Edelweiss has took so much time for demerger at every stage.

Nuvama Wealth demerger happened = early Jun 2023. Listing date is 23 Aug 2023

JIO Fin Services demerger happened = Mid july 2023. Listing date is 21 Aug 2023

Clearly shows difference.

Edelweiss has took so much time for demerger at every stage.

Nuvama Wealth demerger happened = early Jun 2023. Listing date is 23 Aug 2023

JIO Fin Services demerger happened = Mid july 2023. Listing date is 21 Aug 2023

Clearly shows difference.

Results are on the expected lines, and the stock performance since last month has shown it all.

Meanwhile going along the line, another launch today.

Looks like the management has got hold of this new strategy, hopefully, it reflects in bottomline.

I believe that it did make the result look more better off(imagine if they had added the loss to PnL; then would be significantly lower), but would wait for next quarterly result’s Other income section

REL has been on flat margins for years. No con-calls. Quite mysterious company however it’s the largest gold refinery in the world.

Request you to please give your inputs.

Can you throw some light on the holding period for the stocks, the approach towards profit booking, the kind of stop losses implemented?

And have you automated this, or there is an element of manual intervention?

The ILD relationship of VIL is moving from Tanla to Route Mobile.

Route press note – https://www.bseindia.com/xml-data/corpfiling/AttachLive/7275acd4-7d6b-48a1-885f-c1348ad44e88.pdf

Tanla press note acknowledging impact – https://www.bseindia.com/xml-data/corpfiling/AttachLive/c3e0fbae-6eb8-4a15-8729-a486b31e74a5.pdf

FY24 impact will be restricted to 4 months it looks. 4 month impact would be 23Cr topline and 12Cr bottomline. Full year impact in FY25 should be 68Cr topline and 36Cr bottomline. Very impressed with the disclosure and clarity provided. Uncharacteristic.

The conference call transcript for Q1FY24 is out, I will summarize it:

Pipes & Tubes:

In Q1FY24, lower steel prices and economic headwinds led to flat growth yoy. But, due to a better product mix and value-added products, we got better margins. Q4FY23 was a one-off exceptional on realizations and we should not compare with that.

Volume grew 20%, with domestic +27% and Export +6%. Due to the cyclone, lost 15 days of production. API Export which is a high-margin product got impacted and dispatch was slow. Expect Q2FY24 to be better and H2FY24 even better as major projects pick-up post monsoon.

For DFT Plant we will do 30k MT for FY24 but only with 2k EBITDA/MT. We are finding the right buyers as this is a large-size product and stocking is not possible. Once, we set the tone, EBITDA will improve significantly.

Overall Utilization levels are 72% for this quarter. On average for a year, the utilization levels are 78-80%.

OB is currently at 500Cr deliverable in 1-2 months. Got steady inflow in CGD, O&G, and API Pipe Business.

Approved CAPEX of 45cr. 40Cr for CR Steel to improve surface finish quality and 5Cr for PVC Pipes. Anjar and Hindupur’s CAPEX are ongoing. With these CAPEX, volume guidance remains at 12%. We will remain at EBITDA/MT of 6500 levels (near to FY23 figure) or slightly more.

Lighting & Consumer Durable:

Favourable environment led to higher growth. 27% growth in professional lights and it will grow further due to good CAPEX cycle,

EBITDA margin at 8% for Light where earlier it was 6.4%. This improvement is due to backward integration from the PLI scheme, better product mix, and premiumization. We expect margins to improve further.

Introduced a few more products in the appliances category. Plan to add 5 new products a month i.e. 60 new products a year. We launched a few new products in anticipation of a good upcoming festival season.

Advertisement spend – plan to double in FY24. On an annual basis 20% growth in light business with better margin. Also, efforts are being done to strengthen interactions with dealers & distributors, and electricians through a series of campaigns. We have taken abroad about 400 dealers/distributors for a big launch program.

Others:

Reduced debt by 170 Cr. And intend to be debt free by next FY. There is 230 cr. Of debt but all WC only, no long-term debt. All CAPEX will be done with internal accrual going ahead.

Committee is made already for de-merger. They have completed their de-merger work also. But the board has not taken up the agenda yet. Instead, they took up a split and approved from FV of 10 to FV of 5. So, it is on board.

We did ROCE of 15.8% v/s 8.2% yoy as on Q1, ROE improved to 12.5% from 5.7%. All this is due to a better product mix i.e. premium and high-margin products.

My View:

The results are decent. Volume growth was visible in both Pipes & Tubes +20% and Light business +12%. Also, Q2 will be better and H2 will be even better as per the management. The guidance of 12% volume growth in Pipes & Tubes along with 20% growth in the lights business for FY24 is also pretty decent.

If you are waiting for the de-merger to encore value you might well remain invested as there is nothing wrong with this company that will affect the value in the medium-term. I remain invested given the fact that relative valuations are cheap i.e. 11x TTM PE v/s other pure-play steel pipes companies like Ratnamani (32x), APL Apollo (60x), etc. Yes, the business specifics are different but the gap in valuation is too huge which definitely gives a margin of safety and additional benefits of surprises going ahead.

Disclosure: Invested.

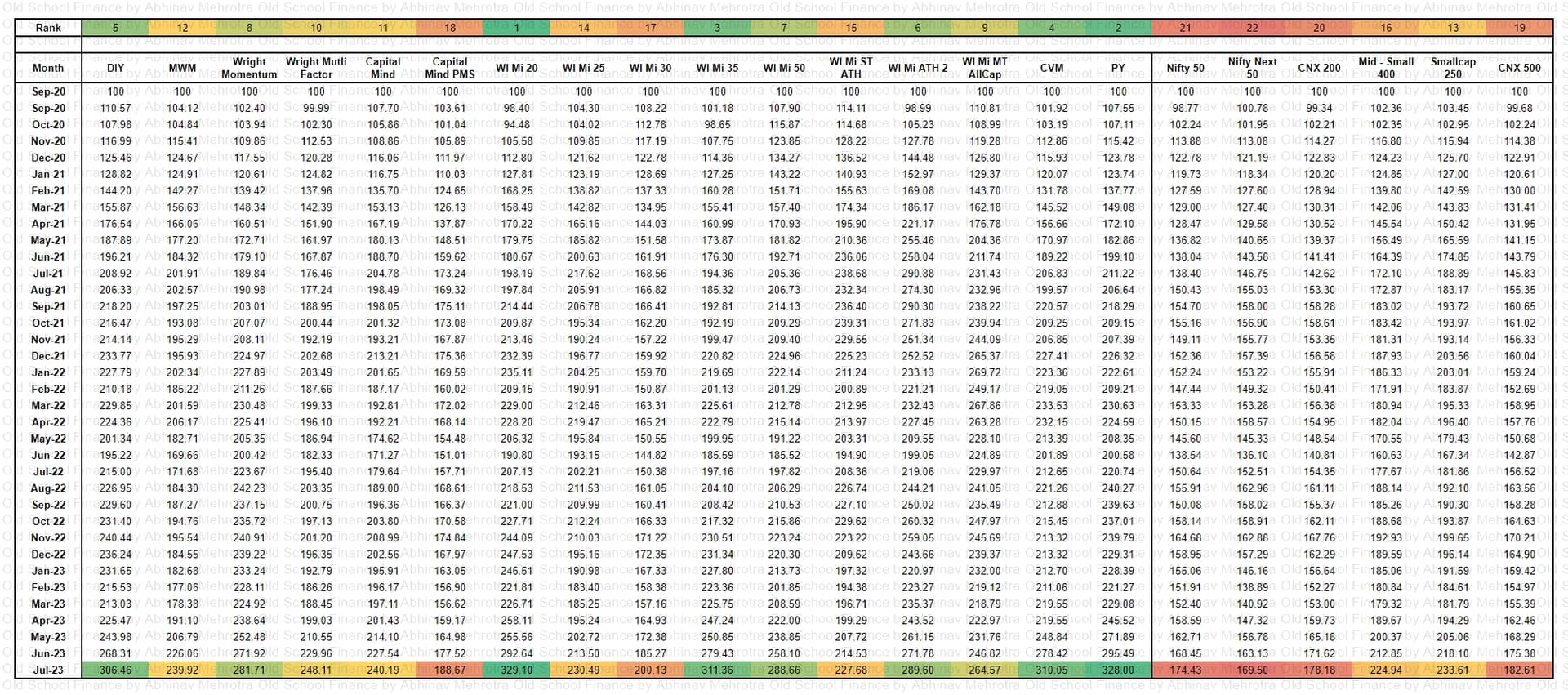

Since momentum is a well-known product I have benchmarked my performance to other smallcases as well.

Usually the correlation is lowest between value and momentum. So it makes sense to run a barbell or satellite-core framework in portfolio of these two.

Value+growth+quality can be discretionary and momentum can be systematic non-discretionary.

Mixing the factors doesn’t always have the best results. They are best run separately.

For diversification in portfolio asset allocation is a better diversifier than factor diversification.

You will find the fama-french library of factors date tailored to India here: Invespar

There is another resource called qfinr where you can input your PF returns, or your MFs and see which factor you have been historically been exposed to.

I have shared how to build a momentum screener here. If you have any more queries do ask. I have also shared a repository of research papers on factors in the blog post.

For books you may want to read,

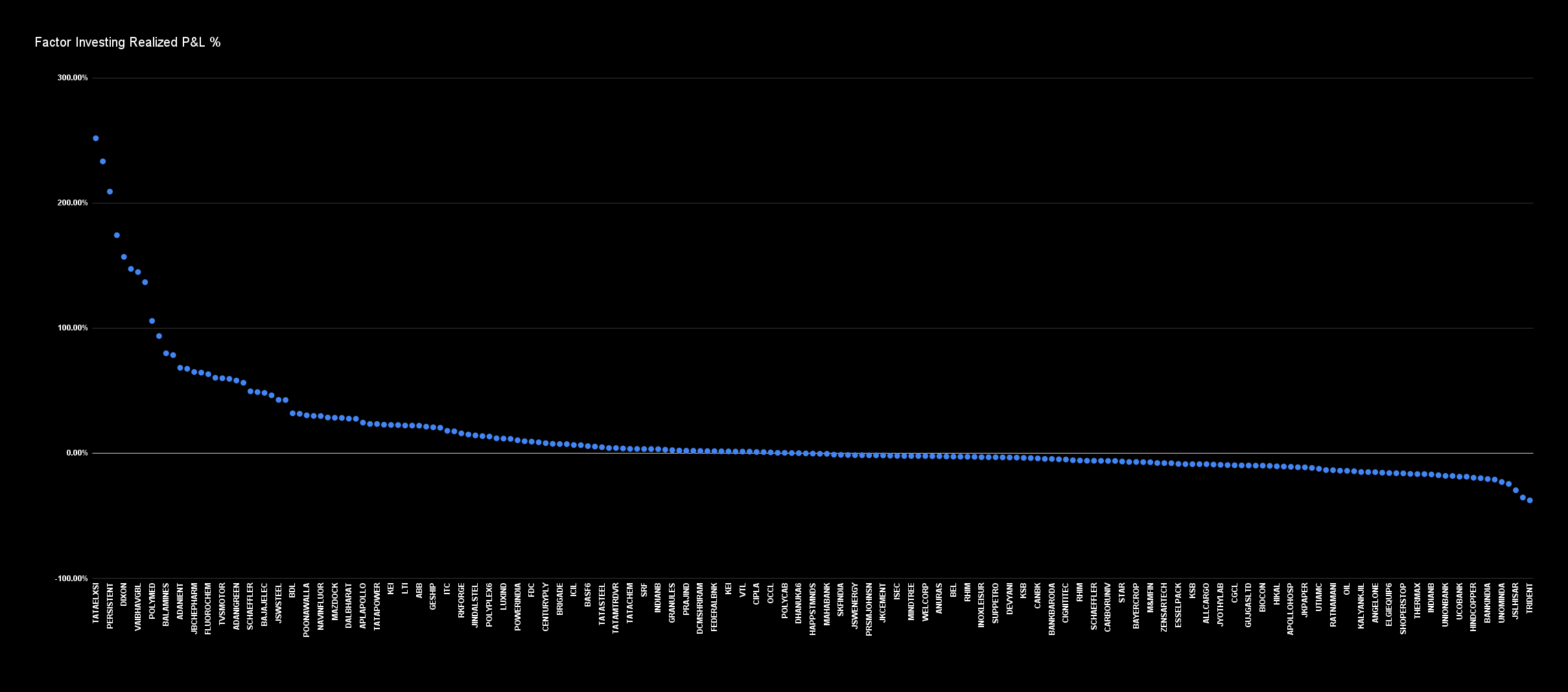

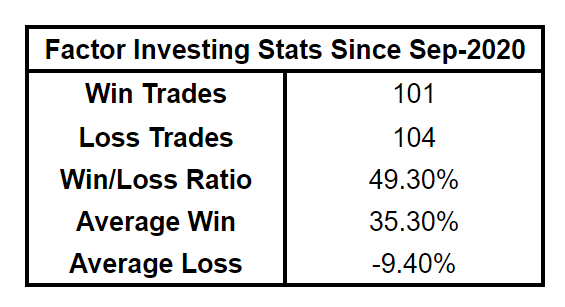

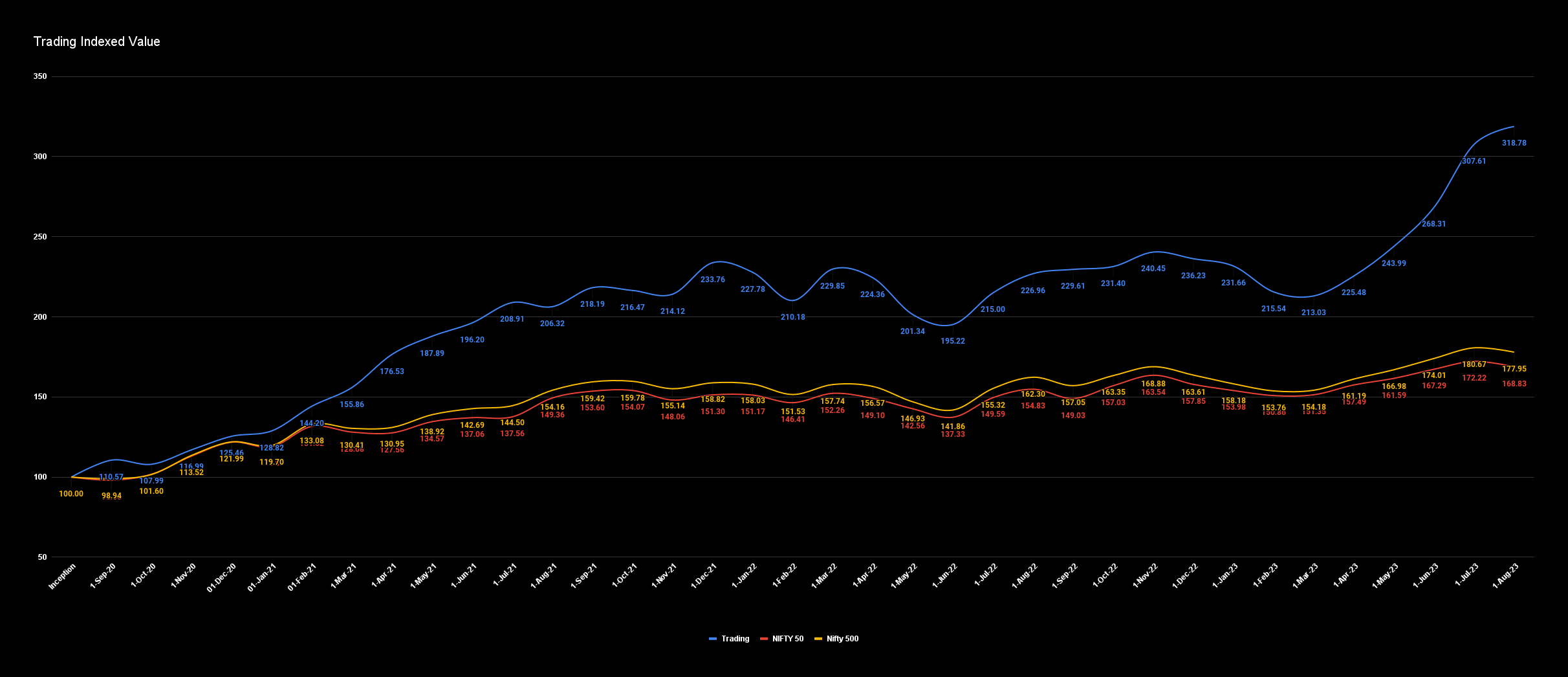

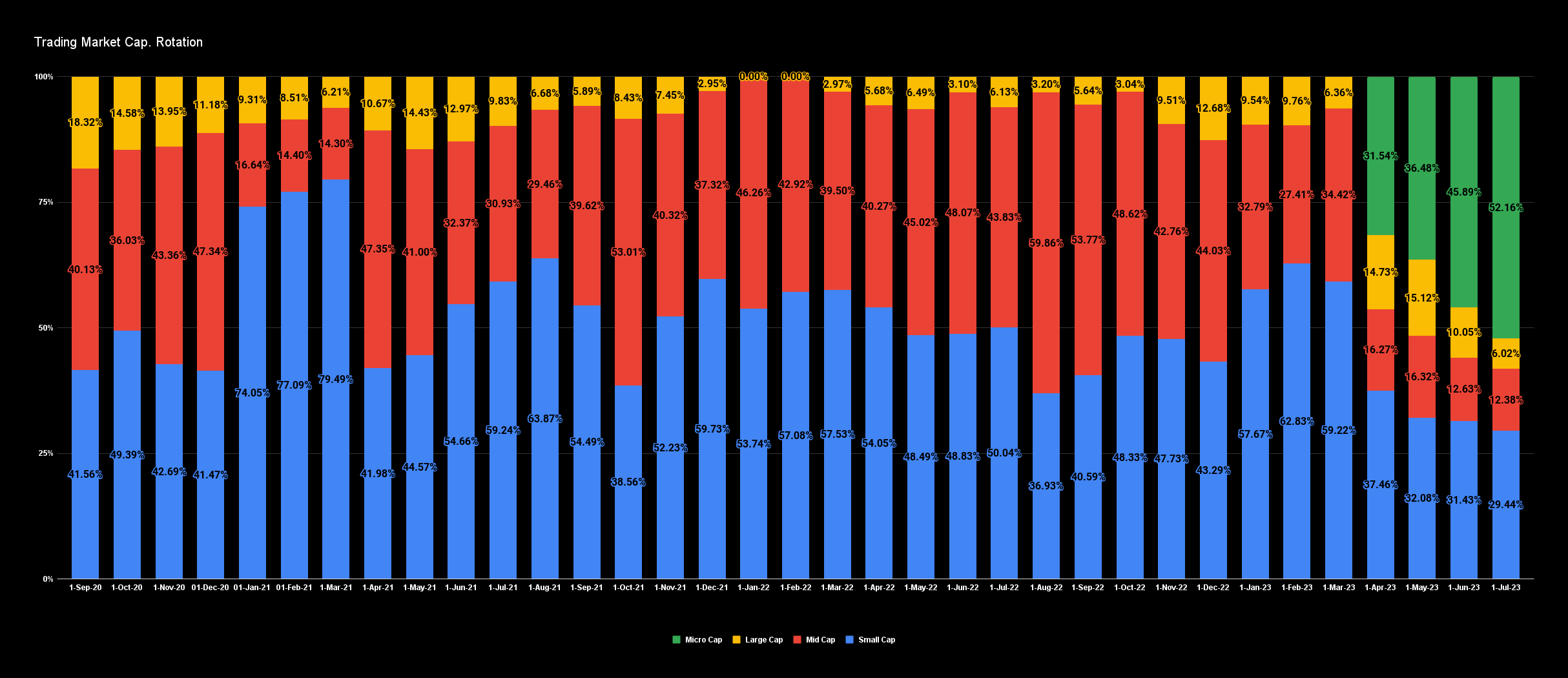

Below are some stats of the strategy I have been running.