In ethos company sales growth

Selan Oil Exploration (25-09-2023)

We will have more clarity from the management at the AGM later this week. The merger valuation is a complicated exercise in terms of valuation, tax impact, NCLT, BSE and NSE approval etc. so it will take about a year. The terms will come in due course but the management. I don’t expect them to be unreasonable to Minority shareholders as I always say that the majority shareholder (i.e. Oaktree) wouldn’t want to ruin its reputation over a $10 mn transaction.

The interesting thing is that they don’t want to wait and plan to use the cash (via an inter-co loan) to develop offshore assets in Antelopus which would have been concerning if the merger wasn’t on the cards.

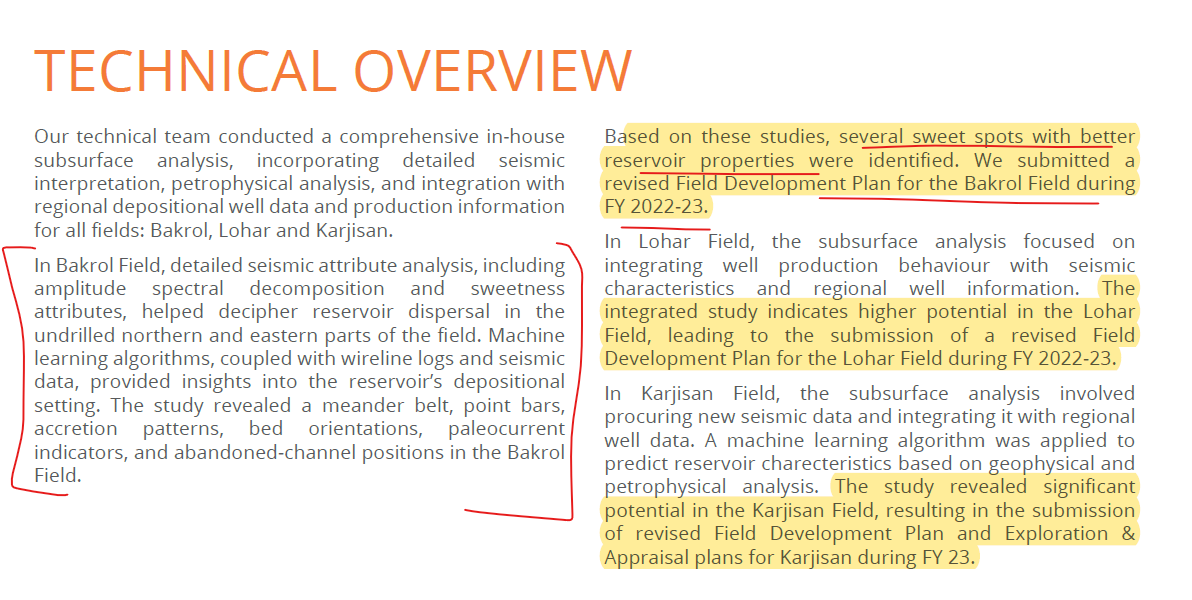

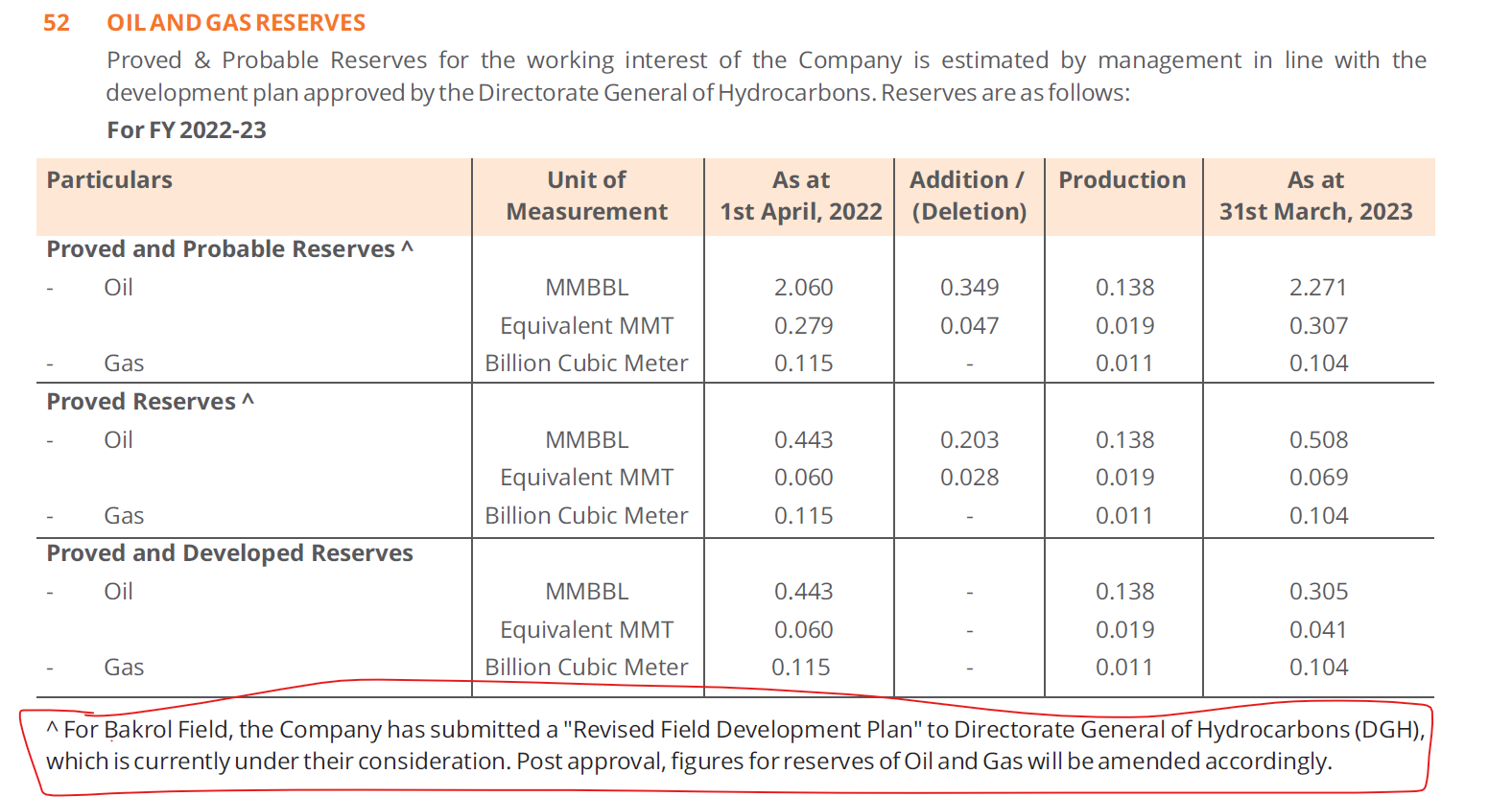

As an aside, I don’t think anyone noticed a particular disclosure in their current annual report under Technical Overview section followed by Note 52 where they disclose the oil and gas reserves. My reading is that they have found a higher reserve than expected. Hopefully, management clarifies during the AGM. Lots of optionality still in the asset. ![]()

Disclosure: invested and biased.

Ranvir’s Portfolio (25-09-2023)

Glenmark Pharma latest updates-

Selling 75 pc stake in GLS (Glenmark Life Sciences) that was involved in making APIs and had a small CDMO business – to Nirma Group

To get sale proceeds (post Tax) of about 5000 cr. Has a debt of 4600 cr on Books

GPL to be debt free by yr end

GLS used to pay hefty dividends to its parent so as to reduce its Debt burden. That obligation is now gone

GLS’s CDMO ambitions were at risk as its parent (GPL) was involved in NCE research. Innovators were uncomfortable handing over CDMO projects to GLS because of that

GLS used to trade at significant discount to peers because of these reasons

I think, its a win-win for both GPL and GLS

Disc : bought a tracking position in both

Glenmark – Will Innovation Pay? (25-09-2023)

Glenmark Pharma latest updates-

Selling 75 pc stake in GLS (Glenmark Life Sciences) that was involved in making APIs and had a small CDMO business – to Nirma Group

To get sale proceeds (post Tax) of about 5000 cr. Has a debt of 4600 cr on Books

GPL to be debt free by yr end

GLS used to pay hefty dividends to its parent so as to reduce its Debt burden. That obligation is now gone

GLS’s CDMO ambitions were at risk as its parent (GPL) was involved in NCE research. Innovators were uncomfortable handing over CDMO projects to GLS because of that

GLS used to trade at significant discount to peers because of these reasons

I think, its a win-win for both GPL and GLS

Disc : bought a tracking position in both

Glenmark – Will Innovation Pay? (25-09-2023)

Glenmark Pharma Q1 results –

Region wise sales –

India – 1064 cr, up 3 pc (under performed the IPM)

North America – 808 cr, up 22 pc

Europe – 573 cr, up 73 pc

RoW ( basically EMs ) – 551 cr, up 30 pc

APIs – 376 cr, up 16 pc

Others – 27 cr

Total sales – 3401 cr, up 22 pc

Percentage of Branded sales out of the total @ 47 pc

( basically India + RoW formulations )

EBITDA @ 631 vs 431 cr

Margins @ 18.6 vs 15.5 pc YoY

Glenmark’s 9 brands are in top 300 brands in IPM. Glenmark is no – 2 in Respiratory and Derma segments in India

Glenmark Consumer care grew 20 pc. Has popular brands like – Candid Dusting powder and Scalp Anti Dandruff shampoo in its portfolio

Mkt Share of Glenmark’s Speciality Drug – Ryaltris (nasal spray for allergies) in various countries –

Aus-18 pc

SA-15 pc

Poland-8 pc

Italy-10 pc

Glenmark’s subsidiary – Ichnos Sciences has various NCE under discovery and development phase – most of them are Oncology molecules. GPL aims to get into some out-licensing deals yr

Have reduced R&D spends to 8.5 pc of sales. Will bring it down to 7.5 odd pc by next yr

This will boost profitability going forward. GPL’s heavy spends (beyond Industry norm of 5-6 pc of sales) are because of its NCE programs

Company to remain focussed on 03 Pharma therapies – Derma, Respiratory, Oncology. Going to launch a number of new products in these areas

Continue to file 10-15 products in US/ yr. But the complexity of the products has gone up significantly. Not filing plain vanilla products anymore

Disc: hold tracking positions in both GPL and GLS. Biased. Not SEBI registered

Ranvir’s Portfolio (25-09-2023)

Glenmark Pharma Q1 results –

Region wise sales –

India – 1064 cr, up 3 pc (under performed the IPM)

North America – 808 cr, up 22 pc

Europe – 573 cr, up 73 pc

RoW ( basically EMs ) – 551 cr, up 30 pc

APIs – 376 cr, up 16 pc

Others – 27 cr

Total sales – 3401 cr, up 22 pc

Percentage of Branded sales out of the total @ 47 pc

( basically India + RoW formulations )

EBITDA @ 631 vs 431 cr

Margins @ 18.6 vs 15.5 pc YoY

Glenmark’s 9 brands are in top 300 brands in IPM. Glenmark is no – 2 in Respiratory and Derma segments in India

Glenmark Consumer care grew 20 pc. Has popular brands like – Candid Dusting powder and Scalp Anti Dandruff shampoo in its portfolio

Mkt Share of Glenmark’s Speciality Drug – Ryaltris (nasal spray for allergies) in various countries –

Aus-18 pc

SA-15 pc

Poland-8 pc

Italy-10 pc

Glenmark’s subsidiary – Ichnos Sciences has various NCE under discovery and development phase – most of them are Oncology molecules. GPL aims to get into some out-licensing deals yr

Have reduced R&D spends to 8.5 pc of sales. Will bring it down to 7.5 odd pc by next yr

This will boost profitability going forward. GPL’s heavy spends (beyond Industry norm of 5-6 pc of sales) are because of its NCE programs

Company to remain focussed on 03 Pharma therapies – Derma, Respiratory, Oncology. Going to launch a number of new products in these areas

Continue to file 10-15 products in US/ yr. But the complexity of the products has gone up significantly. Not filing plain vanilla products anymore

Disc: hold tracking positions in both GPL and GLS. Biased. Not SEBI registered

Logistics sector (25-09-2023)

Anyone tracking Transport corporation of India, needed to understand why this is cheap compared to its peers?

Investing Basics – Feel free to ask the most basic questions (25-09-2023)

One basic query regarding management…

Many investors advocate benefits of professional management like in case of TCS, Infosys where professionals are hired as CEO and CFO and company operations are handled by professional people. Experience and qualifications are cited as key positives for them.

While promoter-managed comapnies are looked down as they may be not much qualified , like Howard returned or IIM alumni etc. But if we see closely, many promoter managed companies have very high personal wealth of promoters in the form of company equity…so when there is skin in the game, there is a better chance of more prudent decision making and strict control of expenses etc. They are less likely to go on inorganic acquisitions than professional managers. So what is more better? Who will create better value for shareholders?

The SME portfolio (25-09-2023)

That is more than required, appreciate you giving such a reply.

VP in a sense is more matured investing, even the members who churn more relative to others, and I don’t remember anyone investing exclusively in SME. I guess, even the members who can understand more about businesses, who can allocate more, for whom lot size does not matter, even they don’t participate as much as you. And I have looked at just a few SME names on occasion, but never participated. One reason being the restriction of capital for such endeavors, other being to wait for the stock migrating to main board, and that I can wait, even if a business is compelling.

There are some young members who are active in the forum, but they participate in bigger names, and yours, from the topic title to the latest post, is exclusive to SME, unique contribution.

Although I do have some basic idea of how things work at the lower rungs of the ladder SMEs, your experience is a good learning of a high risk, high reward segment.