Hi Sreener Team,

Is there any plans to add fundamental data, ratios and charts for index as well. This will be a great addition to such a useful tool you all have developed.

Regards.

Hi Sreener Team,

Is there any plans to add fundamental data, ratios and charts for index as well. This will be a great addition to such a useful tool you all have developed.

Regards.

Follow Tar – investkaroindia.co.in. His weekly newsletter has all the information.

am not related to Tar anyway, just found his work useful hence sharing.

Thank you for the idea and information. I used to shop at Magson in the past; their products have good quality, and they generally sell in bulk quantities. Therefore, we can anticipate high margins, although it may not be suitable for the mass market. Hence, revenue growth is expected to be reasonable. Two consecutive fiscal year growth figures may be indicative which is much lower than anticipated.

Deeper analysis of the annual report, it reveals significant related-party transactions. For instance, someone’s brother is employed within the company, and there are also purchases from related parties. This appears to be an issue that requires close monitoring going forward.

Thanks @Utkarsh_Bharadwaj for the efforts around COF. Completely agree with COF coming down further and Bank able to maintain atleast 5.50%-6% range of margins in future. Would like to add couple of points around COF, Bank & NIM:

Stabilising technology spends and positive contribution from High yielding Credit cards + Cross sell from branches will further help to reduce COF as commented by Mgmt even after spends on adding more branches over time.

Industry leading services and innovation in age old products like Offering Auto sweep to FD facility for MSME CA Balance of INR 2 lacs will garner lot of Current account business. Bank has also built good Govt banking, startup business, MSME which have strong CA potential.

IDFCB has strong Risk people at the Top from ICICI, HDFC Bank and are focussing a lot on Rural banking, MSME with loans with Avg yield of 12-15% and bank is able to manage risk in that segment with high use of data and proprietary lending models & most importantly strong experience of lending in these segments. These loans will balance the lower NIM from Home loans, Vehicle loans in Tier 1-2 cities resulting from aggressive growth in Secured assets. Having followed banking closely, I don’t see any other Mid size bank with 25 plus loan products in Retail + MSME and still innovating. The problem with other banks is that they have close to 50% corporate book with lower NIM and focus on new products + customer service is lower. IDFC has less than 20% wholesale book where lending is more to NBFC’s and A rated corporates with exposures in the range of 200-250 crore.

Since the bank is going much granular, CASA customers will continue to adopt IDFCB over PSU banks and many other regional banks due to strong brand and services. Further, CASA customers today are not much concerned about interest rates on SA but more on security, ease of banking, products, customer support, App UI, Customer value. IDFCB is performing well on all these and should be able to grow its customers offering lower SB rates as well. Amongst the large banks, ICICI has been a pioneer in digital banking and today CTO of ICICI is with IDFC alongwith many other senior members. For eg: Being a First Select customer of the bank from last 5 years, I have never received a call from Bank/RM to buy any insurance or unnecesary product whereas there are ruthless eg’s of people being mis-sold ULIP by banks. There are many more references of strong customer focus and ethical banking which one will come across by using their services or reading AR.

Motto of the Bank is Ethical + Digital + Social good. Mgmt. has ensured that these are not words only.

If only IDFCB can keep the GNPA within 1.50%-2% bank level, it can do a 20-25% CAGR for a long time seeing the credit opportunity available in the country.

P.S.: Significantly Invested from lower levels & would be comfortable in averaging up over time with the progress of the bank.

Sapphire food is far better than burgur king.

sir, by that the rates have been changed drastically. is there any web page that can collectively provide information on regular basis.

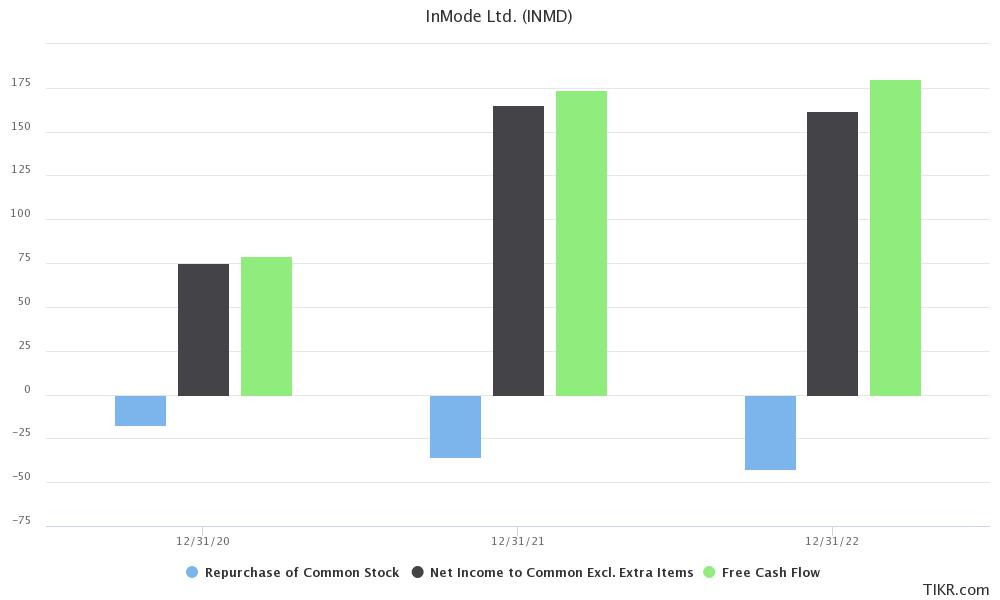

Share price fall: Its very common for share prices to fall a lot, I have seen Inmode falling from $100 to $20 without any deterioration in business quality. So this fall doesn’t seem too much.

Dividends: I dont know why most of NASDAQ cos do not pay out dividends, despite generating high cashflows. That being said, InMode does regular buybacks and has bought back $95mn worth of shares in last 3 years, which is 22% of their freecashflows over these 3 years. This is in-line with most growing cos, I prefer them to reinvest most of their capital in their business.

R&D: They spend $10mn on R&D each year, they have kept the absolute spends constant in last 3-years, while growing sales from $200mn in 2020 to $500mn now. Thats why % spends look lower.

Acquisition: Its hard to make a generic comment on it, let them do something first before making a judgement on it.

I have been regularly buying Disney shares, I do feel its very undervalued. Over time, risk has reduced significantly in Disney as they have invested in building their streaming business and diversified beyond their linear TV business. Currently, market doesn’t like streaming cos, but just 2 years back market thought that streaming cos will rule the world. Over a longer period of time, its content which will make the difference. Whatever the distribution medium is, content will find a way to get monetized as long as customers want to see that. I feel Disney has one of the most precious contents, and they continue investing in that. Park is a decent business, and is currently doing very well.

I am finishing up my work on Stellantis. I will likely buy it soon, its crazy cheap!

Beneficiary list is not available in public domain for UP. As per my assessment , the the current 10000 Pump orders for Shakti Pumps pertains to Kusum Target for FY 2022-23 for UP(pending Solar Pump around 12550 Nos) and not from FY 2023-24.

Enclosed is sanction approval note date 15/09/2023 of UP Government for 30000 Pumps which is target for current financial year. It seems that KUSUM will be implemented in true spirit during the current FY in all states.

UP SHASHANADESH 150923.pdf (743.1 KB)

http://shasanadesh.up.gov.in/GO/ViewGOPDF_list_user.aspx?id1=NjEjMzcjNSMyMDIz

State wise implementation target:

| 1 | Andaman & Nicobar | 100 |

| 2 | Andhra Pradesh | 1000 |

| 3 | Arunachal Pradesh | 200 |

| 4 | Assam | 5000 |

| 5 | Bihar | 5000 |

| 6 | Chhattisgarh | 25000 |

| 7 | Delhi | 1000 |

| 8 | Goa | 200 |

| 9 | Gujarat | 7000 |

| 10 | Haryana | 160000 |

|11 | Himachal Pradesh | 700 |

| 12 | Jammu & Kashmir | 4500 |

| 13 | Jharkhand | 8000 |

| 14 | Karnataka | 10000 |

| 15 | Kerala | 100 |

| 16 | Ladakh | 1600 |

| 17 | Lakshadweep | 100 |

| 18 | Madhya Pradesh | 50000 |

| 19 | Maharashtra | 180000 |

| 20 | Manipur | 150 |

| 21 | Meghalaya | 200 |

| 22 | Mizoram | 1700 |

| 23 | Nagaland | 100 |

| 24 | Odisha | 4500 |

| 25 | Puducherry | 100 |

| 26 | Punjab | 50000 |

| 27 | Rajasthan | 110000 |

| 28 | Sikkim | 100 |

| 29 | Tamil Nadu | 4000 |

| 30 | Telangana | 400 |

| 31 | Tripura | 3000 |

| 32 | Uttarakhand | 1500 |

| 33 | Uttar Pradesh | 30000 |

| 34 | West Bengal | 1000 |

|TOTAL||666250|

Disclosure: Substantially Invested , views fully biased and increasing at every dips.

Such information will be there in quarterly presentations and analyst concalls.

Analyzing Indian Hotels is inherently difficult even in normal times, and the pandemic has further distorted the data last three years. Here an attempt is made to compare the current fundamentals over FY20 with some back of the envelope calculations.

In the data shown above, we can see that on a TTM basis, revenue from operations is currently 1.35 times FY20 figure. Operating profits are 1.9 times with a big improvement in operating margins from 22 % to 31 %. Due to this, PBT is higher by 3.43 times and EPS by 2.77 times the FY20 figure. The company has turned cash positive from a net debt position, thanks to an equity fund raise and improved business cash flows which were double last year over FY20. I have not included operating metrics like no. of rooms, RevPAR etc. as all that is factored in the revenue and profit figures.

Looking at the macro, management says hotel demand in FY23 grew by 11.1 % and supply grew by 4.5 % Vs. FY20. In the current year, domestic airline passenger growth is flat in June 23 vs. June 19 at around 120 – 125 lac passengers per month. Overall, airline passenger traffic for August inclusive of international is still down from pre-pandemic levels. Foreign tourist arrivals are also running below the pre pandemic levels.

Thus, the improvement in company fundamentals seems largely a result of the management’s efforts at re-engineering the business model and does not factor any industry-wide / macro factors. This leaves scope for more upside on the performance.

Coming to the valuations, the Price to Book during the period has gone up from 4.40 to 7.40 and Market Cap to Sales from 3.80 to 9.80. So the stock is certainly more expensive than it was pre pandemic and is also valued more richly than others in the sector. What should be the steady state valuation of the new IHCL is not clear to me. Any views?

Disc: Have a small tracking position)