The share price of BSE has been rising for the past couple of months on the back of the exchange’s rising derivative volumes and also on market rumours of possible merger with commodity exchange MCX. In these couple of months, going pureply by the official filings of BSE and MCX, there has been no official communication from both the exchanges denying the rumours of a merger between them. The fact that MCX was desperate for technology-related solutions for its trading platform and could benefit from BSE’s technology and that BSE could strengthen its position if it got the support of MCX commodity volumes has encouraged market players to take the rumours seriously and push up the share price, brokers said.

Posts in category Value Pickr

Stocks with Temporary Setback (30-08-2023)

I started this thread to understand stocks that will go through temporary setback because of new developments in company, policy changes from government, changing public taste for products/services, increase in raw material prices or an X factor affecting the company’s performance.

Hope the investing community will educate us with daily happenings that will affect performance of company.

MTAR Technologies – A wager on innovation meeting economies of scale (30-08-2023)

Grant of Industrial License (Defence) from Government of India/ Ministry of Commerce & Industry/Deptt.

Speciality Restaurants (30-08-2023)

We believe the food sector will witness a robust sales growth in the high teens over the next few year – Source: Speciality restaurants Annual report.

Short and Crisp video on Speciality restaurant from Avinash Gorakshakar. Link below.

https://twitter.com/AvinashGoraksha/status/1667154639010111490?t=kj5Iw_DAlJuEEHM4IFKWRg&s=19

Currently ruling below 200 DMA at 205. Today Annual report also released …

https://www.bseindia.com/xml-data/corpfiling/AttachLive/504b9f70-313e-4ee6-84aa-a4a5c0f9421a.pdf

Kama Holdings Limited (30-08-2023)

If you like srf at current valuations, I believe kama holdings remains a better bet for long term.

The management is honest and shares rewards with shareholders, so a discount of 65 percent(reduced from 70 perc) is not warranted either.

52 week highs and all time highs strategy (30-08-2023)

Sir, do you consider volume, or only price? If you do, how much focus or emphasis do you place on volume?

Does volume need it to be incorporated in chart analysis, for all kinds of participants, or retail need not bother because of their smaller positions, and is the absence of high price move, but good volume a precursor to a big up move?

Your thoughts please.

Atul Auto Limited (30-08-2023)

25.08.2023 CNBC

- Will be able to recover Q1FY24 volumes over remainder of FY24, will try to exceed 30’000 units in FY24

- Focus is on regaining pre-covid monthly volumes of 3500-4000 units

- Selling 500-600 EVs monthly (L3 category; lead acid battery)

- Breakeven is achieved when they sell 2300-2500 vehicles monthly

- Awaiting FAME II certifications for L5 EV 3-W

- Petrol 3-W (developed during COVID) has been received well in export markets

- Exports will grow from 10% to 20-25% in medium term

Disclosure: Not invested (no transactions in last-30 days)

Gokaldas exports — cup and handle/rising channel (30-08-2023)

Following this.

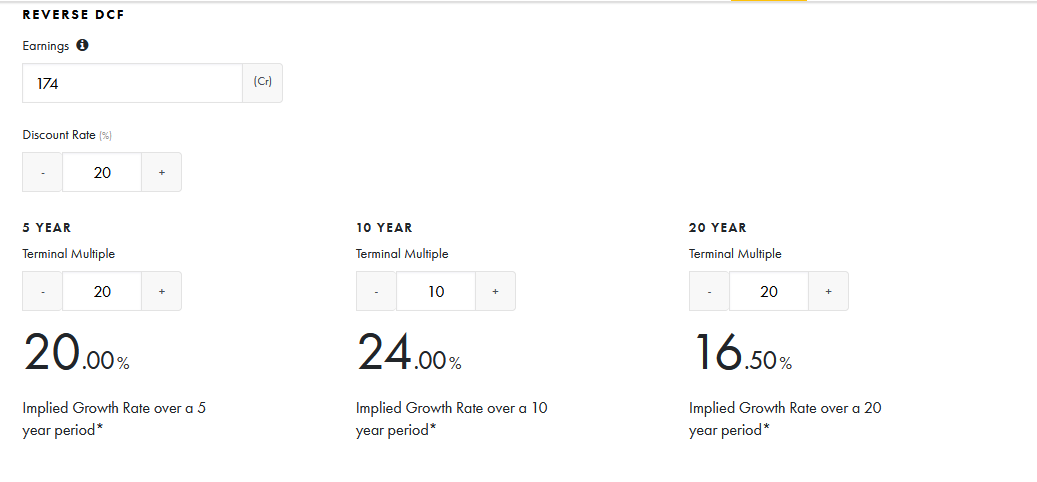

I just did the Reverse DCF for Gokaldas after the ~38% jump in share price over the past 2 days.

Used TTM PAT as the Earnings input (which is a conservative estimate only as net PAT over past 5 years divided by net CFO over the 5 years is 49%). Assuming that I wish to make 20% CAGR over the next 5 years, the implied growth rate still comes out to be 20%.

With the increased number of FTA agreements in discussion and likely to be concluded over the next few years, would it be fair to say that Gokex is still fairly valued?

Disc: Invested and Tracking. Noob alert.

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (30-08-2023)

They gave a generic statement saying “we will maintain margins”. But they categorically said Q1 margins were too high owing to large export skew. Prior to that,company maintained 22% EBITDA & with capacity nearing 100% util I would assume atleast 22% should be sustainable margins for Fy24.

Sirca Paints India Limited (30-08-2023)

Read the announcements carefully. Their AGM was held on Aug 25, so wait for 30 days.