I am interested… Kindly add me

varmarahul76@gmail.com

Posts in category Value Pickr

Zoom webinar on stage investing (12-10-2024)

Indigo Paints: Upcoming Star (12-10-2024)

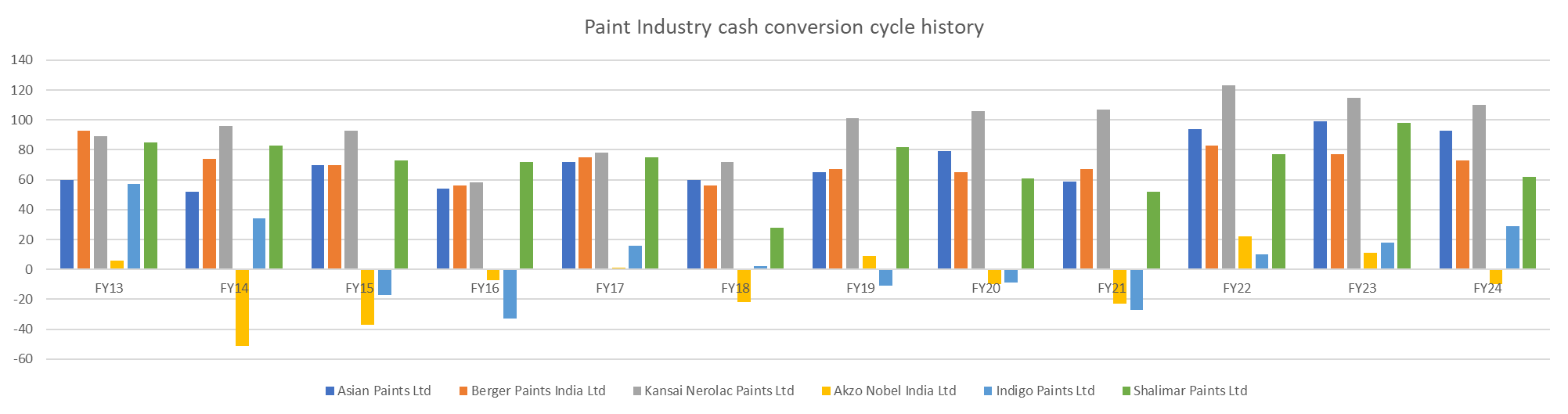

I believe the chart is self-explanatory in identifying the most efficient player in the paint industry when it comes to working capital management.

Stop the Count – US Policy impact on Indian Equities (12-10-2024)

Starting this thread to analyze the impact USA Policy changes have on Indian Economy and Equities. Though it’s no use trying to predict winner of an Election, or speculating the policies they might bring, once the event happens, we can be better prepared if we analyze it.

Historically, market sentiment goes bearish if there’s a regime change, and then gradually recovers. This is because market loves continuity of policies and fears uncertainty – which is often temporary.

IT & Pharma:

- They are export heave sectors in India, are most impacted by election outcomes.

- Trump favours a 20% tariff on all imports from outside USA, and 60% for goods from China.

- Trump has also criticized India’s import tariffs, and had vowed to have reciprocal taxes in place.

Renewable Energy:

- Trump is looking at more production of Energy from Oil & Gas, and aims to make Energy utilities cheaper for the people.

- Many Indian companies are top exporters of Solar PV to USA, and could see poor order growth.

- Older policies will remain in place

Geopolitical Stability:

- Geopolitical conflicts have been lower during a Trump presidency.

- This impacts global equities.

Weaker US dollar:

- Donald Trump believes that devaluing the dollar will restore America’s manufacturing sector to its former glory.

- A weaker dollar support’s Indian equities+debt market. FII would be more comfortable holding Indian companies if INR depreciation is low. In the last

- Imports may become cheaper for Indian companies for raw materials, boosting profit margins.

- Indian debt markets high interest rates become attractive given less deprecation of the rupee. Else there’s no use getting 7% yield in India when the INR weakens by 10% every two years.

I plan to continue adding to this thread based on what unfolds. Will appreciate insights from the VP community!

Websol energy system ltd (12-10-2024)

Hi Apoorve, Thanks for sharing this here. I would like to share my thought on this as below;

Kudos to this thesis posted on twitter handle. My compliments to them ![]() . However, the data should be taken with caution before processing into our brain. I could find the joy and unnecessary enthusiasm in the words which is common for anyone who come across a undervalued company for the first time. It sounded good till first half of the thread where the Annual PAT of 170 Crs. was estimated with solar cell production data

. However, the data should be taken with caution before processing into our brain. I could find the joy and unnecessary enthusiasm in the words which is common for anyone who come across a undervalued company for the first time. It sounded good till first half of the thread where the Annual PAT of 170 Crs. was estimated with solar cell production data ![]() which is almost close with many of our conservative estimation ((600 MW*90%/12)*9 months))1.1 Crs. NPM 25% + Q1 PAT 23) = 134 Crs, but the second half started sounding more of a fin-fluencer/influencer tone to me. Hence i ignored the second half of the thesis. The reasons are as follows;

which is almost close with many of our conservative estimation ((600 MW*90%/12)*9 months))1.1 Crs. NPM 25% + Q1 PAT 23) = 134 Crs, but the second half started sounding more of a fin-fluencer/influencer tone to me. Hence i ignored the second half of the thesis. The reasons are as follows;

- Annual PAT of 170 Crs. is with an assumption of 30% NPM which may not be sustainable as input wafer cost is decided by China weekly (Mr. SL Agarwal statement in recent AGM) and not in control of Websol. So, taking 30% NPM straight for the whole year is misleading. As it is a commodity, price fluctuation is part of the business.

- The Twitter handle cited import data of Centrotherm machinery components. Firstly, Those are not looking like main equipments, those are sub assemblies/components/parts which are required for regular preventive maintenance and replacement under warranty for failed components. (As module line production is still under ramp up, the possibility of component failures and replacement is normal.)

- Secondly, management clearly informed us that the expansion is still under planning and they will inform us once it is materialized. They don’t have enough area to expand at the Falta SEZ. Hence, Company already announced that the second phase of expansion shall be implemented at a new location in Odisha under a subsidiary company namely Websol Kalinga green energy./suitable name etc. The proposed company is not registered in MCA website till now.

- Developing a 1.8 GW cell line in Phase-2 in a virgin land outside their existing state without SEZ tax benefits is a humongous task for Websol as the fund requirement would be more than 1000 crs. (DRHP of Vikram, Premier, Waree has machinery quotations from Chinese manufacturers but Websol traditionally uses Centrotherm germany equipment’s which is costlier than Chinese.) I am personally expecting some US/Europe based company collaboration for 2nd Phase expansion.

- In one of the convertible warrants meeting, Mr. SL Agarwal was reading the snippet given to him like “we are expanding the cell line by another 50% in Falta SEZ” i.e., 300 MW in addition to 600 MW. I even recorded the video but there was no follow up official intimation to BSE/NSE. or in the Q1 results. So I ignored it as a slip of tongue.

The second 33 kV line is true as twitter handle provided with the WB Govt. tender proof.

The second 33 kV line is true as twitter handle provided with the WB Govt. tender proof.  However, it is a replacement for old line or for expansion purpose is not clear.

However, it is a replacement for old line or for expansion purpose is not clear.

- The most haunting question in investors mind is whether Websol will self consume their in house cells for module line or use the outsourced cells?. Websol registered Solar cells of 242 MW till Oct in DCR portal. So, there is a possibility of selling in house Cells to DCR market and using the outsourced cells for module line. Twitter handle’s thesis with NPM of 30% for both module line and cell line will fail in big way if they self consume the inhouse cells. Projected revenue of 2280 Crs will become almost half to 1200 Crs. Hence, need further clarity from management.

- If they sell Cells and modules separately in the open market then module may not qualify under DCR category as min. of 55% of domestic content is required to qualify as DCR. Further, the best NPM of module only players are around 10-13% only. So in anyway, Rev of 2280 Crs. and PAT of 685 Crs. with a assumption of 30% NPM for 1.2 GW cell and module is a distant dream with phase-1 alone. It is misleading. Needs clarity from management.

- However, Twitter handles help in taking the company to many retail investors. With visibility, the buy/sell pressure comes. I hope that was the main motive of that twitter thread. My best wishes and compliments.

- Thesis and Antithesis should exist together to avoid biased information and to take neutral informed decision.

- All the above points are all my personal opinion based on the publicly available information limited to my knowledge. I am not an expert and I may be completely wrong. Request others opinion and feedbacks to evolve together.

This Time It’s Different ?! (12-10-2024)

Nifty to S&P500 ratio.

This used to stay below or around the 4 range between 2014-2022. Given it’s sustaining > 4 presently, either I am bearish on Indian equities (short term ofc), or bullish on U.S.

Base currency for the world is USD. Foreign investors have lost 10% in Indian investments due to depreciation. Whether they hedge through currency futures is a different story.

E2E Networks Ltd – Listed small Cloud computing player (12-10-2024)

Competitive intensity in the GPU cloud market in India as of today (Note – it consist of Indian companies only and not the hyperscalers of the west).

While going through the recent newspaper articles and company fillings i have found out that following companies are providing or will start providing GPU cloud services :

- Shakti Yotta Cloud – Biggest in the terms of capacity (Owns Data Centers as well)

- E2e Network Limited

- Krutrim (by Ola group) – New Entrant

- Anant Raj Cloud – New Entrant

Further while reading about the Indian AI mission on one of The Economic Times article found the following para interesting –

“Top chip companies, cloud makers and cybersecurity firms have shown interest in the government’s Rs 10,000 crore GPUs procurement tender, which is central to India’s AI Mission. Nvidia, Intel, Advanced Micro Devices, Qualcomm, Microsoft Azure, Amazon Web Services, Google Cloud and Palo Alto Networks were among the scores of companies that attended a pre-bid meeting on August 29. Also present at the meeting were representatives from the likes of Yotta Data Services, L&T, E2E Networks, Tata Communications, CtrlS, ST Telemedia Global Data Centres, NTT Data, Dell and Vigyanlabs.”

Read more at:

Morepen Labs – a believable turnaround story (12-10-2024)

Even if this gets hived off, generally shares of new company will be given to existing shareholders. Share swap will be function of valuation of both entities

While not clear in this, reason for such hive off is that to have more focus and raising capital (there may be set of investors who may be keen for medical equipments business but not in pharma or other way round)

ADC India Communications Limited (12-10-2024)

Disclosure of your holding & detailed risk analysis is missing.

Arman Financial Services Ltd (12-10-2024)

Look at my last post. Arman (no matter how got it is runned) will and is getting impacted by the MFI cycle. I have tracked the company since last last 4 cycle (8 years+), it has become very predictable now. Only thing different about this cycle is that, despite knowing that the market is over-heated, the management didn’t slowed down the growth to an extent. But it still remains a very very well governed and managed company. Don’t look at the P/E or P/B now, it will compress further, optipically it looks better.

Disclaimer: I exited my 6 years old holding about two quarters back, but will look for opportunity to re-enter once the dust settles.

Geospatial sector – Sunrise Opportunity (12-10-2024)

Thank you for sharing valuable information.

Can you please share the websites from where you found out that ceinsys was the lowest bidder and the website from where you found out the technical tender details doc. This would help a lot of beginner investors.