@DEBASHISH sir would love to know your analysis and take on this. I remember you mentioning about private placement and waaree RTL ![]()

Thanks

Posts in category Value Pickr

Reverse Merger- Sangam Advisors (29-08-2023)

Bull therapy 101-thread for technical analysis with the fundamentals (29-08-2023)

I believe ‘last leg/rally’ etc are not for me to predict. I prefer to build in a strong thesis and invest after evaluating if the risk/reward is favourable. Have mentioned both risk and thesis pointers above clearly.

Just food for thought, but the corporate governance shady past could be priced in already being quite old?

What remains to be seen is if the business fundamentals improve and the market perception of the company can become slightly better if these issues don’t crop up again. Blind pessimism can be a friend in the market sometimes!

MPS Ltd (29-08-2023)

Another Acquisition

Liberate Learning Pty Ltd (Australia), Liberate eLearning Pty Ltd (Australia), App-eLearn

Pty Ltd (Australia), and Liberate Learning Limited (New Zealand) (“Liberate Group”).

MPSi agreed to acquire 65% of the shares held by the shareholders of each entity of

Liberate Group for a consideration of AUD 9.32 Million which is payable as per the terms

of SPA and other transaction documents.

The remaining 35% shareholding of each of the entities of Liberate Group will be acquired

by MPSi in subsequent tranches based upon valuation methodology as agreed under the

transaction documents.

Looks like a 50 crore acqusition (for 65%) of a co doing a revenue of 45 cr at 40% margin !!

Here is the link to the Liberate group https://www.liberatelearning.com.au/ Client profile looks whose who in Aus, starting from BHP Billiton onwards !!

PS – invested

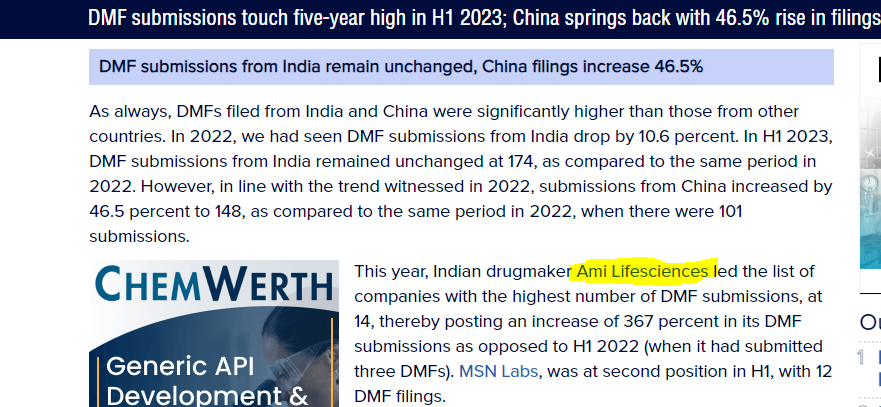

Ami Organics – Pharma Intermediates & Specialty Chemicals (29-08-2023)

Is AMI Lifesciences forward Integrated with AMI Organics. ?

I have not read this thread fully , forgive me if it was discussed earlier

Note: Have taken a position recently

Piramal Enterprises Ltd (29-08-2023)

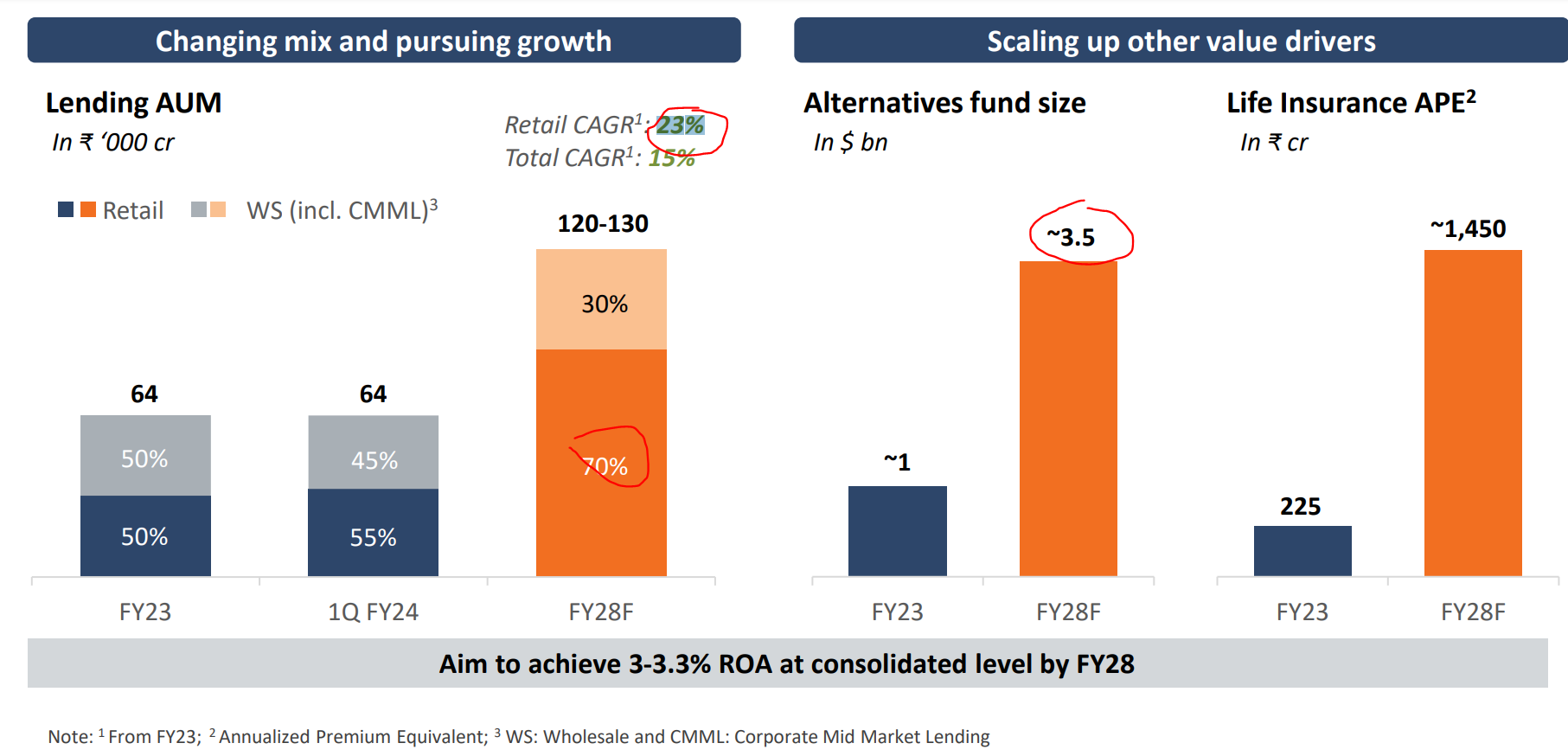

PEL published investor day PPT. It is very detailed and provide their aspiration for FY28.

Key Takeaways:

-

AUM growth outlook: Based on recent performance, they are cautious about retail growth. Although the base was small, now they have invested in technology and opened up many branches, which can be a positive surprise going forward.

-

More than tripling Alternative funds size. This shall increase the immediate fee income (in the next 3 years), but it will not have a meaningful impact on carry payment as the carry comes 3-5 years after investment as it is one of the most important parts of alternative returns (Chery on the cake). PEL generally do not say much about this segment. Once it reaches $3 billion, it will be interesting to see how it shapes up.

-

There is a huge growth in Life insurance, but it may impact the balance sheet as Life insurance is growing much faster, and it may not be profitable yet due to the huge investment they are making in growth.

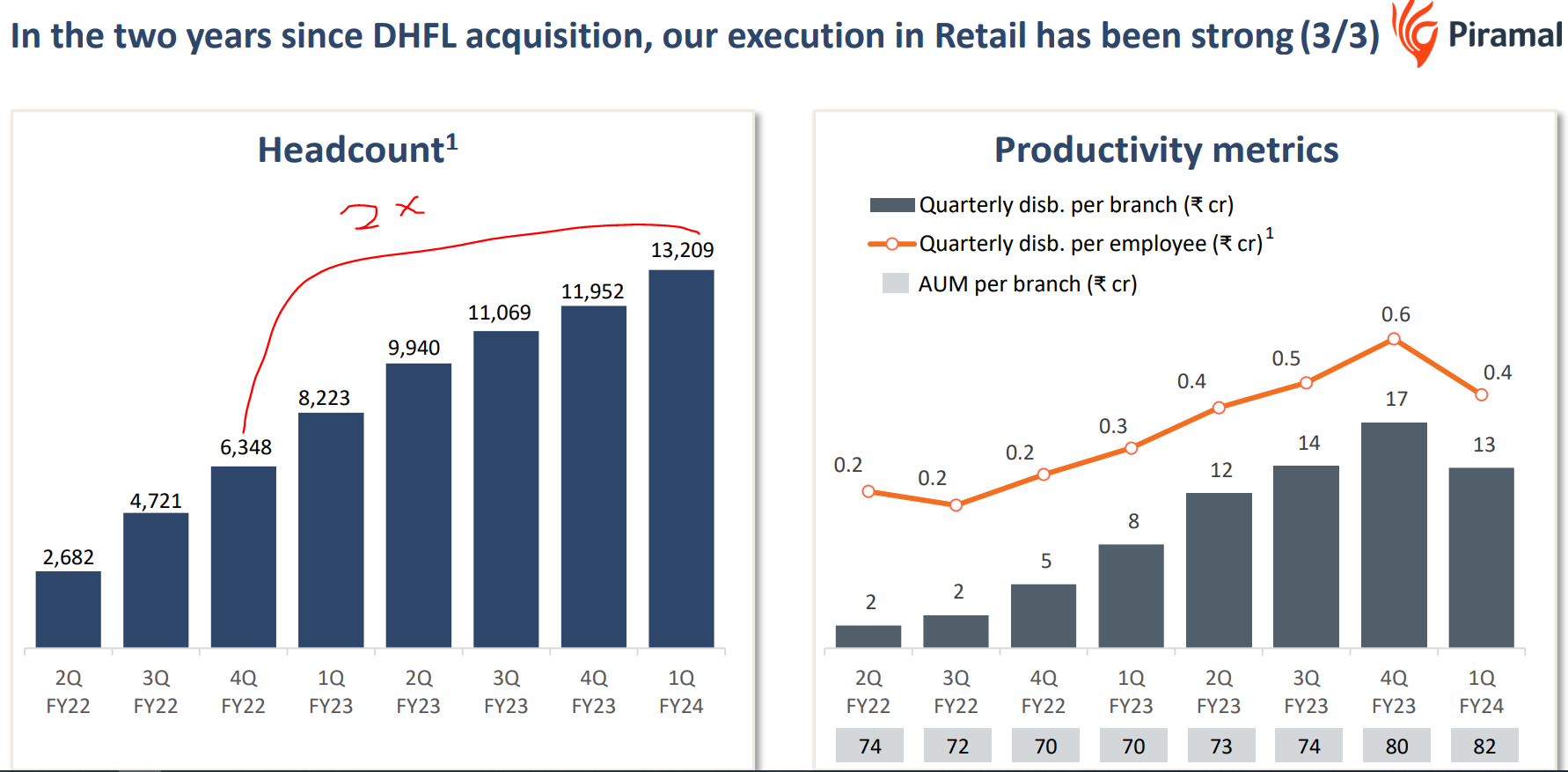

Productivity Metrics

- More than double the number of employees in 5 quarters (well after DHFL acquisition). They have invested huge upfront in building and strengthening the retail front end. The current P&L shows the cost, but not all benefits are realised yet. As they increase the contribution from retail, I think the operating leverage will play out, helping their profitability.

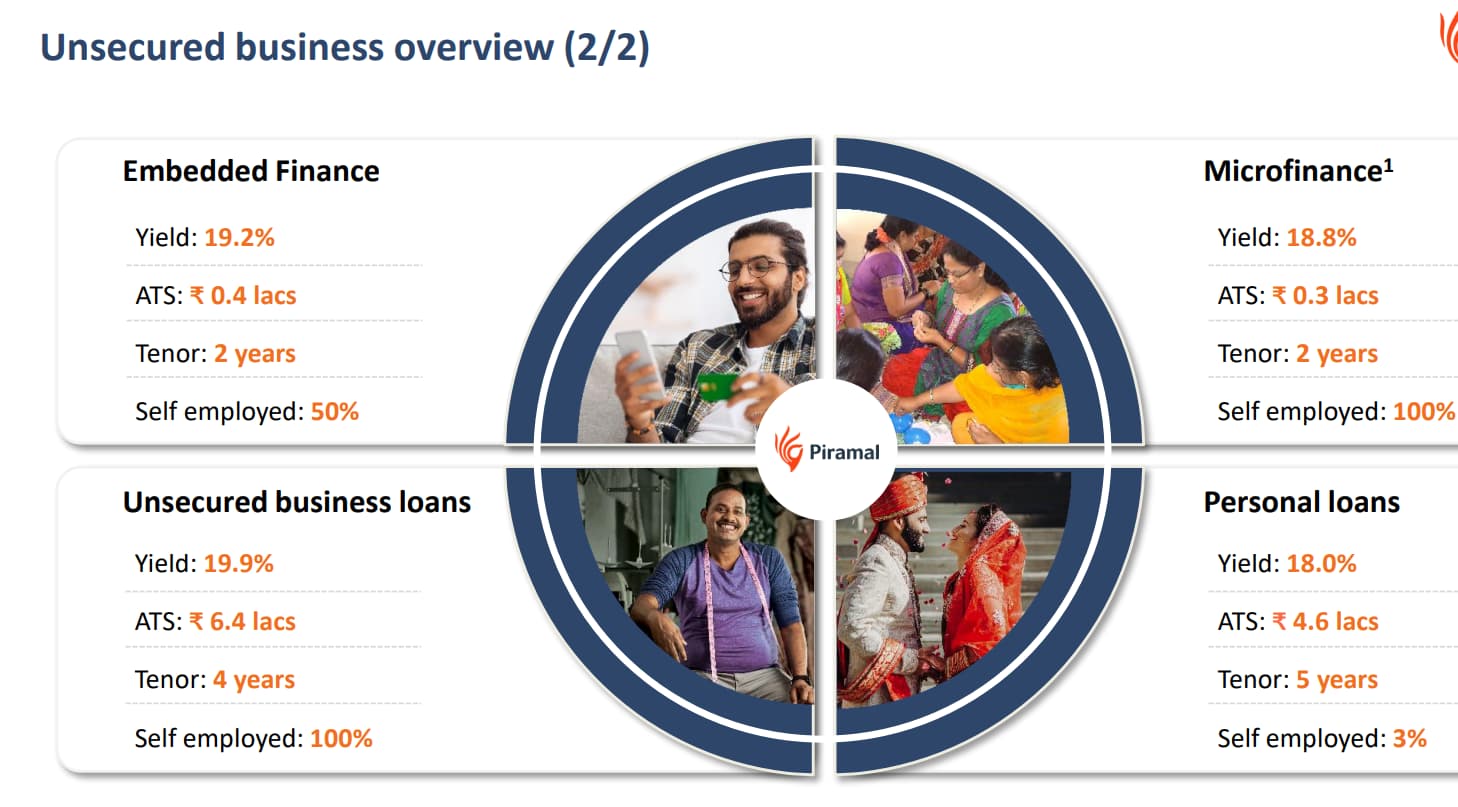

3- Unsecured

- I think this could be the bone of contention. They have ramped up disbursement massively- 40X in 7 quarters. Although the yields are much better, PEL’s records in managing the risk-adjusted return are bad.

-

During 2018/19, they were thumping their chest and saying a lot of things about the quality and how they monitor of their portfolio. They even said that RBI had applauded their portfolio tracking. Fast forward 4 years, they have lost all (or most of) profit due to bad loans.

-

So I would personally not read too much into it now. It is concerning that they are ramping up risky segments very fast, which his fraught with risk. They had difficulty managing secured lending to real estate developers (2X security for the loan), but still made massive provisions how this unsecured fear is a thing to watch. I hope they manage this well after learning a thing or two from Wholesale 1.0 debacle.

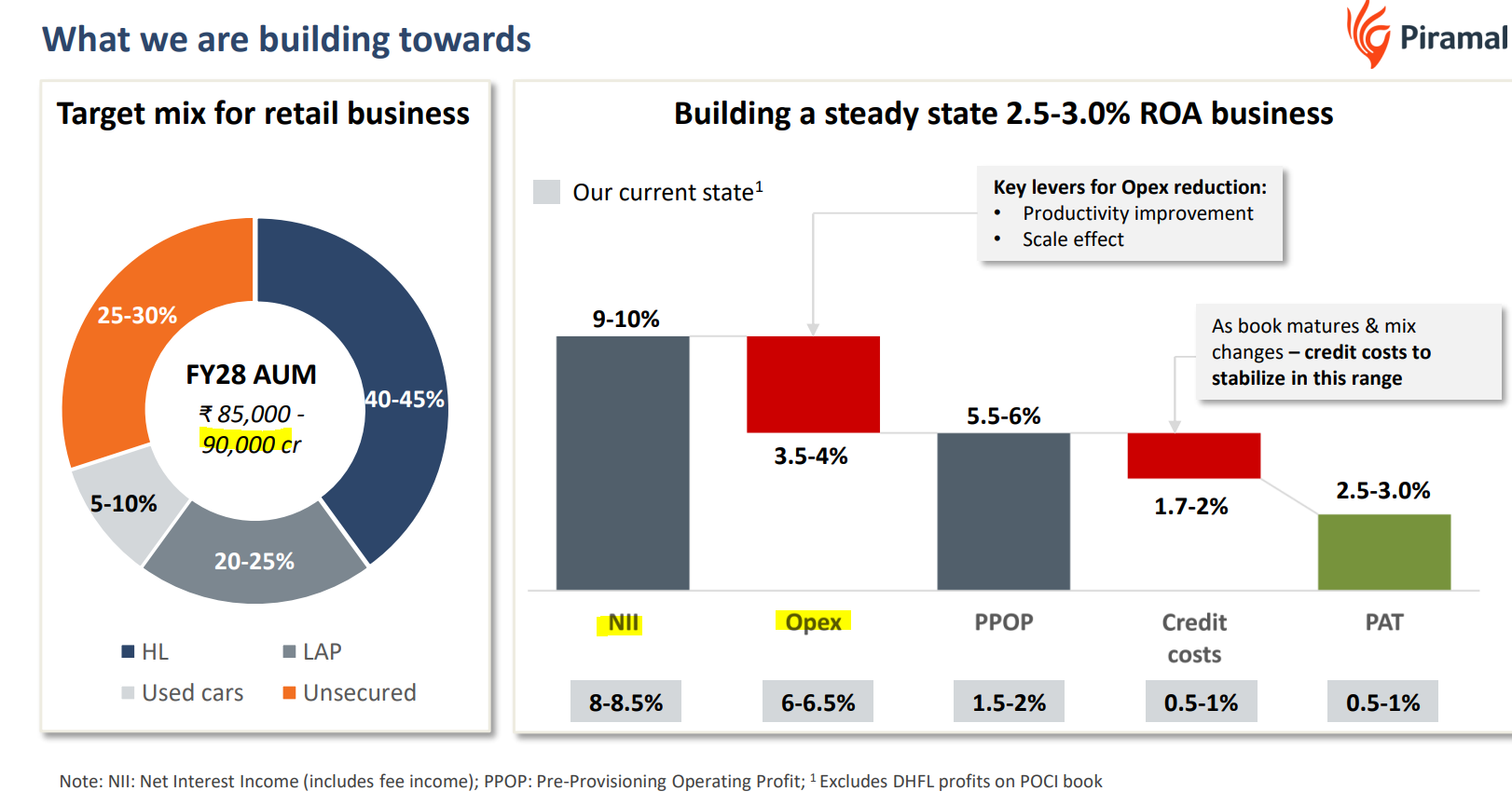

FY28 Aspiration breakdown

-

This is one of the most important slides and provides a glide path for the portfolio. Retail AUM target is 90,000cr (Fy23 is ???).

-

The improvement in ROA is likely to come from Opex reduction or operating leverage play along with NIM improvement.

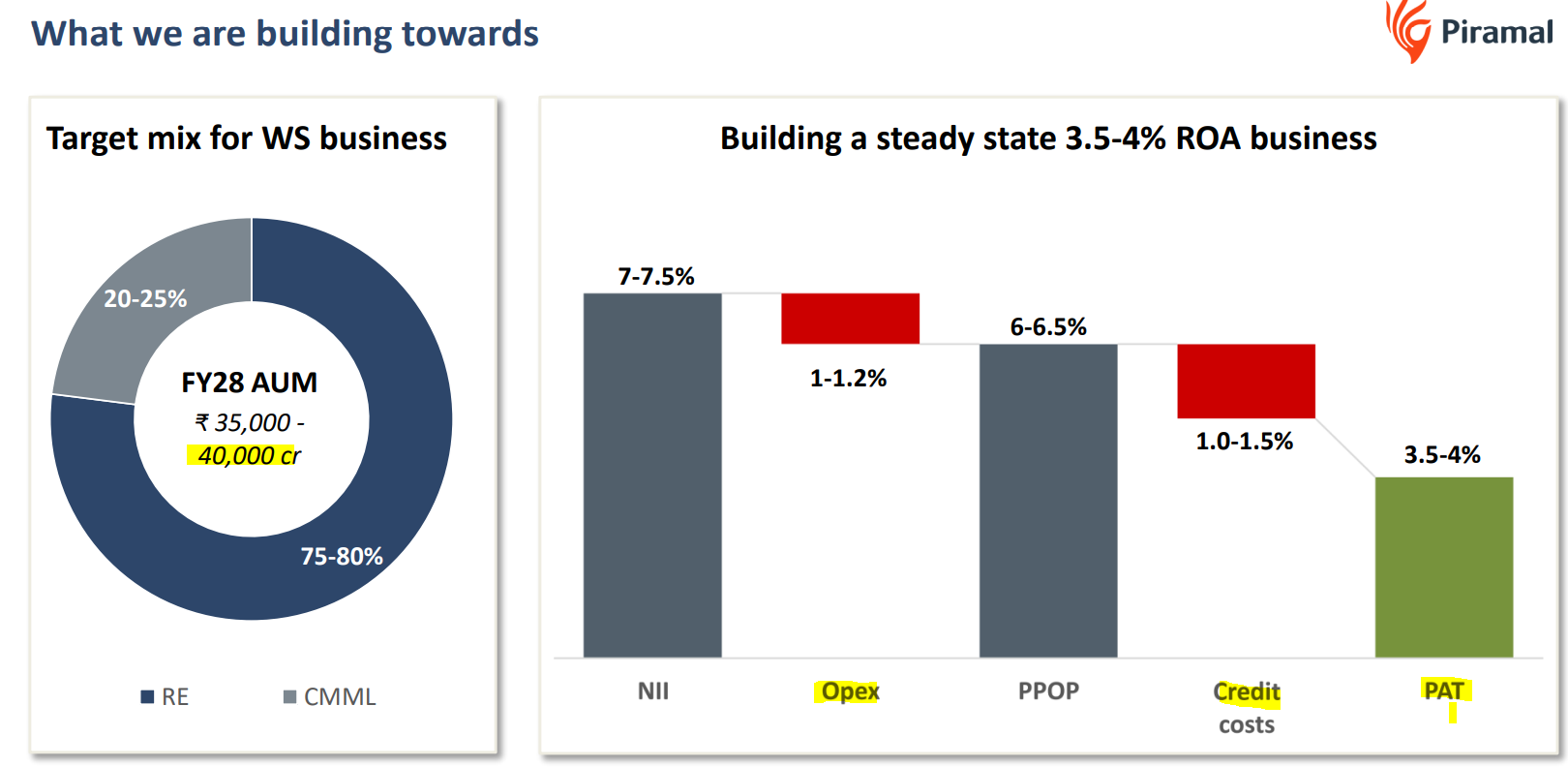

New Wholesale

Large exposure to land purchase. Even if they manage it well, the market will not like it and is not likely to give a high valuation to this part. So even though it may be more profitable than retail, but if one goes by their own record, the wholesale profitability can disappear in a flash. Hopefully, PEL is lucky second time, and I hope that it fares better than the wholesale 1

Overall good read and they are providing PEL’s aspiration. I think PEL will need 2/3 quarters to clear the book before they start reporting better numbers.

Note- Long term invested

KPI Green- Turning Sunshine Into Cashflows (29-08-2023)

As I said earlier it should be a trade secret and being a trade secret it isn’t public and I haven’t bothered to know either as my on-ground research and forensic accounting have given me enough conviction of no wrongdoing. Can’t share every resource as it’s time-consuming to find where exactly I found what but about the speed it was about in the last con call and their cash conversion cycle says it, Please go through that and I think you should get in touch with the company secretary for better clarity as almost all companies do not publicly disclose such information.

Escorts Limited – Playing for Margin Expansion (29-08-2023)

Some unconfirmed news on the counter. I suspected this might be one of the next steps, since the Mid Term Business Plan details in the Auuunal Report were very generic for the Railway business, whereas for Agri they had mentioned definitely plans on capex. Construction Equipment business also am not sure, if they want to retain if Kubota is not having similar products.

We have to wait to see how this benefits minority investors or not. I would have preferred if they demerged this business, distributed shares to minority investors, listed it seperately and then sold the promoter stake to buyer. If its a slump sale, then the cash hoard just increases.

India’s Escorts Kubota mulls sale of railway equipment unit -CNBC-TV18 | Reuters

Gokaldas exports — cup and handle/rising channel (29-08-2023)

Notes on Atraco Acquisition

(from Company release, Management Interviews & con-call)

Quick info on Atraco:

It’s a well-established Dubai-based garment manufacturer.

The HQ in UAE covers functions of Product Development, Marketing, with Manufacturing based in Africa (4 units in Kenya & 1 in Ethiopia)

The co produces about 40 Mn garments (with a 74:26 mix in Woven & Knit).

And the customers include 40-50% Children (newer segment for Gokex)

Co is tax-free, being based out of Dubai.

Customer base is 95% US based with only 1 common customer

The key advantage it offers is being a low-cost duty free manufacturer.

Kenya has duty free access to US. The agreement governing it, AGOA is due for extension in 25, The management is confident of the extension.

Ethiopia has duty free access to Europe, while US access has been temp suspended.

Financials

Group’s revenue is about $107 Mn with a profit after tax of $7.2 Mn for 2022. (after a 1 time cost of $1Mn)

That is at 30 & 35% of Gokex Revenue & Profitability base.

So the company is of a substantial size from Gokex standpoint.

The EBITDA (adjusted) – 10.5%

Could improve by 1.5 -2 % in 2-3 yrs from Productivity gains, Modernisation . Management expects a growth of 25-30% in next 2-3 yrs

And would be incurring Capex of 4Mn in FY24/ 25

The current utilisation is at 88-89%

Valuation

The deal valued at $55 Mn & expected to close by Q3.

It is funded by mix of debt (40 MN $) and internal accruals

They have Working Capital of $35Mn & Debt of $15 Mn.

That makes the deal’s effective cost to be $35Mn (55-35+15)

The Owner is aged & selling to ensure proper Succession to Legacy.

The Mgmt is seasoned & to continue.

Previous Expansion plans

Gokex had suspended the Bangladesh expansion plans for time being, with multiple factors in play – rising Cost structures (min Wages to be revised) & global perception becoming less favourable.

Capital Allocation

The Management’s clearly focused on anything being a strategic fit first –

Adding capabilities in Low Cost regions, and ensuring sustainability of operations.

Further, looking at Attractiveness of the Opportunity – this deal provides comfort as it is akin to Buying Growth at low Valn.

Mgmt has been extremely focused on being Conservative & Execution oriented.

With this deal, GokEx moves towards being a truly global garment Exporter.

Disclosure – Invested & Biased.

Sources – Concall, Media release, Interviews on CNBC TV 18, BQ Prime.

https://twitter.com/CNBCTV18News/status/1696383371738599424?s=20

IDFC First Bank Limited (29-08-2023)

thats exactly what i have done.