Growth is clearly visible in the numbers but the return ratios are disappointing .ROCE is around 10 percentage.Management is not walking the talk interms of working capital.Its increasing

Posts in category Value Pickr

Hitesh portfolio (19-08-2023)

To the above two comments, i add this about PSEs like PFC, NTPC, REC, Power Grid and such in the field of power generation and distribution:

Does the meteoric rise in stock price in some of these reflect earnings growth or is it a case of optimism on renewable shift in future? What is the basis of sentiment change? Assuming these companies will anchor or herald the shift to renewables, will it translate to investor wealth given govt control on multiple things including pricing power?

Does government no longer controls the pricing? Has the ROE cap at below 15% no longer there in some of these?

For example, Coal India appears in Graham’s 10 years earning screen, monopoly, huge earnings, cash pile etc…still it has destroyed investor wealth in all these years.

Privi specialty chemicals – Waste to wealth story (19-08-2023)

Privi speciality chemical

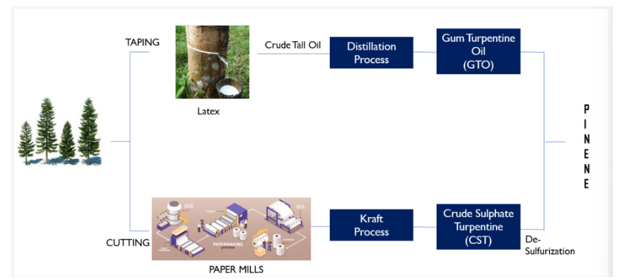

• Privi is India’s largest manufacturer and exporter of aroma chemicals. Almost one third of the aroma chemicals produced globally are made from chemicals obtained from a Pine tree. Company started with only 2 products in 1992 and today have expanded their portfolio to over more than 74 products. And expects to keep trend going forward with three to four new products launch each year. Company has two manufacturing facilities at Mahad in Maharashtra and Jhagadia in Gujarat.

• Privi speciality operates in aroma chemical which are used in fragrance and flavour industry used in soaps, shampoo, detergents, cosmetics and toiletries and the most importantly in perfumes. The company cater to the worlds 10 largest fragrance companies and have a significant presence in Europe and USA. 70% of production of Privi comes from pine tree.

Pinene based products- Dihydromycrenol(dhmol) and Amber fleur accounts for sizeable revenue. Both these chemicals are used in fragrances

- Dhmol is also called as God’s molecule as it is used in 99% of the perfumes, and Privi controls around 30% of market share of dhmol in the world.

- Amber fleur is a royal molecule of F&F(Flavour and fragrance) industry because of its velvety nature. Expected growth of this product is around 5-6% pa.

WHAT I LOVE ABOUT THIS COMPANY WHICH MADE ME DIG DEEPER ABOUT THIS COMPANY IS ITS WASTE TO WEALTH STORY.

Waste to wealth story depicts how this company makes revenue through by products of different raw waste materials using technology and with guidance of good R&D team.

Both crude sulphate turpentine and gum turpentine oil are natural products derived from pine trees, but they differ in their extraction methods, composition, uses, and quality. Gum turpentine oil is obtained through the distillation of pine oleoresin and is commonly used in various industries, while crude sulphate turpentine is a byproduct of the pulp and paper industry.

Difference between GTO and CST

GTO Method

• Gum turpentine oil is obtained directly from pine trees. When the bark of pine trees is cut or wounded, a sticky resin is exuded, known as oleoresin. This oleoresin contains gum turpentine oil and rosin. Gum turpentine oil is obtained through the distillation of this oleoresin.

• Gum turpentine oil is a more refined product compared to crude sulphate

turpentine. It mainly consists of alpha-pinene and beta-pinene, along with smaller amounts of other terpenes. The distillation process results in a purer and more standardized product.

• GTO process is the most common way is being adapted by most companies

• Major raw material supplier of GTO is China accounts for around 70% of worlds production.

CST METHOD

• Crude sulphate turpentine is obtained as a byproduct of the Kraft pulping process used in the paper and pulp industry. When pine wood is processed to produce paper pulp, chemicals are used to break down the lignin in the wood. As a result, crude sulfate turpentine is released as a byproduct.

• Sulphur content in CST is too much which has very foul smell which needs to go through refinery process to make it suitable for aroma chemical

In Asia only PRIVI is the company which has refinery to refine CST

Privi has long term tie up with the world largest mills for raw material supply. Privi has Right to first refusal to this raw material

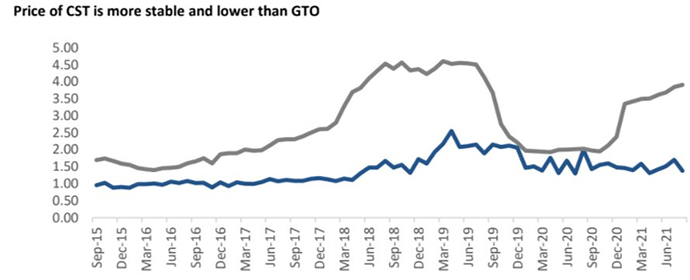

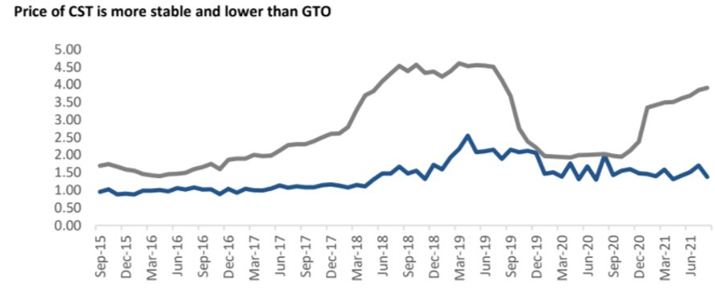

Some key advantage of CST over GTO

• Pricing: Price of CST is more stable than GTO in world market above in the picture depicts the price volatility between CST and GTO.

• Privi with a cost advantage through its backward integration as CST can be sourced much more easily and cheaply than GTO. As we know China is the largest producer of GTO in the world, so indirectly companies are dependant on supply chain with China

• As the price range of CST remains stable Privi is being able to procure higher margins and better valuations over the time.

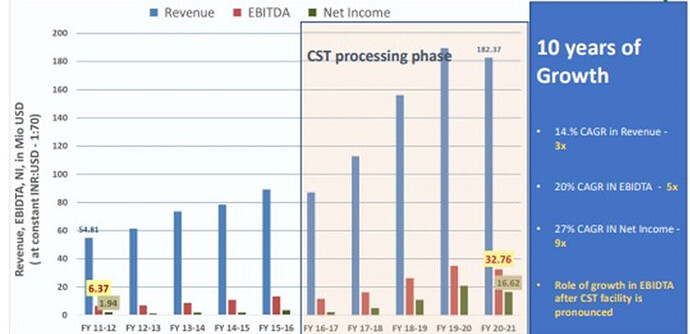

Privi is one of the few companies in the world which is able to understand the chemistry of CST and showing magnificent results out of it.

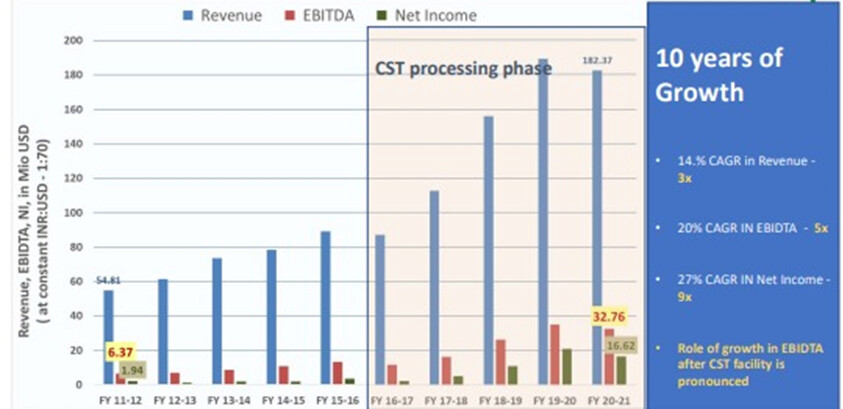

This is how adapting to CST brought in great results for the company here is the above chart showing the 10 years growth of the company.

From by-product to value added product by Privi

- Dipentene is a by-product generated through terpineol and camphene, with further processing of dipentene a product is formed called second generation herbicide which is used in agriculture purpose.

- The Dream project of PRIVI

Privi has USFDA approved plant to manufacture pharma- grade camphor. To obtain camphor, the oleoresin is harvested from the pine tree. The oleoresin is then subjected to a purification process to separate the camphor crystals from the other components of the resin. The camphor is typically further processed and refined to obtain pure camphor crystals, which can be used for various purposes. - The Bio Renewable Laevo Menthol Equivalent to natural Menthol, company have worked around 7 years into this project. The process of making l- menthol is hard to make as involves complex reactions and difficult separations. Menthol margin will be higher, minor details given by management.

Other cost effecient methods by company

• Sulphur content which is left over while going through CST process is also being extracted which is also a source of revenue for the company.

• Harmful gases are being trapped while production of aroma chemical are being used as heating of water to create steam for further production of various other chemical.

• Company has setup various filtering processor to reuse contaminated water left out during processing the same filtered water .

CUSTOMERS PF PRIVI

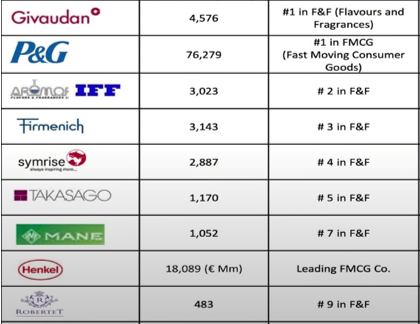

Givaudan is a global industry leader creating game changing innovations in food and beverage as well as inspiring creations in the world of scent and beauty, Givaudan operates in the expanded market space of flavour & taste, functional & nutrition ingredients, fragrance & beauty.

“We are excited with this opportunity to be partnering with Givaudan to support and expand their production of speciality fragrance ingredients. We look forward to showcase our knowhow and manufacturing expertise as a trusted partner through this strategic joint venture.” by management

Privi has signed a 5 years agreement with Givaudan in which Privi will supply 40 highly specialised molecules which will be low in volume but high in value (high margins).

The other key customer which has recently connected to Privi is RECKITT BENCKISER who is manufacturer and distributor of personal care, household, specialty products, nutrition, toiletry and health care products. The company sells its products with brand name DETTOL.

Aroma chemical companies in India will be benefited from ‘China-plus-one’ strategy and the government’s campaigns ‘Make in India’ and ‘Self-reliant India’ to boost domestic manufacturing and promote Indian products in the global markets. Global players are evaluating viable alternative manufacturing countries like India to reduce their reliance on China and diversify supply risk. Furthermore, the Indian aroma chemical industry benefits from less-stringent environmental norms as compared to China.

MANAGEMENT

Mr. Mahesh P Babani

Chairman & Managing Director

Over the past 2 decades, he has travelled extensively across the globe and has deep knowledge of the entire value chain of Aroma Chemical Business. His knowledge extends from sourcing of raw materials to their processing and to the final consumers of Aroma Chemicals. He has strong relationships across the management level of PRIVI’s customers, suppliers and other stake holders. Mr. Mahesh Babani is a Commerce Graduate and has operational and managerial experience of over 30 years.

Mr. Anurag Surana

Non-Executive, Independent Director

Mr. Anurag Surana has over 2 decades of experience in Chemical Industry is a known and reputed name in the industry and has brought immense value to the Board by providing inputs on manufacturing operations and management controls. Mr. Surana was associated with PI Industries as a Whole-time Director till September 2012. Presently, he is the Managing Director of KAGASHIN Global Network Private Limited. He is undergraduate and has completed his education from University of Delhi. He is a Director on the Board of IFFCO-MC Corp Science Pvt Ltd, Nichino India Pvt Ltd, Nichino Chemical India Pvt Ltd, Kagashin Global Network Pvt Ltd, Esco Agencies Pvt Ltd and Neogen Chemicals Limited.

Mr Anurag Surana has brought in lots of clients for the company he has worked with and for Privi as well.

Entry barrier

• There are no significant technology barriers in the space. However, established players have a critical advantage in terms of client relationships.

• Global Flavours& Fragrances houses derive most of their revenue from mature FMCG players.

• Competition among the larger players is often price based, which is the consequence of limited product differentiation.

• Companies that are able to create product differentiation would be in a position to build better margins and protect themselves. Company need to approve their products from the customer which is a big challenge for the company as it usually takes years for the products to be accepted.

RISK

- Compliance with strict pollution control norms regulations regarding water discharge.

- 70% of raw material is being imported from various other countries. Any change in import rules and duties may effect company operations.

- Side effects related to synthetic aroma chemicals may constrain industry growth . The use of synthetic fragrances can cause issues such as skin irritation and rashes due to chemical composition of various harsh chemicals which may not suit every person**.**

- The key market players are focussing on producing natural fragrances, due to the consumer preference for natural fragrances and concerns regarding synthetic fragrances due to health risks. India has become a prominent global supplier of natural fragrant raw materials such as essential oils of menthol mint, sandalwood, jasmine and spices.

- The chemical substance used in fine fragrances, cosmetics and toiletries, food and beverages provide user with distinct fragrances and experience

- The Company has high inventory days which have gotten larger due to supply disruptions recently. This means that a significant amount of the Company’s capital remains always stuck in inventory

- Mahad is a flood-prone area in Maharashtra which saw water levels rise to 25 feet in the Maharashtra flood last year. This risk from floods forms a significant threat to Privi’s operations in its Mahad plant.

competitor

The global fragrance and flavour market is largely oligopolistic with a few aroma formulators, India’s largest aroma chemicals company SH Kelkar is also a formulator. Privi Speciality Chemicals and Oriental Aromatics Ltd. are suppliers of raw materials that go into making these chemicals. Eternis Fine Chemicals Ltd. and Anthea Aromatics Pvt. are their unlisted peers.

Oriental aromatic

The company uses gum turpentine oil to manufacture aroma chemicals. In the earnings call, the company’s Chief Executive Officer Parag Satoskar said it expects capex investment to contribute 1.7 times to the top line. The management expects to renegotiate/pass on/work out prices with customers to absorb the increase in raw material costs.

Company is one of the largest manufacturers of variety of specialty based aroma chemicals, and camphor, with a vast product range including Synthetic Camphor, Terpineols, Pine Oils, Astromusk. Company started its camphor production since 1964 using technology from DUPONT of USA. Major chunk of revenue for OAL comes from camphor as we now company extracts chemical through gto process making of camphor is bit easy through this process. The company currently has a market share of nearly 33% and intends to scale up the same to 35-40%. But

The Bodani family have extensive experience in the chemical industry from last 6 decades

As per the latest commentary by the management all the plants are running at almost full capacity, which invites the need for further capacity addition to cater to the increasing demand from the customers. Thus, the management has planned a capex of approximately Rs3500-4000 million for next 3-5 years, as per Crisil report.

Eternis fine chemical (2nd competitor)

Eternis is an pvt ltd company which deals in all kind of aroma chemicals and major business is through export.

with only 12 popular formulas in the portfolio and a few specialty chemicals for specific clients, Eternis has created a strong foothold in the global market and caters to nearly 45 clients across 20 countries. Their molecules are primarily used in soaps, detergents, household products, fragrances and fine fragrances.

Mariwala believes that in India, Eternis’ primary competitor is Privi Organics(now Privi speciality) which makes 33 aroma chemicals and beats Eternis in terms of revenue, at ₹13.4 billion in FY19. One of the products that Eternis added in 2016 is coumarin, the chemical that boosted its revenue growth in FY18. An extremely popular ingredient in perfumes, coumarin smells like fresh hay and is used to support odours such as lavender and rosemary. Due to the versatility of the product, Eternis sought to expand its coumarin business and acquired the market leader in this formula — AIMS Impex last year. The deal was reportedly worth ₹500-600 million and it consolidated the company’s position in this chemical. This gave a boost to their existing capacity of 1,500 tonne. Eternis is now its only manufacturer in India.

CONCL

Privi caters their products worldwide, the most used aroma chemicals in the perfumes and scents are Dhmol and amber fleur. Privi holds 30% market share worldwide for these chemicals. Privi is one the most preferred company by 10 largest f&f players in providing aroma chemicals molecules. Recently they came into JV with the Givaudan (Swiss multinational manufacturer of flavours, fragrances and active cosmetic ingredients). Talking about the process of extracting pinene based products is through CST which is bit complex but provides competitive advantage as raw material is very cheap and they have connection with largest paper mills companies in the world to provide pulp to Privi. Coming forward company is now extending their products portfolio, recent capex in galaxmusk chemical and camphor. Privi hold USFDA approved pharma industrial grade camphene manufacturing. The camphene is hydrogenated to make isoborneol which is used in commercial manufacturing of camphor Limonene is used to manufacture citrus based aroma chemicals.

Overall, the growth in FMCG will drive the growth for the F&F industry. The demand is expected to be robust in near future Companies like HUL, PepsiCo, P&G, Coca-Cola, Colgate, The Kraft Heinz Company and other players are in constant requirement of the F&F raw materials for meeting consumer demand.

Aroma chemicals are synthetic aromas. Virtually all perfumes on the market are composed of aroma chemicals. 75-90% composition of a perfume fragrance is aroma chemicals.

DISC- The report constitutes facts and is being collected through reliable sources. Report is made only for Educational purpose and does not constitute any kind of Buy/Sell recommendation.

Krishca Ltd : A SME offering steel strapping Solution (19-08-2023)

Hi,

Couple of questions:

- What is the HS code for their products?

- how long is ADD applicable on imports from china?

Thanks

Tilaknagar Industries- Potential Turnaround Candidate (19-08-2023)

Tilaknagar industries first ever concall Q1FY24 notes :-

-

After whiskey , brandy is the 2nd largest category in IMFL . Brandy has 20% IMFL volume share .

-

Past super growth came from leverage , now growth with deleveraging the company.

-

90% of the company’s volumes come from brandy .

-

Flagship brandy mansion house brandy largest selling brandy in india . 40% + growth in flagship brands mansion house , korean napoleon brandy .

-

Only company in asia to try flavoured brandy mixes

-

Working on innovations towards premium brandy .

-

Relaunch of blue lagoon brand ( entry level gin)

-

80% volume of brandy for the company comes from prestige and above segment

-

Continuous increase of market share .

-

Net per case realisation Rs 1250 vs Rs 1157 (YoY)

-

Company majorly operates in the southern region with 85% contribution of overall volumes of the co.

-

Near full capacity utilisation at 2 of their units.

-

100 KLpd greenfield project

-

Exploring newer geographies such as eastern and north eastern ( seeing good tractions from sikkim region)

-

Q1 YoY Volume growth 42% ( exceptional growth due to last year’s lower base )

-

Overall the IMFL industry growing at 12% ( according to management).

-

Margins dependent on state and brand mix .

-

Medium to long term will explore outside brandy .

-

Gross debt reduced from 1200 crs ( peak ) Vs 239 crs ( June 2023)

-

Refinancing cost at 13%

-

Interest cost at 6 cr vs 13.4 crs (YoY)

Going forward

- Margins shall be in the range of 13-14% ( As volumes increases company operating leverage shall kick which can possibly lead to margins expansion

- For FY24 , Volumes growth to be in mid teens and on longer term towards low double digits to mid teens .

- Addressable market growing at low double digits.

- 100 KLpd greenfield project , (will cost above 50 crs and below 100 crs)

- From next FY onwards normal capex of 25 crs.

- No leveraged expansion going forward.

- Goal is to become net debt free in 5-6 quarters .

- No taxes for FY24 ( 160 cr accumulated tax losses in the book). From FY25 taxes shall be applicable .

- Marketing spends shall increase as business has moved from consolidation to growth phase .

IRB INVIT TRUST- new game in the town! (19-08-2023)

Did anyone attend 7th August Concall?

Please share the salient points or any link as I am unable to find same on you tube this time.

Aptus Value Housing : Is valuation justified or just another HFC? (19-08-2023)

Hello to all

Did anyone attend the AGM held on the 18th of August, 2023 if yes please share the questions and answers.

Thanks

Kovai Medical Center and Hospital – Health and Wealth (19-08-2023)

To add on my 2 cents :

- What’s the plan to expand medical college from current 150 to 250 seats ? We know, this would be long term but that’s when operating leverage shall kick in

- What’s the succession planning of top leadership ?

Salzer Electronics (19-08-2023)

AR 23 is a good read – Switchgear etc are seeing healthy demand and grew 40%+ incldg exports, higher probability case of 20%+ topline and much higher Ebdita growth(improving product mix + RM stability + better realization ) – overall a good proxy for electrical infra theme with good growth + some rerating possibilities,

-

New products (much higher margins) seeing good traction in exports with spike in export for 3 phase dry transformer and DP contactors volumes, should aid product mix improvement.

-

Industry & tailwinds – some tailwinds working in favor ofIndian players in expports particularly , CG Power in their concall has indiacted very high demand for switchgears and supply constraints giving visibility for future, to an extent that they are not able to fulfil given very large OB /enquiries. A possible tailwind here

-

switchgear projections indicate rapid expansion i

Price action Taken out ATH on charts and likely to do well from here

EV chargers – Mgmt calls EV chargers JV as high optionality case FY 25 onwards but need to be seen as project has seen some delays, though some good discussion in Q1 concall here on status updates and higher focus on fast chargers (not a crowded space like regular chargers) – space as a whole should see exponential growth in coming times. Their JV with EU player makes it less denting on capital reqmt.

- Promoter also indicated raising holding in one of recent interviews – more connected to mkt perception than performance itself, if and when it happens will help further

D – invested

Campus Activewear – betting on the India Consumption Theme (19-08-2023)

Campus Q1FY24 Earning updates

Weak quarter from campus. Revenue of 353.8Cr, 4.8% growth YoY.

Trade distribution down by 5.5%, D2C online up by 10% and D2C offline up by 82%.

EBITDA and PAT margin stable at 18.8% and 8.9% respectively.

Witnessing green shoots of recovery in eastern UP and parts Bihar, Expect full blown recovery by festive season.

Comments from Earning call:

Nikhil Agarwal emphasizes their brand’s unique selling point (USP) of introducing the latest global fashion trends and designs to India promptly and affordably. They maintain a vast portfolio of 600 designs, including 300 new ones annually, highlighting their commitment to offering fashionable and technologically advanced products ahead of competitors.

Improved gross margin is attributed to favorable changes in channel and product mix, along with sourcing efficiencies. The sustainability of this margin improvement is linked to the company’s consistent growth trajectory, and there is potential to improve it further.

growth in D2C offline driven by franchise stores. Out of 255 stores 90-95 are company run stores rest franchise. Strategy to have 70:30 split in favor of franchise.

Nikhil anticipates a positive impact on domestic growth through the implementation of the BIS regulations starting January 2024. By focusing on premiumization within the price range of Rs. 1,000 to 3,000, the company aims to capitalize on the BIS-driven reduction of imports from China, Vietnam, and Indonesia, ensuring not only improved margins but also a rise in average selling prices (ASP) within the optimal price range.

The company’s historical growth trajectory, with a 3-year and 5-year CAGR of around 24% to 27%, has been maintained even in recent times. While some shifts in margin profiles have occurred, their priority in a slowdown scenario remains focused on pursuing growth aggressively while maintaining a respectable margin profile, as margins can be regained in stable macro conditions. Gaining market share and shelf space is emphasized as a crucial strategy, considering its lasting impact compared to recoverable margins, making slowdown periods seen as opportunities to excel.