Yes you are correct, we are just exploring possible verticals for future. We can stop this discussion if you want as it doesn’t add value to this forum as of now.

Posts in category Value Pickr

Olectra Greentech – Electric Bus Opportunity (07-10-2024)

Per the Q1FY25 transcript, they delivered 156 E-buses. No tippers were delivered in Q1FY25.

Krishca Ltd : A SME offering steel strapping Solution (07-10-2024)

I dont think management is thinking about it as of now…since they have lot to do in steel strapping and packaging itself…

Vaidya Sane Ayurved Laboratories Ltd (Madhav baug) (07-10-2024)

Hi,

I attended the AGM. Sharing the notes:

-

Been in Ayurveda for 24 years. (Inspired by his father when he was admitted to ICU)

-

Hospitals in- Khopoli, Nagpur, Vizag, Clinics- 350

-

Revenue Bifurcation

-

20% Hospital

-

70% Franchise

-

10% Clinics

-

-

80% are franchise, 20% are company owned.

-

Patients who come to us majorly have Diabetes, Blood Pressure, and Heart disease (heart patients have more ticket value)

-

New patients around 6-7K every month, 25% are getting enrolled for regular plans with us

-

We have a whole month of Diet Kit in a 6-7 Kg box. It contains breakfast, lunch evening snacks, dinner, chai everything is into it and the patient doesn’t have to go hunting for any kind of food material anywhere outside.

-

Have a comprehensive care plan that helps patients manage and even reverse their chronic conditions. We are proud of our annual care plans, which ensures that patients stay with us for an entire year, receiving consistent, follow-up, and care.

-

Herbal Medicine dispensed by the franchise Clinic to the patient, in this

- Franchise Margin- 40%, Company Margin 60%

-

Therapy: Supposed to be consumed inside the clinic for the therapy of the patients

- Franchise owner margin 70%, Company Margin 30%

-

Diet Kits

- Company margin is 55%, and Franchise Owner Margin is 40 to 45%.

-

NABH accredited hospital, CGHS covered, Insurance covered cashless facility

-

Production gradually has been starting in these 2 factories, about 85 to 90% of the medicines have been manufactured in this Dynamic Factory already.

-

In the UV Factory, we have reached about 40 to 45% of food products being manufactured, and the rest of them will be manufactured in the next about 3 to 6 months.

-

About 100 more beds are to be added to hospitals over the next 12 to 24 months in phases.

-

Working on improving CRM, internal branding

-

Plans to add 10 or more hospitals, Plan to expand hospitals through acquiring sick resorts, and hospitals.

Krishca Ltd : A SME offering steel strapping Solution (07-10-2024)

Steel strapping is a good start , once you start making some money you will look for newer verticals to add.

So from Steel Straps to Strapping Contracts to Packing Contracts to Specialty Steel division to Welding consumable and so on…

Looking at Crown one can visualize what kind of newer verticals one can add.

Krishca’s edge is it’s manufacturing , once you start dealing with specialty steel & high precision steel products, all these verticals open up , now it’s up to management to decide which vertical to enter and when Currently focus is on strapping & packing business only.

HBL POWER SYSTEMS: Booting-up for the Race of the Century (07-10-2024)

Submarine batteries. HBL Power

Krishca Ltd : A SME offering steel strapping Solution (07-10-2024)

Hello Rocket !

I am still studying Krishca. while its interesting i am yet to invest .

I’d like to understand comparison of Krishka to Crown & Signode with respect to market size.

Crown is a giant in packaging…it mostly does metal cans…beverage(let say all types of food grade tin cans)

Its subsidiary Signode does packaging of many types(Corrugated (containers), Stretchfilm (wrapping),jumbobags(plastics containers),steel straps (wrapping).

My understanding with containers demand is …there existists large market in terms of colume requirements. on the otherhand the wrapping volumes(all type of wrapping plastic as well as metal) are lesser compared to containers.

are you saying krishca could/plans also get into the tin container packaging business ? i find the market size to be large of tin containers if krishca is able export…however i would like to know more if krishca can also enter into other type of packaging business which Signode does.

Vaidya Sane Ayurved Laboratories Ltd (Madhav baug) (07-10-2024)

Hey guys, did any of you attend the last AGM? Anything of note?

Selan Oil Exploration (07-10-2024)

Selan : Sept 24 AGM notes

-

Business overview

a. 70% volume is from oil and 30% is from gas

b. Field wise – approx. 60 -65% of sales volume is from Bakrol , while 30% is from Karjisan. Lohar has smaller contribution

c. Confident of delivering on the guidance for full year (30 to 35% higher avg sales than FY 24) -

Bakrol field

a. Drilled 6 wells in Bakrol. Production from these wells is as much as that from all other older wells

b. Looking to drill more wells in Bakrol

c. Extension sought for Bakrol. to drill beyond 2030. EC process is on -

Karjisan

a. Should see ramp up of gas production from the field

b. Commercial gas sales to a new gas buyer has commenced in Q2 FY 25 -

Lohar field

a. Focus on opex reduction to continue and on sustaining production levels

b. Extension sought for Lohar beyond 2030 -

Duarmara (in Assam) – On track to commence drilling by end of FY’25

-

Elao field – more of an opportunistic acquisition. Not supposed to have a big contribution to volume

-

Macro view

a. Seeing a lot of support from the Govt; as we move from offshore to onshore drilling

b. No impact of Windfall tax cut as company doesn’t come under ambit of windfall tax

c. Gas prices continue to be robust

d. Expecting gas to play a big role in decarbonizing ; bigger portion of Antelopus would also be gas

Disc: Invested

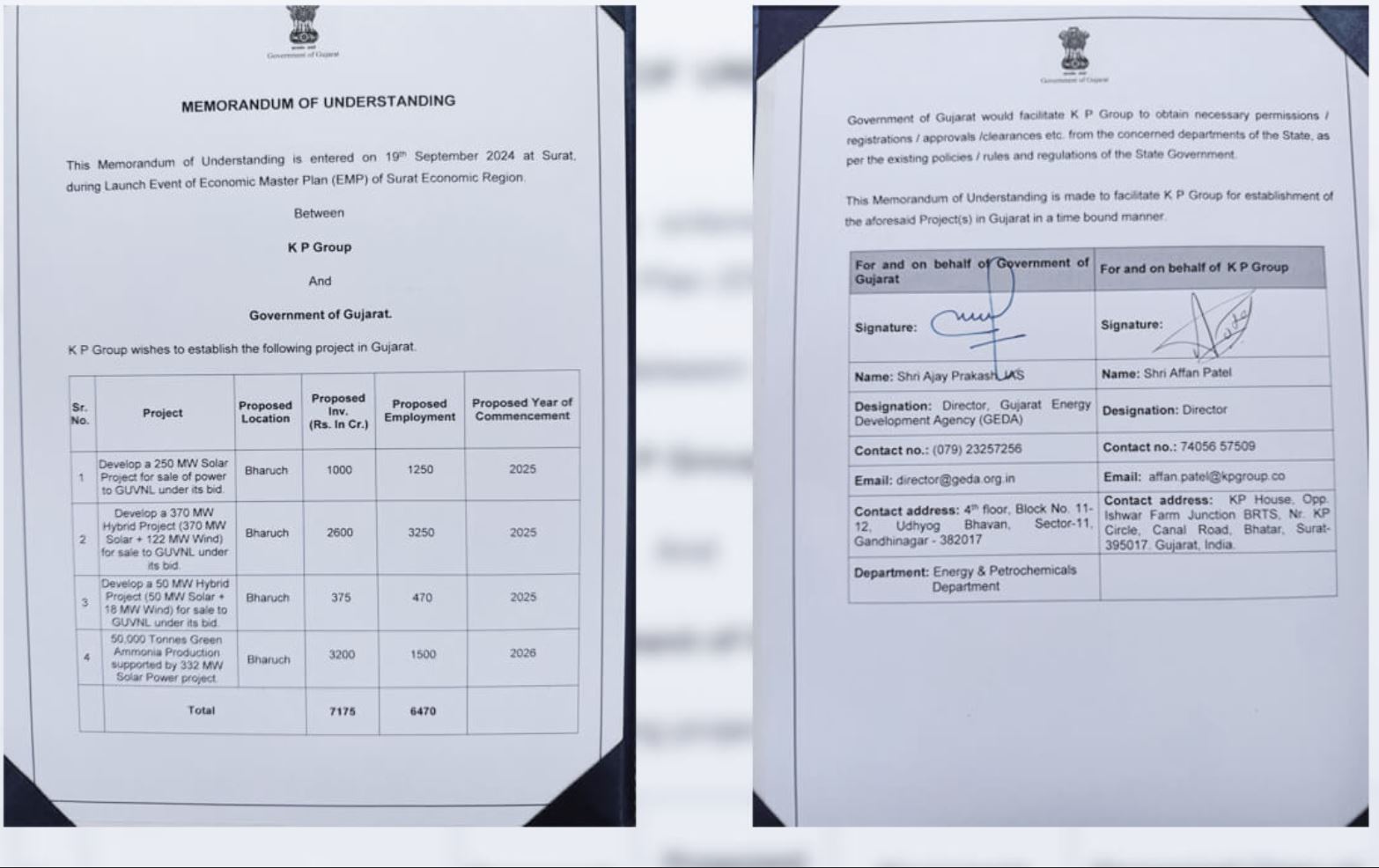

KP Energy – Lotus in muddy water (07-10-2024)

Already having 1GW order book and recent kpel signed memorandum with Gujarat government