like Swachh Bharat, Jal Jivan Mission etc. will push continue to generate strong domestic demand for the Plastic Machinery

Interview at one of the biggest exhibition

An Exclusive Interview with Mr. Vinay Bansod of Windsor Machines Limited by Pratyush Bhaskar, MPTV

Client List

- Sunshine Plastic Industries

- Worth Plastics

- Suraj-logistix Pvt.Ltd

- Creative Polypack Pvt.Ltd

- Vaibhav Plasto Printing & Packaging Pvt. Ltd

- Prince Pipes

- Maxpro Plast India

- Kalpaka plastics Pvt. Ltd.

- Apollo Pipes Limited

- Gupta Polytubes Pvt. Ltd.

- Hari Udyog Pvt. Ltd.

- Ohm Pipe Pvt. Ltd.

- Shiva Polytubes Pvt.Ltd

- Rihno Plast

- Shree Mother Plast (India) Pvt Ltd.

- Shree Plastics

- AKG Industries

- Associted Pipes Industries

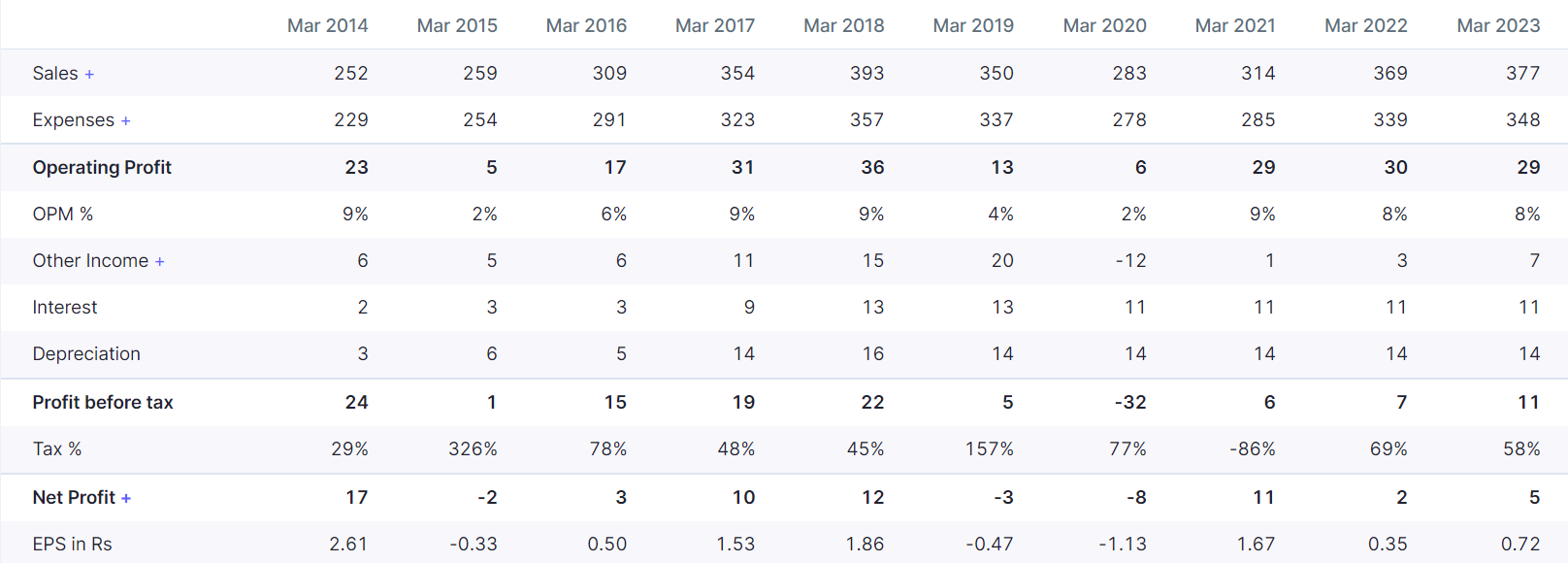

Financials:

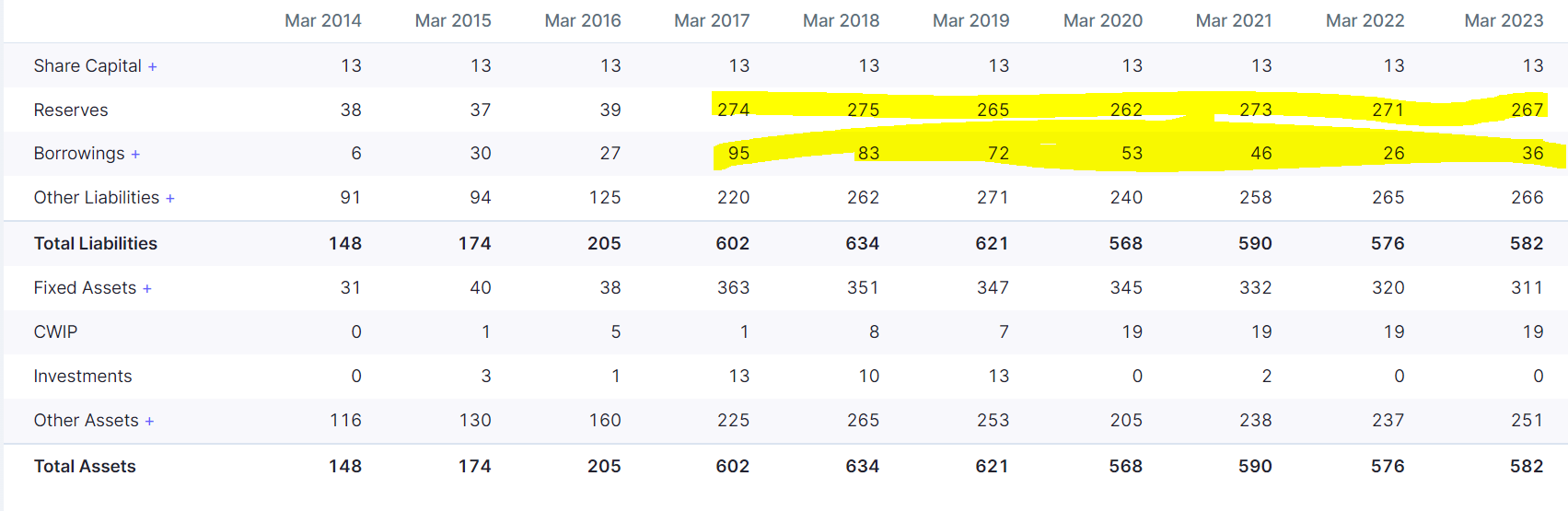

Balance Sheet

Share Holding Pattern:- Not seeing any movements here

Technicals:

Stock is about to give a breakout on a monthly Time Frame (approx after 6 years the stock is crossing current levels)

Please feel to contribute more by identifying red flags or more supportive data pointers

Disclaimer: Invested very small… definitely on radar to add more.

Amit Singh Learning page (24-10-2023)

ICICI Bank is the new HDFC in making.

ICICI Bank- Mar Cap Rs. 6.5 Lakh Cr, CMP 930, P/B 3.02, Annual Rev TTM Rs. 1.42 Lakh Cr, Cost of Fund 4.69

HDFC Bank- Mar Cap Rs. 11.41 Lakh Cr, CMP 1506, P/B 2.9, Annual Rev TTM Rs. 2.18 Lakh Cr, Cost of Fund 4.8

Post change in ICICI Bank Management focus and ease in doing business has grown.

some points;

Customer 360 is the approach of the bank.

- Evolving needs of customer

- Decongesting Process- Removing Redundancy helped bank to reduce response time, Leveraging power of subtraction in Service delivery, Abolition of non value adding process. (Video KYC, ILens for online loan approval, etc…)

- Re Orientation of Technology

- Agile HR practice- Job Rotation and moving across roles,

- Fair to Customer Fair to bank

Multidimensional approach to bring entire bank to the customer requirement and its eco system

Product and Service to meet banking requirement of Individual customer at every life stage.

Digital Platform has helped in Customer profiling and Banking need, helping cross sell/ up sell products by ICICI bank

Salient Point:

- Credit Card Spend grew by 60% in FY23

- 29% market share in Fastag

- Supply Chain finance grew by 56%

- Their lending in five segments:

a) Retail- Is growing QoQ 6% at Rs. 6148 Billion, segment growing 18% YoY

b) Rural Loan- Growing at 4% QoQ Rs. 937 Billion, segment growing 15% YoY

c) Business Banking- Growing at 11% QoQ Rs. 828.33 Billion, segment growing 40% YoY

d) SME- Growing at 7% QoQ Rs. 542 Billion, segment growing 15% YoY

e) Domestic Corporate and Others- Growing at 3% QoQ Rs. 2489 Billion, segment growing 12% YoY - Focus on SME and Business banking growth.

- Net Interest income grew by 23% Q2 YoY and Core operating profit by 22% at Rs. 136 Billion.

- PAT increased by 35% Q2 YoY to 102.61Cr.

- Overseas Non India linked corporate portfolio reduced by 29% to ~Rs. 95 Cr.

- Cost of Fund has increased from 3.93% to 4.69%, HDFC cost of fund is 4.8 in Q2 FY24

- Avg CASA is 40%, dip of 5% YoY and 2.6% QoQ.

- NIM of ICIC is 25.2% compared to HDFC 21%. ** HDFC pre merger was at 38% to 35%.

- QoQ Total Rev Growth is 5% Q2 FY24 and last 4 Qtr 7% Avg, compared to HDFC, 38% (post merger) and 8% (Pre Merger).

Sona Comstar BLW – Direct EV Play (24-10-2023)

Tomorrow its Q2 numbers will be announced. Any idea what the market expectation was about its revenue/profit numbers?

Simple strategy with back-test results (24-10-2023)

I know that there are many gaps in my knowledge, and those gaps are as wide as they come, but I am not too sure, if one can invest in a company for long term based on ratios, other than what are usually looked at to analyze a business.

I do acknowledge that there must be a lot of merit in creating and presenting such ratios or concepts, which sometimes could be beyond my current understanding, but from my limited knowledge and experience, what the market participants think of the business, who are very different groups, but arrive at the same conclusion of either moving the price up or down, play the bigger role. So while such ratios are intriguing, they may not work as anticipated and may test our patience. I don’t know if the line between a value buy and a value trap is thin.

I also acknowledge the fact and the beauty of purchasing something less than its value, and see it becoming profitable. The thought of looking at such opportunities cross my mind sometimes. Sales, profit, cash flows, dividends, all are in place, it is just the price that feels wrong.

And if I remember correctly, I did buy something, looking just at its ratios, and paid dearly. I think I read a comment along the lines of, numbers are past, or they reflect the business up to that point etc.

Just my thoughts, presenting my views for my own benefit and clarity. No intention to curb your enthusiasm, I am enthusiastic myself. We can create our processes and philosophies from many varying sources, different schools of thought and multiple disciplines.

Steel Strips Wheels Limited – Attractive Valuations (24-10-2023)

Recently started following the company, no investment as of today. The company looks impressive with high growth potential, increase in margins, operating efficiencies, and good market standing. However, there are few questions still troubling me here

-

The market share figures in each segment are

PV – 50%

MHCV – 53%

Tractor – 44%

OTR – 70%

These numbers have remained constant across quarters for 2-3 years. In every ppt, there is almost zero deviation from the numbers. I find it very strange. There has not even been a 1% movement in any category for years. Their client-specific business share exactly the same across quarters as well.

-

For 4-5 years, investors were expecting margin improvement from alloy wheels and exports but not much improvement in numbers here. Covid and inflation might take some blame here though.

-

The negligible presence of FII/DIIs for a 4000 Cr. company raises some concerns.

Hoping to get some answers here

HBL Power: Signs of change (24-10-2023)

Some notes from the above article that I received as a WhatsApp forward.

-

Exposure to sub-zero temperature and oxygen-deficient atmosphere freezes the fuel and lubricants and impacts the mechanical efficiency of the platforms. The hydraulics, electronics and batteries of the heavily sophisticated platforms are also impacted. Pure Lead-Tin (PLT) batteries, superior to existing Lead-Acid batteries in negative temperatures, are being tested and will be implemented in all vehicles. At the operational and tactical level, introduction of specialist equipment to include rectifiers, PLT batteries, utilisation of specialist grade FOL (fuels, oils, lubricants), preventive maintenance and development of best practices have enabled operational readiness of 95 per cent, which contributes significantly to the operational preparedness of the Army.

-

These are being used for trucks and are being tested for heavier armoured vehicles. These batteries deliver high current and are vital for starting tanks in extremely low temperatures.

Power grid – a superior alternative to Invits (24-10-2023)

Hi all, I’ve just done an updated valuation on Powergrid, and it seems to be a compelling long term investment at current prices.

Powergrid (NSE: POWERGRID) owns and operates 45% of India’s electricity transmission network. It meets all the criteria for a good long term investment:

- Moat : the dominant player in transmission. Has 20~30 year contracts with assured ROEs. Is the government’s preferred vendor for large scale or complex transmission projects

- Long growth runway : increasing Indian power consumption and massive investments in new renewable power generation capacity

- Management execution : consistently exceeded regulatory benchmarks with 99%+ transmission system availability and demonstrated ability to execute large scale projects over the last decade

- Attractive valuation : limited downside possibility at current prices, with attractive returns on the upside. Risks to the growth trajectory: regulatory regime and tariff changes, competition by private players and fraud / corruption.

Please let me know your thoughts / feedback

Valuation model (base case): 20230917_PowerGrid_analysis_ to share – Google Sheets

To get a sense of each project’s unit economics, I also looked at the ROEs on their InvIT projects based on FCF and equity value:

disc – invested, this is not a buy / sell recommendation