Avantel core business has found robust footing. I hope to see sales improving in the near future.

I would be more interested in Imeds global picking pace. A new high growth segment turning profitable should be good news for shareholders.

Avantel core business has found robust footing. I hope to see sales improving in the near future.

I would be more interested in Imeds global picking pace. A new high growth segment turning profitable should be good news for shareholders.

A little rough work from my end.

A gradual move into switchgear will help improve sales in Lighting due to complementary market position similar to fans. Wires may not be high margin but it will help increase economies of scale as copper wires are the main component of all other items manufactured by Crompton.

White goods market is a bigger and tougher nut to crack with only a couple good names like Voltas and Symphony having the sustainability in the extremely competitive market. Others like IFB and Onida are still struggling. Still, acquisition of a legacy brand with good recall like Onida for e.g.( they were looking to sell before) can work similar to butterfly acquisition.

Just my thoughts. No news confirmations ( rumors )or buy/ sell recommendation.

the products are not manufactured by shankara but traded, they just capture the spread, no value add or further processing by them.

now they are adding higher margin non steel products, which will increase margins as well as ROCE

Hi All,

I got this company through screener of 100% Revenue growth in less than Rs 110 cr company .

Pace e commerce company is pune based company dealing in Kids stuff. Recently I Visited the site of PACE E Commerce company-“cotandcandy.com” . Where they sold products like Beds,storage , carpet , table chair, footwear, clothes & toys for boy & girls.

From Current business of Kids- company had made revenue of Rs 28 Cr in FY23 v/s RS 11 Cr in FY22. EBITDA of Rs 1.31 Cr in FY23 v/s Rs 0.92 Cr in FY22. company is profitable in both the years. Company is under SME segment and reports financials half yearly.

This company is operating in children online products required in daily basis. In FY23 Revenue growth was more than 100%- Rs 28 Cr sale , interesting part is that it is Profit making online company growing at this rate.

Balance sheet

Networth Rs 29 cr

Borrowing Rs 4 Cr

Market Cap Rs 49 Cr

EBITDA Rs 1.31 Cr

Total Enterprise value= 53 Cr

EV/EBITDA= 41

PE= 37

this was financial for old business. Company is doing only online sale of kids product.

In year 2022 company has appointed a new fashion designer and launched a brand : “OSTILOS” this year in June 2023 for WOMEN. They will do online sale of products under brand name “OSTILOS”. In coming year Company will add new products for MEN also as per website column.

Currently this brand is showing Dress, Tops, Bottom Wear & T-shirts, which will further increased in other types of design also.

Total range of products are 33 for women under brand ” OSTILOS”.

Promoter is already doing online business for kids in which he is showing growth, so in new Fashion online business also huge chance of growth

Lets see how the new brand will do in coming years.

||Mar 2020|Mar 2021|Mar 2022|Mar 2023|

|Sales +|1.49|1.70|10.46|28.37|

|Expenses +|1.42|1.38|9.54|27.06|

|EBITDA|0.07|0.32|0.92|1.31|

|OPM %|4.70%|18.82%|8.80%|4.62%|

|Other Income +|0.01|0.02|0.05|0.03|

|Interest|0.06|0.23|0.22|0.56|

|Depreciation|0.01|0.01|0.02|0.02|

|Profit before tax|0.01|0.10|0.73|0.76|

|Tax %|0.00%|30.00%|27.40%|18.42%|

|Net Profit +|0.00|0.07|0.54|0.62|

Please do your own research before investing.

CMP 1912

Seems that it is starting the next leg.

Sika Interplant Systems🚀Stock Analysis🧐🔥Best micro cap stock✔️

Aerotek SIKA is already a joint venture

I am intrested , please add me too.

yes, and this acts as a switching costs for oems, there is no substantial savings for them in changing suppliers.

hence unless there is inferiority in quality of product, suppliers aren’t changed.

high customer stickiness

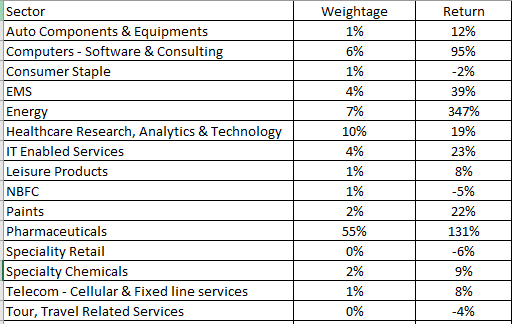

PF :

| Serial | Stock Name | Buy Price | CMP | TODAY | Weightage | Return | Holding Days |

|---|---|---|---|---|---|---|---|

| 1 | LAURUSLABS | 344.69 | 394.6 | 0 | 36% | 14.48% | 23 |

| 2 | NEULANDLAB | 2100.01 | 4055 | 2 | 14% | 93.09% | 210 |

| 3 | SYNGENE | 682.35 | 810.45 | 1 | 10% | 18.77% | 182 |

| 4 | PRAJIND | 296.41 | 487.3 | 0 | 5% | 64.40% | 282 |

| 5 | AXISCADES | 452.44 | 555.5 | 1 | 4% | 22.78% | 97 |

| 6 | SYRMA | 346.72 | 482.5 | 1 | 4% | 39.16% | 147 |

| 7 | ORCHIDPHAR | 579.69 | 577 | 0 | 3% | -0.46% | 82 |

| 8 | NEWGEN | 499.57 | 949.95 | 0 | 3% | 90.15% | 109 |

| 9 | SBCL | 146.02 | 558.95 | 2 | 2% | 282.79% | 182 |

| 10 | MASTEK | 2155.64 | 2189.4 | 2 | 2% | 1.57% | 7 |

| 11 | DMCC | 309.66 | 326.4 | 1 | 1% | 5.41% | 132 |

| 12 | JUBLPHARMA | 453.95 | 472.4 | 2 | 1% | 4.06% | |

| 13 | KAMOPAINTS | 177.97 | 190 | -1 | 1% | 6.76% | 7 |

| 14 | OKPLA | 109.25 | 117.9 | 5 | 1% | 7.92% | |

| 15 | SIRCA | 365.86 | 421.4 | 1 | 1% | 15.18% | 105 |

| 16 | GABRIEL | 251.71 | 282 | 2 | 1% | 12.03% | |

| 17 | JUBLINGREA | 465.49 | 485.3 | 2 | 1% | 4.26% | |

| 18 | LATENTVIEW | 413.56 | 427.25 | 1 | 1% | 3.31% | |

| 19 | TATACOMM | 1694.61 | 1827 | 0 | 1% | 7.81% | 7 |

| 20 | PATANJALI | 1306.83 | 1278.1 | 0 | 1% | -2.20% | 7 |

| 21 | GUFICBIO | 241.17 | 285.95 | -1 | 1% | 18.57% | 109 |

| 22 | JIOFIN | 225.03 | 213.45 | -5 | 1% | -5.15% | |

| 23 | EASEMYTRIP | 41.19 | 39.75 | 2 | 0% | -3.50% | |

| 24 | BCONCEPTS | 454 | 426.3 | 0 | 0% | -6.10% | |

| 25 | FLUOROCHEM | 2892.1 | 2877.45 | 1 | 0% | -0.51% | 21 |

| 26 | SUVENPHAR | 515.25 | 519.85 | 0 | 0% | 0.89% | 7 |

How you should read this chart is for example : 55% of my Portfolio allocation : I did make 131% returns now at the entire portfolio level (XIRR) can be very low

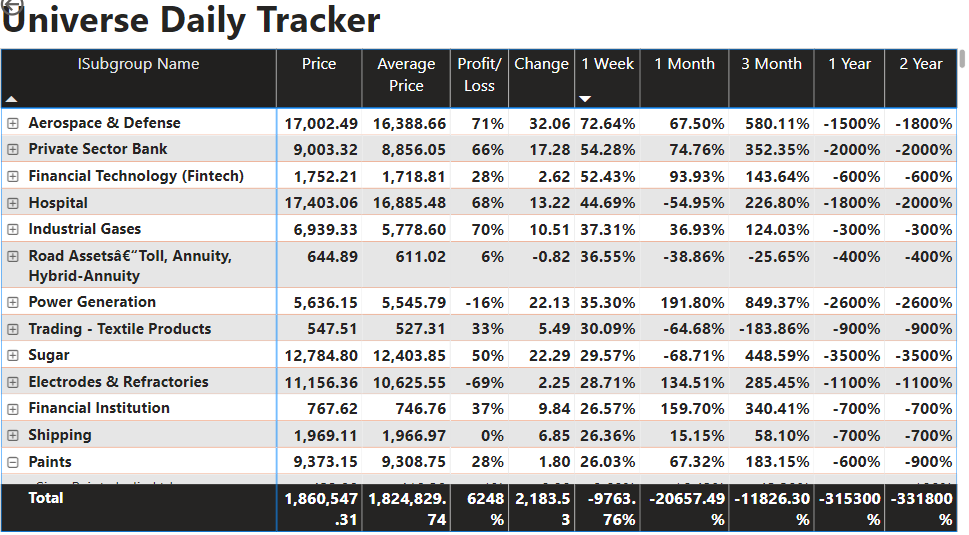

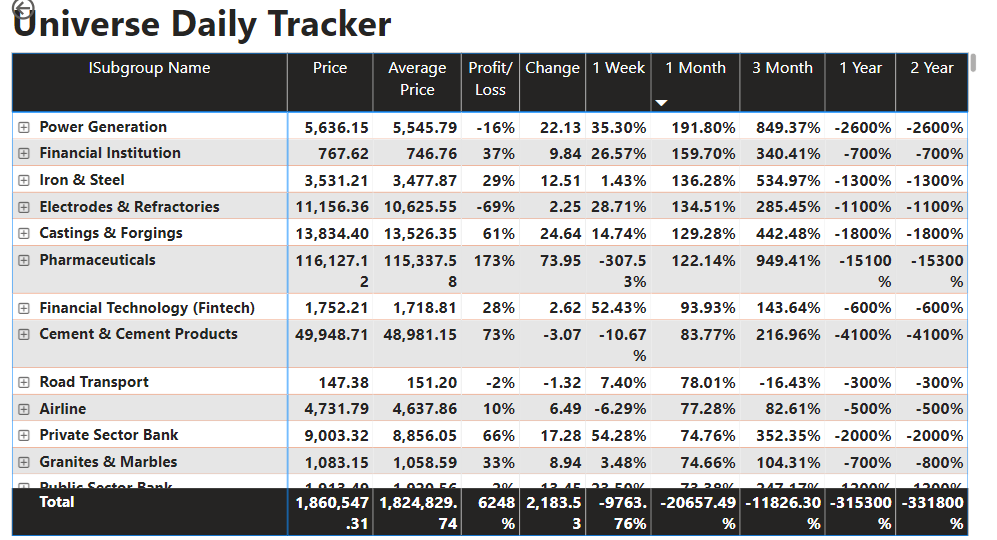

My Own Tracker for all BSE listed stocks :

Week wise

Month Wise

Cheers

I don’t know am still not convinced with the Banks

Firstly I understand the banks will do well in next 12 month

Secondly after 12 months there will be NPA issues

Thirdly Bank profit pools are not too narrowed example in banks there are many and so thus the concentration pool of profit gets dispersed

I understand the fact not all banks are the same, they have different strategy but still not convinced.

@Sudhanshu_Shekhar : Helped me to fast track with the banks but given the small finance banks – there is SURYODAY, EQUITAS, UJJIVAN, FINO (coming in) many more if they come in – I am quite skeptical the earnings will get dispersed.

Now Why JIOFIN? : See BAJAJ FINANCE was the only Big fish in Ocean and there is a premium scarcity to it, same way as you see in the same Ocean JIO has arrived with low cost of funds to grab more share – that’s why am interested and hardly there are 2 tough players with solid background

I am interested , please add me too.