332b0898-e8eb-41ee-9045-d2116c4d5cb0.pdf (619.5 KB)

.

First approval for the merger is here…

Posts in category Value Pickr

IDFC First Bank Limited (17-10-2023)

Newgen Software (17-10-2023)

Newgen reported excellent results.

Revenues at Rs 293 cr in Q2 FY’24, up 30% Q2 YoY; Profit after Tax at Rs 48 cr, up 59% Q2 YoY

New logo addition:14

Revenue and margin expansion, was well received by market today.

To take decision of booking profits on P/E is tricky. Growth may continue for coming time also. Best time to sell growth stock is when growth slowdown.

Disclosure: Invested

Dividend Yield Portfolio – for Wife (17-10-2023)

I personally use RSI for this … Weekly RSI

See the bright Sun: Aditya Vision (17-10-2023)

HDFC mutual fund bought more 95k shares @2602/-.

Vinati Organics (17-10-2023)

Status of Veeral Additives Private Limited’s amalgamation case as per NCLT portal

NCC: Extremely undervalued (17-10-2023)

NCC has everything going good for it – Increase in

Order inflow & backlog

Revenue

Profits

Govt spending on various infra projects

It is still trading at reasonable valuation

While so many stocks have moved up very high, NCC hasn’t moved up to that extent – inspite of all the good news on business front

Can anyone share inputs on the possible reasons? Is it possible that lot of accumulation is going on?

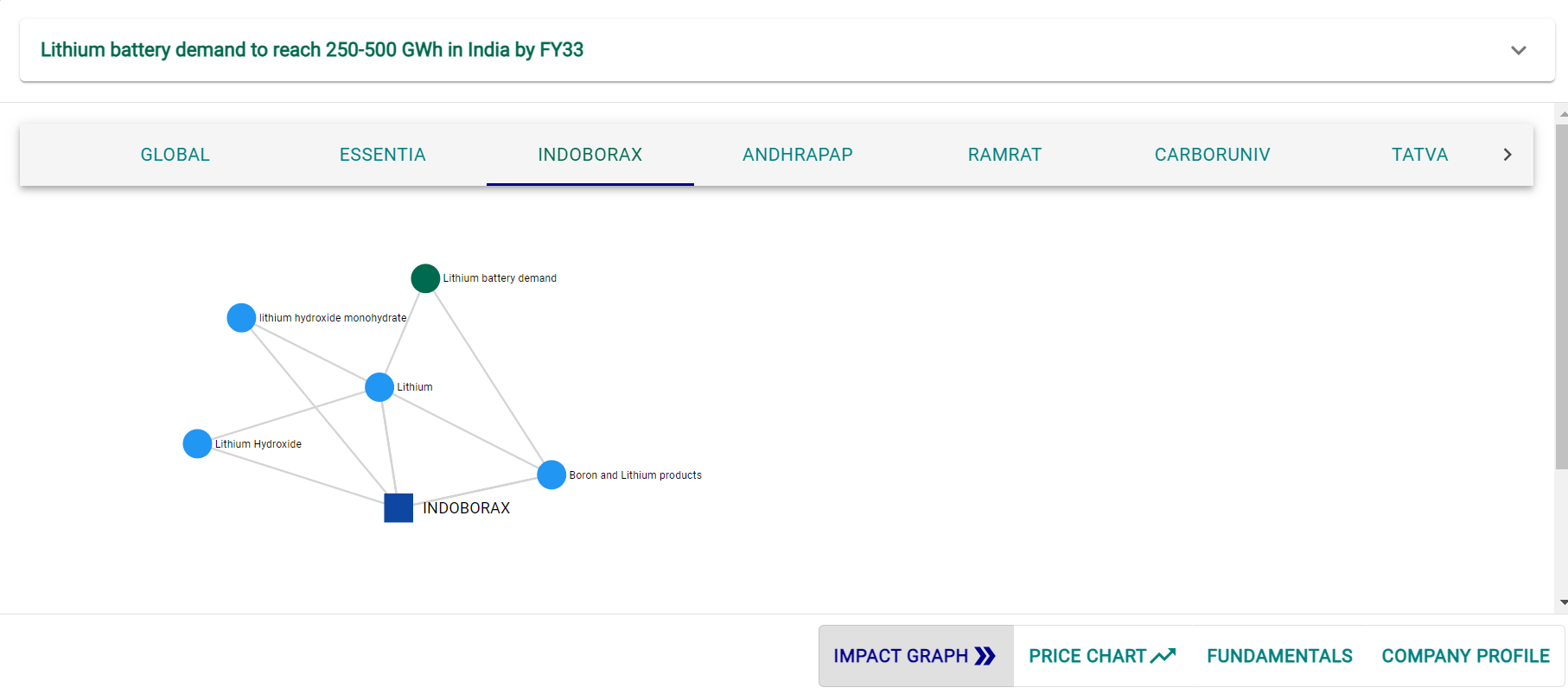

Lithium Battery Demand Surge in India Expected to Bolster Indo Borax and Chemicals Stock (17-10-2023)

India is poised for a monumental surge in lithium battery demand, and Indo Borax & Chemicals Limited (NSE:INDOBORAX), a manufacturer and seller of boron and lithium products, stands to benefit significantly. With projections indicating that the demand for lithium batteries could reach between 250 to 500 GWh by fiscal year 2033, the company’s prospects are looking brighter than ever.

The recent report, titled ‘EV Batteries: Battle to control EV supply chain’ by Axis Capital, has highlighted that achieving a 250 GWh battery demand would necessitate incentives of INR 1.8 trillion over the period of fiscal years 2024 to 2028, along with an initial capital expenditure (capex) of USD 30-33 billion. This forecast is in line with India’s ambitious goals to electrify its transportation sector and reduce its carbon footprint.

So, how exactly is this bullish forecast going to positively impact Indo Borax & Chemicals Ltd’s stock price?

Increased Demand for Lithium Products : Indo Borax & Chemicals Ltd manufactures and sells lithium hydroxide monohydrate products. With the rapidly growing demand for lithium batteries in India’s electric vehicle (EV) market, the company’s lithium products are likely to be in high demand. This uptick in demand can potentially lead to increased revenues and higher profits.

Positioned for Growth : Indo Borax is already established in the Indian market and has been providing quality lithium products for years. This positions them well to capture a substantial share of the growing market, given their experience and track record.

Market Confidence : A booming industry and an established player like Indo Borax can instill confidence in investors. As they see the company benefiting from India’s electric vehicle revolution, it can attract more investment and drive up the stock price.

Favorable Regulatory Environment : As the Indian government provides incentives and support to the EV industry, it indirectly benefits companies like Indo Borax. The conducive regulatory environment can create a positive atmosphere for the company to thrive.

Strong Financial Performance:

In addition to these promising forecasts, Indo Borax boasts impressive financial credentials that make it a compelling investment opportunity.

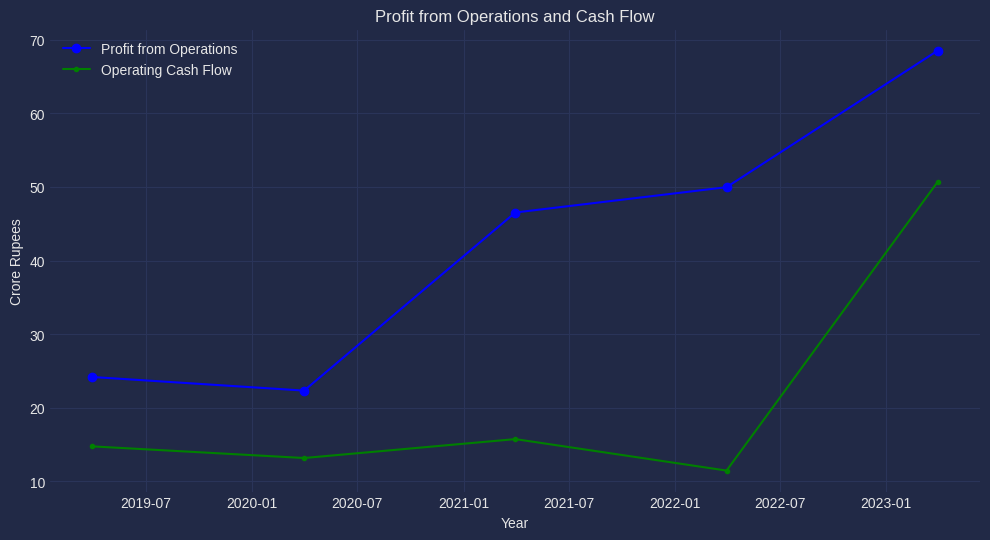

The above figure shows operating profit growth for the last 5 years.

Robust Profit Growth : Over the past five years, Indo Borax has demonstrated remarkable profit growth, with a staggering 243% increase. This equates to a compounded annual growth rate (CAGR) of 28%. Such consistent profit growth signifies a company that is efficiently utilizing its resources and generating value for its shareholders.

Strong Cash Flow Position : The company maintains a healthy cash flow position with a consistent 183% growth over the last five years and a CAGR of 23%. This strong cash flow not only ensures operational stability but also provides flexibility for investments in research, development, and expansion.

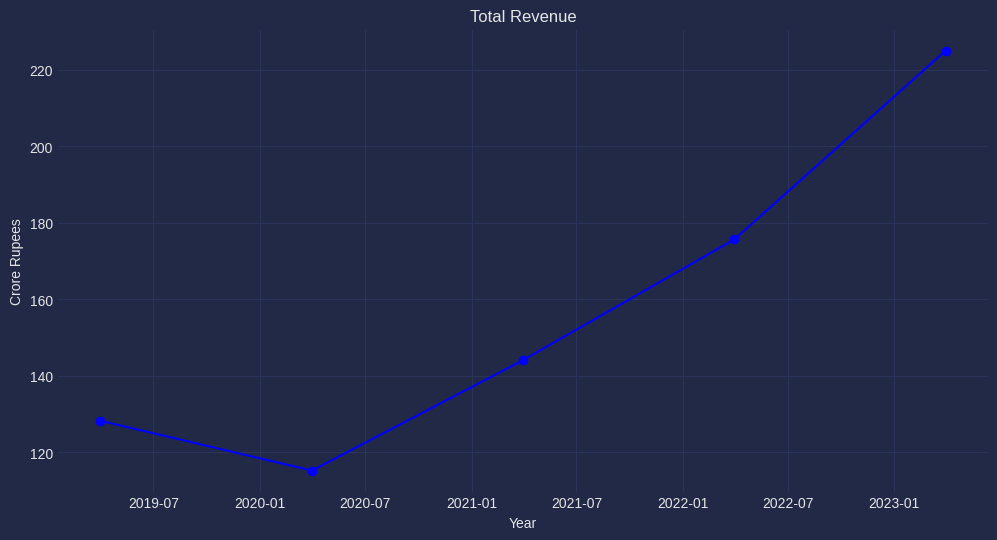

The above figure shows the revenue for the last 5 years.

Impressive Revenue Growth : Indo Borax’s revenue has surged by 75% over the past five years, demonstrating a CAGR of 11.89%. This growth highlights the company’s ability to capture market opportunities and meet the rising demand for its products effectively.

Attractive Valuation Metrics : The company’s PEG (Price/Earnings to Growth) ratio stands at 0.5, well below the typical threshold of 1. A PEG ratio below 1 suggests that the stock may be undervalued relative to its growth prospects.

Favorable Valuation Ratios : Indo Borax boasts a Price/Book (P/B) ratio of 2, which is below the industry median. Additionally, the Price/Earnings (P/E) ratio is a modest 10.7, also below the industry median. These metrics indicate that the stock may be attractively priced compared to its peers.

Debt-Free Status : The company’s debt-free status is a significant advantage in a potentially high-growth industry. It means that Indo Borax does not have substantial interest payments or debt-related risks that could hinder its growth or financial stability.

Conclusions

In conclusion, the surging lithium battery demand in India is expected to have a positive impact on Indo Borax & Chemicals Ltd. In light of Indo Borax & Chemicals Ltd’s robust financial performance and the burgeoning demand for lithium batteries in India’s electric vehicle market, the company is well-positioned to thrive. These factors, combined with a favorable regulatory environment and established market presence, bode well for the company’s future. The company is well-positioned to capitalize on this trend, potentially leading to increased revenue and growth opportunities.

Reference: Lithium battery demand to reach 250-500 GWh in India by FY33

Disclaimer: The article is not a recommendation or advice as to whether any investment is suitable for a particular investor.

Mazagon Dock: aptly called “Ship Builder to the Nation” (17-10-2023)

Mazagon Dock Shipbuilders to construct Defence Ministry’s Coast Guard Training Ship for Rs 2,310 crore.

Tanla Platforms ~ Leading player in the fast-growing CPaaS market (17-10-2023)

Sorry if this has been answered before but why DIIs have always stayed away from this company?

Nithin’s Portfolio (17-10-2023)

Newgen Concall Q2, 2024 :

- Management has said that H2 will be better than H1.

- The company is hiring more freshers at a size of 700 or more

- Attrition rate is far lower

- Doing well in both BFSI & GSI segment

- Management has ambition to grow EBITDA more than 20% and PAT more than by 18% from the given trend

- Got new wins from domestic market, one being India’s largest bank

Need to be mindful of employee cost and revenue stream from subscription, long term contracts.

So far no changes to contracts/subscription.

Will share updates when I get transcript – so far all looks good, will continue to ride it…