i think there is no option but to apply and go through it… it may take months…

dont know what the purpose to delay for no reason – whether it is to discourage people to become RA/IA?

Posts in category Value Pickr

How to register with SEBI as a Research Analyst? (11-10-2024)

Sai Silks (Kalamandir) – only listed player in the organized saree market (11-10-2024)

Thanks a lot for sharing it, in my views management is completely lagging what they have promised, I don’t think they gonna be meeting their future revenue or store count guidance.

Ceinsys Tech-Engineering, Geospatial & IT solutions Company (11-10-2024)

(post deleted by author)

Sai Silks (Kalamandir) – only listed player in the organized saree market (11-10-2024)

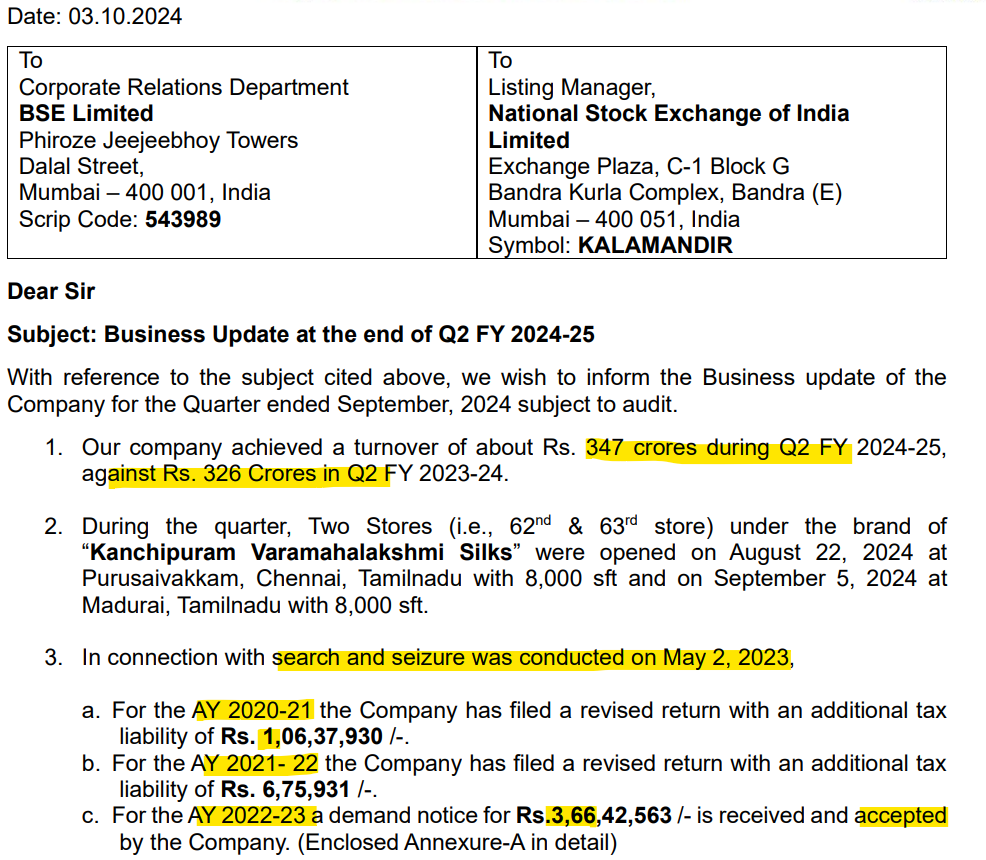

03-Oct-2024 exchange filing:

In nutshell:

- YoY revenue growth in Q2 seems mild (6.5%). Let’s wait for the results to see how operating profit grew.

- IT search and seizure outcome is reported under a regular subject: Business Update. Seems business has accepted the IT demands. Hence, revised returns for the 3 Yrs [AY20-21,AY21-22 and AY22-23].

Disc: No position.

Sai Silks (Kalamandir) – only listed player in the organized saree market (10-10-2024)

I am quite convinced with the management reply on Q1 results due to very less or no wedding dates in the Q1.

Regarding margins I think they have different format stores, which has different margin profile. If we can get Vara maha Lakshmi stores margin profile then it would be helpful to access.

Tracing this company from last 2 quarters, I feel we will see good grown in numbers as they keep on adding Vara maha Lakshmi stores in TN & KA as avg invoice value of these stores is highest among all formats and PE expansion also should be there as they grow in numbers and expand margins going forward.

Troll’s Portfolio (10-10-2024)

No, I am not swing trader. As mentioned i am invested for minimum 3-4 years in most of portfolio stocks. Also i mostly rely on fundamentals, concalls etc. I exit only the tracking positions which i take if am not able to make my mind. Zodiac was tracking position. Phantom will see a lot of disruption to business model thus the exit and IPL was mentioned to be cyclical bet in any case. Other than that ~90% of portfolio remains as it is in last two posts. What makes u feel like i churn a lot?

Troll’s Portfolio (10-10-2024)

Just one thing I have noticed. You seem to change your composition quite frequently. Are you more of a swing trader? If you are seeking investments, then it is important to stay put for a while and only exit if your thesis breaks up.

Lincoln Pharma … the next mid-cap pharma in the making …? (10-10-2024)

Lincoln Pharma has a history of inflating its profits, In FY 2012, the company reported a lower provision for bad debt, categorizing it under trade receivables.

With other income sources including 22 crores from share valuations related to investments or trading.

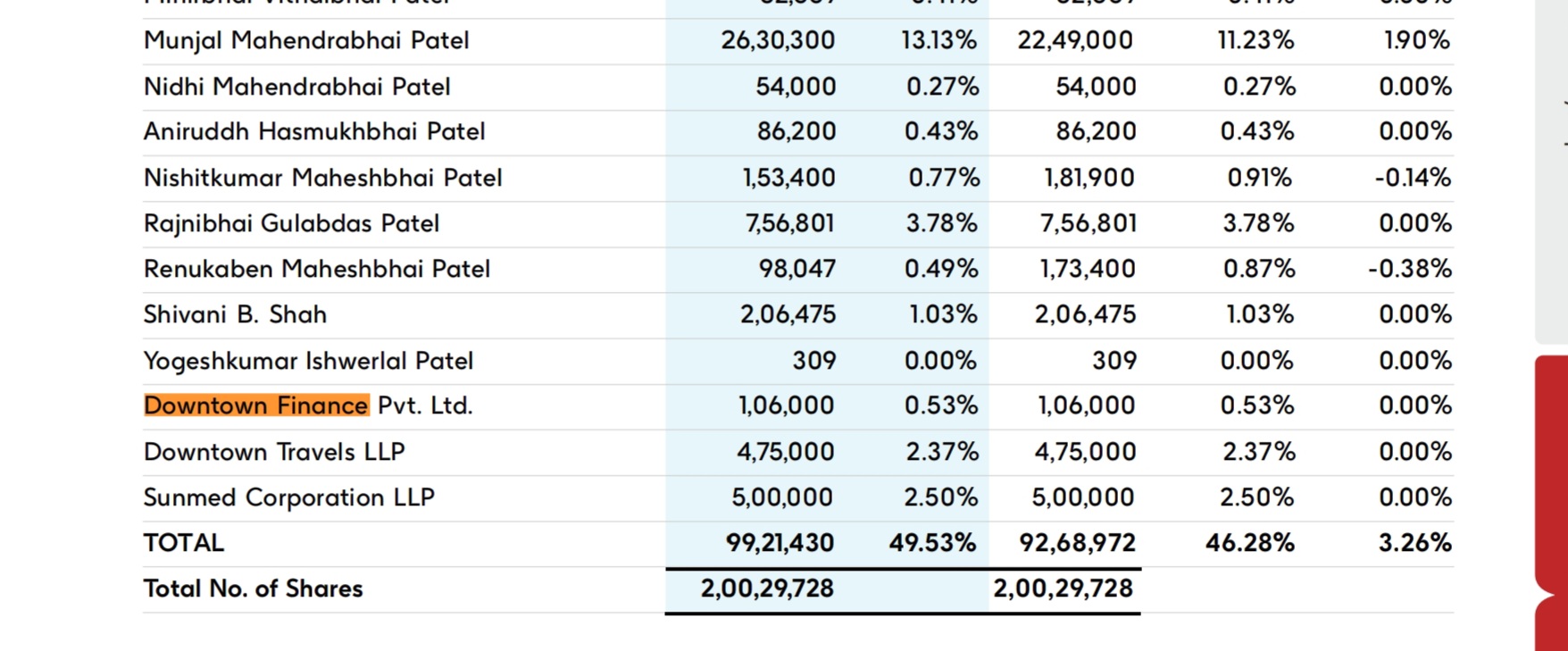

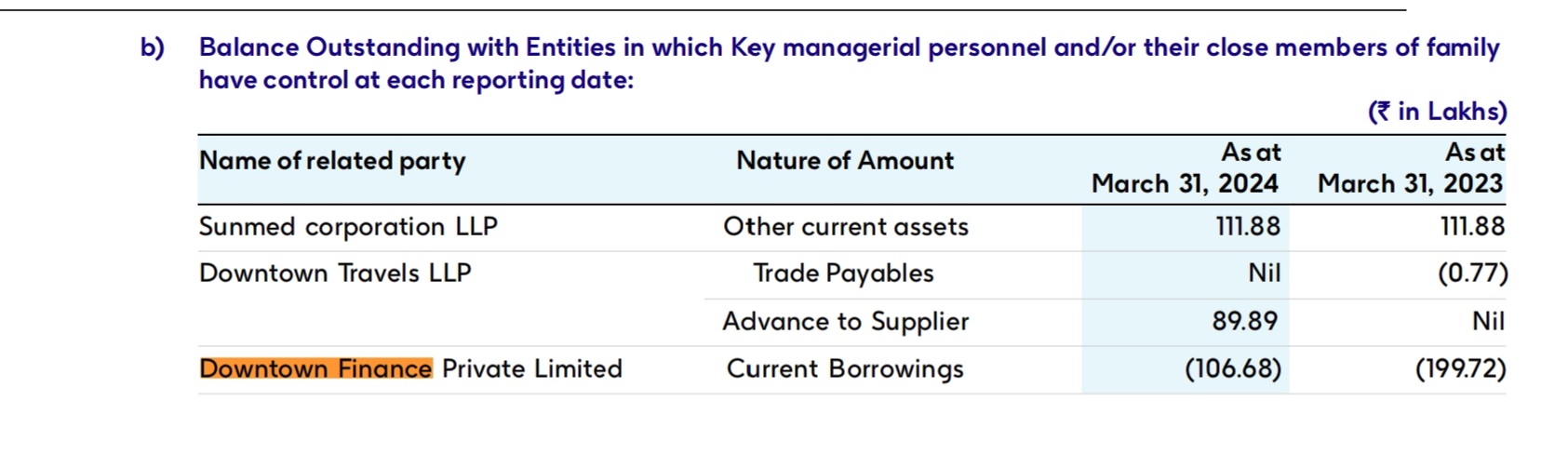

The company also lends money to Downtown Finance, managed by key personnel who invest in Lincoln Pharma shares during significant stock price declines. When asked about this, Munjal Patel stated, “We help them, and they help us,” emphasizing their reciprocal relationship.

Even after excluding fair valuations from stock trading income, the price-to-earnings ratio stands at 20, and low sales growth since 2016 likely contributes to this low P/E ratio.

[My view] Additionally, being a debt-free company, Lincoln Pharma has the flexibility to take risks and generate capital from various sources, including stock trading, which it can ultimately reinvest in its business. If revenue increases in the near future, the price-to-earnings ratio could rerate to 35 or higher, potentially pushing market capitalization beyond 5,000 crores and positioning it as a potential multibagger.

Moreover, cephalosporin developments are in the final stages and are expected to be monetized soon. According to management, this could boost revenue by 250 crores, serving as a significant growth trigger for the company.

Disc: Invested

NPST – Technology Provider for UPI Tech (10-10-2024)

Good analysis Raj. All the numbers I have quoted are QoQ and not YoY. The 2nd table I have is summation from the 1st table, adding 3 months.

The larger point that I was trying to make (and I see you’re coming to the same conclusion) is that the market seems to assume that the drop in Cosmos Payee PSP numbers will have an equivalent impact on the NPST revenues and eventually the stock price, which I don’t think is going to be the case. It may be directionally right but definitely NOT in terms of quantum.

Lincoln Pharma … the next mid-cap pharma in the making …? (10-10-2024)

If we look at last year, the core profit growth YoY has been at 11% while the net profit growth has been at 22% due to the other income.

However the stock p/e excluding the other income is still around 14 (souce screener). Stock still looks cheap to me. But for a rerating they will need to show growth in core business which they have been promising of 15%+