Why is the stock correcting every day ? Any new concern or risk? Also what are the risks associated with the order book growth slowing down in future? Like is the momentum for railways related order book near its peak or still further away from it?

Posts in category Value Pickr

IDFC First Bank Limited (23-09-2023)

IDFC uses lots of data analytics & monitoring customer’s banking behaviour. The management has long experience of Retail lending and if one listens to CEO, he is comfortable growing the bank at 25% CAGR not more than that even though they have potential to exceed that. He is careful while lending to various customers that dont fit their lending criteria. They have serious focus on getting the money back plus the book is very granular.

I also keep getting the top up car loan offer. If a loan offer is given to one customer, it doesnt mean that same offer will be extended to all. Bank does lot of customised loans based on analytics and credit behaviour.

IMHO Its not right to say that bank is lending recklessly. Even during covid, retail portfolio and restructuring was not thar high.

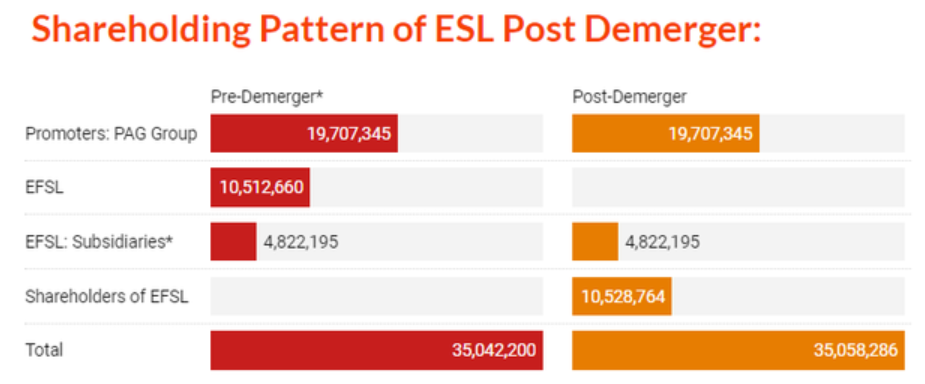

Edelweiss Financial Services (23-09-2023)

Am I correct in assuming that the price of Nuvama should be around Rs 2500 if we are expecting 9000 Cr mkt cap?

Most Important Ratios – my take (23-09-2023)

There are hundreds of metrices available for a value investor to look into while valuing the company and sometimes it can be extremely confusing.

Normally, I tend to look for these measures while valuing a company and try to separate the wheat from the chaff:

- Debt to equity – This should be as low as possible. Less than 0.3 is what I normally put the filter on.

- Unpledged promoter holding – This should be as high as possible. Normally I select more than 45-50%. Promoter running the business must have skin in the game.

- Pledged percentage – it must be zero. I don’t like companies where promoter has pledged their shares to raise capital.

- FCF to Invested Capital – Over a period of 3, 5 and 10 years, CAGR of ratio of Free cash flow to firm and invested capital should be very high. This ratio shows how much free cash flow the firm is generating for the capital invested in the firm. It’s needless to say that I don’t like the companies who aren’t generating positive OCF and FCF over 5-10 year periods.

- Reinvestment Rate – High reinvestment rate from both debt + equity and purely from equity capital perspective. It basically shows how much management is reinvesting in the company back from the earnings it got. Higher this rate, higher the conviction of the management to grow the business.

- ROIIC – High return on incremental capital invested over last 10 years. Again, this should be calculated from both debt + equity and purely from equity point of view. It’s a much better measure than ROCE in my opinion. It shows the return generated by the company based on the incremental capital over a period of time.

- Value compounding rate of the company – This should be as high as possible. This is calculated as the product of reinvestment rate and ROIIC. If a company can retain 25% of its capital and reinvest that capital at a 10% return, we’d expect the value of the company to grow at a rate of around 2.5% per year (10% x 25%). Stockholders will likely see higher per-share returns than that because of dividends and buybacks, but the total value of the enterprise will likely compound at roughly that rate.

- Comparison of Value compounding rate with stock price CAGR over the years – we can quickly compare value compounding rate of the company vs stock price CAGR over 10 years. This is basically a comparison of how much value addition company is creating with the infusion of capital vs the stock price CAGR. If stock price CAGR is less than value compounding rate, its screaming undervalued. If its extremely high then its overvalued in my opinion and with mean reversion, we can expect the price to drop soon to match with the value compounding rate.

Once these basic criteria are met, I then look into other important ratios such as SSGR, fragility scores, movement of FCF, OCF, pricing power through increasing net profit margin, margin of safety, management quality etc. But above are the initial checks that I do and if any company fails to meet those criteria, I will skip it more often than not.

Edelweiss Financial Services (23-09-2023)

This is only edelweiss financial services quantity not by PAG inclusive.

SKM Egg Products – thinking out of the shell (23-09-2023)

So basically they did well in FY23 due to Russia-Ukrain war which created shortage in egg supply. I dont think this growth is sustainable. Please share your thoughts on this.

Gujarat Fluorochemicals: A hidden fluorine story (23-09-2023)

This is a May report

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (23-09-2023)

By the end of 2023, China will control half the world’s installed capacity of electrolysers

While we are racing ahead with Production of renewables at a time when Hydrogen Electrolyser capacities are yet to be built up to scale, the world is looking for BESS ( Battery Energy storage system) to store Renewable energy for using later and Li ion batteries with its high energy density quality are preferred choice.

However, As usual China seems to have understood it correctly. Li Ion battery rare earth elements which are scarce and found in a handful of nations is going to be in great demand both for EV & BESS.

They seem to be ready with Green hydrogen Electrolyser capacity . They would like to Rule the world with half the world’s requirement.

Edelweiss Financial Services (23-09-2023)

Any update on listing price? 9,000cr mcap/10.5m shares of rs 10. Is this calculation appropriate?