Inflame is one of the supplier

Posts in category Value Pickr

Hind oil exploration is this a multibagger bet? (16-08-2023)

I also believe that the selling could have been by HDFC. As far as I know by regulation HDFC can’t hold any shares of another company post the merger. In the last quarter HDFC sold some shares which may have intensified in this quarter.

Hind oil exploration is this a multibagger bet? (16-08-2023)

I also believe that the selling could have been by HDFC. As far as I know by regulation HDFC can’t hold any shares of another company post the merger. In the last quarter HDFC sold some shares which may have intensified in this quarter.

Man Industries (India) Limited (16-08-2023)

Summary of the Q1 FY24 earnings call Man Industries (India) Ltd:

Strengths:

- Diverse Product Portfolio: With products like LSAW, HSAW pipes, and the addition of ERW, the company has a diverse range of offerings catering to various sectors.

- Certifications and Compliance: The ERW plant’s recent certifications (BIS and upcoming API) demonstrate a commitment to quality and adherence to industry standards.

- Strong Order Book: With an unexecuted order book of around 1900 crores and bids for more than 13,000 crores, the company has a robust pipeline of business.

- Improved Financial Performance: The growth in EBITDA and net profit, along with improved margins, indicates financial strength.

- Strategic Expansion Plans: The company’s plans for expansion and diversification into new areas like ERW and stainless steel show a forward-thinking approach.

Weaknesses:

- Operational Challenges: The impact of natural disasters like cyclones and heavy rains has shown vulnerability in operations, leading to production losses and delays.

- Dependence on Certain Markets: If the company relies heavily on specific sectors like oil and gas, changes in those industries could affect its performance.

- Capacity Utilization: The current capacity utilization of 60-70% in certain segments may indicate underutilization of resources.

Opportunities:

- Growing Infrastructure Needs: With increasing demand for infrastructure development in India and abroad, there are opportunities for growth in the pipe manufacturing sector.

- New Product Lines: The introduction of ERW and stainless steel products opens new markets and customer segments.

- Strategic Acquisitions or Partnerships: Collaborating or merging with other players in the industry could enhance the company’s market reach and capabilities.

- Sustainability Initiatives: Emphasizing environmentally friendly practices and products could align with global sustainability trends and attract eco-conscious customers.

Threats:

- Market Competition: The industry is competitive, and new entrants or aggressive strategies by existing competitors could challenge the company’s market position.

- Global Economic Fluctuations: Changes in global economic conditions, particularly in the oil and gas sector, could affect demand for the company’s products.

- Regulatory Changes: Any significant changes in regulations or standards could impact the company’s operations and compliance requirements.

- Supply Chain Disruptions: Global events like pandemics or geopolitical tensions could disrupt the supply chain, affecting production and delivery timelines.

Management Guidance:

- Financial Guidance:

- Revenue guidance for the year ending FY24 is around 3000 crores.

- For FY24-25, with the addition of ERW and other new products, the estimated revenues are between 3500 to 4000 crores.

- Operational Guidance:

- The unexecuted order book stands at approximately 1900 crores, expected to be executed in the next six months.

- The ERW plant has received BIS certification and is awaiting API certification, which will strengthen the company’s position in the market.

- The company is actively participating in tendering processes and expects good order book inflow in the near future.

- Expansion Plans:

- The management has plans for further expansion, including the introduction of new products like ERW and stainless steel.

- Proceeds from land sales may be used for debt repayment or further expansion.

Disc: Invested

Steelcast Ltd – leading steel castings (16-08-2023)

From the earnings call transcript for Steelcast Limited’s Q1 FY24, here’s a detailed summary-

Strengths:

-

Diversified Customer Base: Steelcast has expanded its customer base, adding two more customers during the quarter. They have also diversified their order book across various industries, including Mining, Earth Moving, Locomotives, Transport, Construction, Railways, Ground engaging tools, Cement, Steel, and Defense.

- Example: The company has entered into a long-term supply agreement with a prominent OEM in the USA specializing in the railroad industry.

-

Strong Financial Performance: The company achieved a revenue of Rs. 119.5 crores, a YoY increase of 3.3%. EBITDA reached Rs. 32.3 crores, a 34% YoY increase, with an EBITDA margin of 27%. PAT expanded by 43.4% YoY to reach Rs. 20 crores.

- Stats: EBITDA margin of 27%, PAT margin of 17%.

-

Cost Advantage: Steelcast continues to have a cost advantage, being 20%-25% cheaper than European peers.

- Example: Despite global gas price fluctuations, Steelcast’s cost advantage remains consistent.

Weaknesses:

- Moderate Revenue Growth: Despite strong financial metrics, the company reported only a 3.3% YoY revenue growth.

-

Dependence on Global Conditions: The company’s performance is influenced by global geopolitical conditions, which can lead to unpredictability.

- Example: The management mentioned potential softness in demand during Q2 and Q3.

Opportunities:

-

Strategic Investments in New Sectors: Steelcast is focusing on newer industries such as defense, railways, and ground engaging tools.

- Example: The company has been making track systems for combat vehicles and received approval for a repeat order of 5 more track systems to be delivered by March 24.

-

Cost Savings through Power Plants: The company has commissioned a 5 MW Solar Power Plant and a Hybrid Power Plant, which are projected to yield annual power cost savings in the range of Rs. 10 crores to Rs. 11 crores.

- Stats: Expected annual savings of Rs. 10-11 crores from power plants.

Threats:

-

Global Uncertainties: Geopolitical situations and global economic uncertainties could impact the company’s performance.

- Example: The management acknowledged the ongoing global uncertainties and the need to work through them.

-

Competition: The company operates in a competitive industry, and aggressive pricing strategies by competitors could pressure margins.

- Example: The management mentioned that trying to increase margins beyond the current levels might invite competition.

-

Dependence on Specific Markets: The company’s performance in specific sectors, such as defense and railways, could be influenced by changes in those markets.

- Example: The company’s growth in the defense sector is moving at a slower pace, and the North American railroad industry is progressing as planned.

Comparison with Previous Quarters/YoY Growth:

- Revenue: Achieved a revenue of Rs. 119.5 crores, reflecting a YoY increase of 3.3%.

- EBITDA: Saw substantial growth, reaching Rs. 32.3 crores, a 34% YoY increase.

- PAT: Expanded by 43.4% YoY to reach Rs. 20 crores.

The management’s tone during earnings call was characterized by confidence in their financial achievements, transparency about global challenges, and a cautious approach to future growth. Investors, on the other hand, displayed an inquisitive attitude, probing into key areas of the company’s performance and future prospects.

Steelcast Ltd appears to be in a strong financial position with clear strengths in cost efficiency and debt management, but it also faces challenges from global uncertainties and competition.

Disc: Invested.

Hindware Home Innovation Ltd on to rapid growth post demerger? (16-08-2023)

Do you know who manufactures these Chimneys or whether Hindware does it in-house? I think Inflame Appliance in one of their con-call or interview (can’t remember where) had mentioned that Hindware is one of their customer for Chimneys (Glen is too btw)

Deepak Fertilizers and Petrochemicals (16-08-2023)

lol what? what’s even the point of such humongous backward integration then? Could do a smaller capex to narrow the range than to fully eliminate it

PNGS Gargi Fashion Jewellery Limited (16-08-2023)

Thanks for this thread. Some further insights/notes:-

-

They’re doing pretty great in terms of website design. I noticed features like “Shop The Look” which are high end and you see them on websites like Svarovski or Monica Vinader

-

Instagram page of Gargi is a nice mix of catalogue + local influencer videos and it has decent traction given the size of the Company. Maybe they could improve upon responding to customer comment section or introducing CTAs like Insta Shop

-

Their cataloging strategy is excellent with some high def photos (and not CGIs) of model adorning the particular SKU.

-

Their products unfortunately have no reviews / ratings either on Amazon or their own website. On Amazon, I also noticed that if you search for PNGS Gargi, it shows you some other competitor results on sponsored tag. They might need to fix this.

-

They have lower SKUs as compared to Giva or even lesser known brands such as Voylla.

-

Competitive intensity is significant in this category. Premji invest backed Giva, Nykaa backed Pipa + Bella.

-

I find Aditya Modak to be a very humble – undithered by what competition is doing – sort of a guy. In an interview he talked of how startups are focussed on cust. acquisition but not on retention. Talked of omnichannel advertisement when they open SIS in MBOs such as Shoppers Stop etc. I got the sense that he knows what he’s doing.

I don’t expect fireworks here since they’re not spending huge on advertising, yet at the same time, they’re doing a lot of the things right that even top consulting firms have advised to much bigger Nifty 50 brands ![]() So I see some foresight, pursuit of excellence here.

So I see some foresight, pursuit of excellence here.

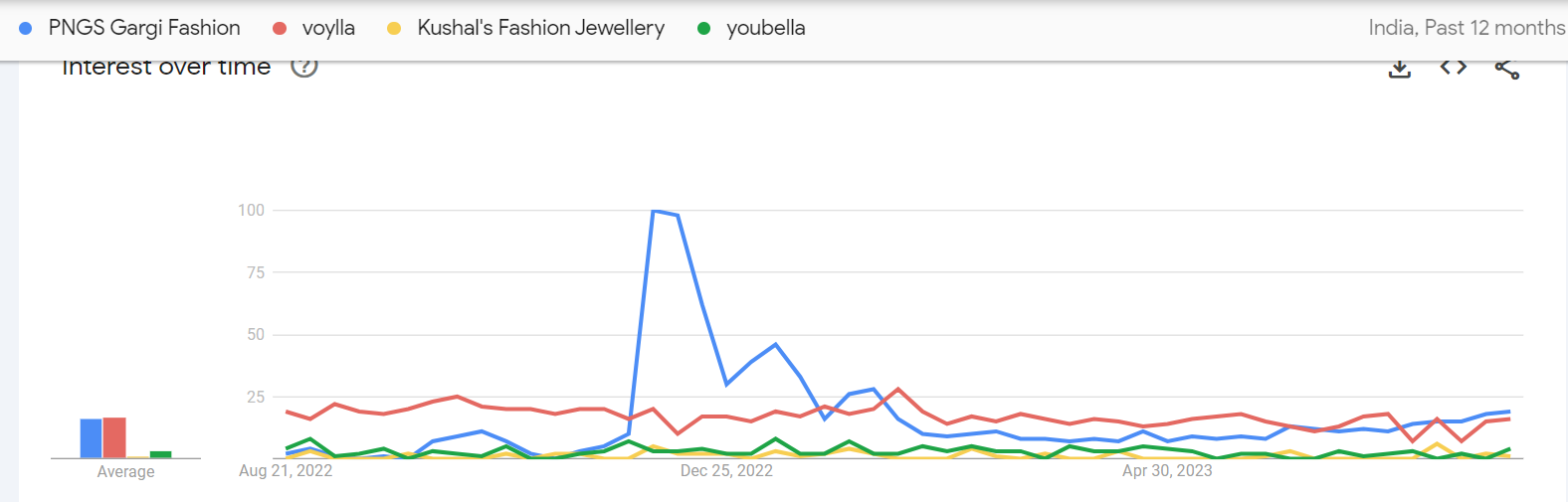

Google trend analysis shows that Gargi clearly saw a lot of interest from the investor community (spike around IPO time) which fizzled out… but if you see the past few months, the trendline is rising again

PNGS Gargi Fashion Jewellery Limited (16-08-2023)

Thanks for this thread. Some further insights/notes:-

-

They’re doing pretty great in terms of website design. I noticed features like “Shop The Look” which are high end and you see them on websites like Svarovski or Monica Vinader

-

Instagram page of Gargi is a nice mix of catalogue + local influencer videos and it has decent traction given the size of the Company. Maybe they could improve upon responding to customer comment section or introducing CTAs like Insta Shop

-

Their cataloging strategy is excellent with some high def photos (and not CGIs) of model adorning the particular SKU.

-

Their products unfortunately have no reviews / ratings either on Amazon or their own website. On Amazon, I also noticed that if you search for PNGS Gargi, it shows you some other competitor results on sponsored tag. They might need to fix this.

-

They have lower SKUs as compared to Giva or even lesser known brands such as Voylla.

-

Competitive intensity is significant in this category. Premji invest backed Giva, Nykaa backed Pipa + Bella.

-

I find Aditya Modak to be a very humble – undithered by what competition is doing – sort of a guy. In an interview he talked of how startups are focussed on cust. acquisition but not on retention. Talked of omnichannel advertisement when they open SIS in MBOs such as Shoppers Stop etc. I got the sense that he knows what he’s doing.

I don’t expect fireworks here since they’re not spending huge on advertising, yet at the same time, they’re doing a lot of the things right that even top consulting firms have advised to much bigger Nifty 50 brands ![]() So I see some foresight, pursuit of excellence here.

So I see some foresight, pursuit of excellence here.

Google trend analysis shows that Gargi clearly saw a lot of interest from the investor community (spike around IPO time) which fizzled out… but if you see the past few months, the trendline is rising again