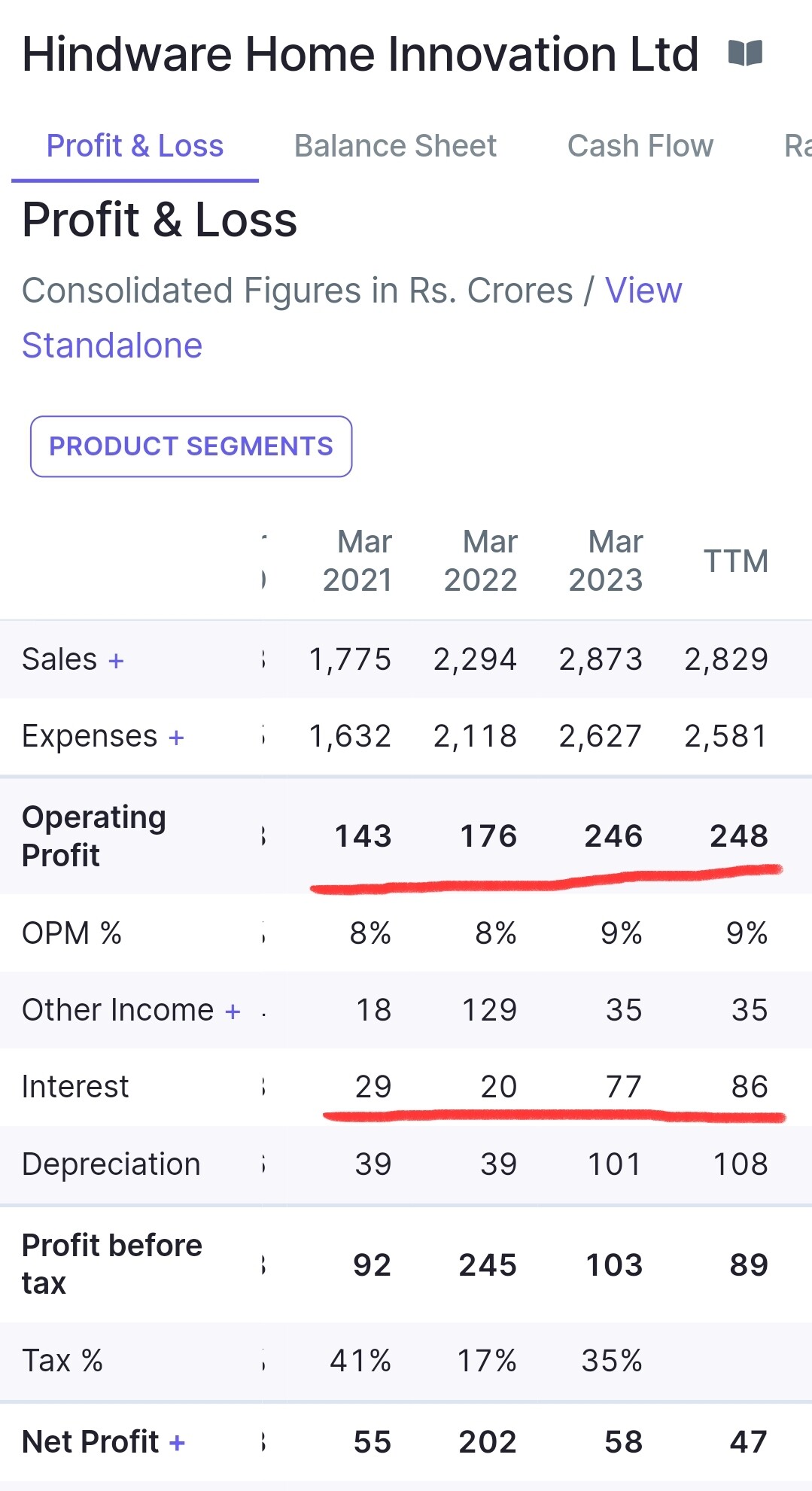

If we study P and L of last 3yrs, thers is good growth of operating profit.

However, net profit is largely affected by interest.

Disc…invested

If we study P and L of last 3yrs, thers is good growth of operating profit.

However, net profit is largely affected by interest.

Disc…invested

Q2- 2023-Investor presentation

1…Inflationary concerns and rising interest rate have slightly

impacted the demand for mid and lower priced offerings

2…Integrated marketing spearheaded by vibrant IPL campaign

further boosted brand recognition and appeal

3…Expanded our reach in the Indian tiles market, with plans to expand the

network further

4…Marketing Initiatives

Hindware partnered with two IPL teams Royal Challengers Bangalore & Punjab Kings for this IPL season

Launched “5 star Hotel like Bathroom” campaign featuring players from RCB & Punjab Kings

360 degree campaign was launched on TV, OTT, Digital, Radio & BTL activations

179M impressions were served during the campaign with a reach of 45M

The website traffic during the IPL season was twice the normal traffic

5…TRUFLOW

= We continue our momentum towards achieving higher market share despite slight headwinds in

Q1 on account of lower demand and reduced input prices

Diversified into PTMT Faucets and Accessories to offer comprehensive plumbing solutions for

customers’ needs

Exclusive collaboration up with RWC Reliance Worldwide Corporation to launch Truflo Sharkbite,

a range of innovative multilayer composite pipes and fittings

Establishing a new manufacturing facility in Roorkee, Uttarakhand, and construction of the facility

is underway

TRUFLO by Hindware, is the fastest growing plastic pipes and fittings

brand in India

o With 2000+ SKUs already being offered and many more being

added, TRUFLO aims to be amongst the top 5 CPVC players in

3 years

In-house manufacturing for better efficiencies & end to end logistics

and supply chain control

The Company offers CPVC pipes for hot and cold-water plumbing

applications, along with lead-free UPVC pipes, SWR pipes, PVC pipes

for potable water, column pipes and overhead water storage tanks

6…Successful launch of the Hintastica Private Limited (JV) line of heating

appliances at its state-of-the-art manufacturing facility in Jadcherla, Telangana,

is delivering as per expectations

Disc…invested

Agree that Deepak Nitrate results was bad. But then after it has become 6 bagger for you, you must have developed that extra cushion where you are comfortable with 2-3 bad quarters…So i am curious why you sold a company which is good and has given you terrific returns just for one quarter bad result. I think greay companies too have many quarters and sometimes few years as bad.

Interesting observations about Dividend Investing.

Investing in “Dividend Yield” funds will also have some other points:

(1) Though an investor will save Dividend Tax and that will help growth in NAV, if you need regular passive income, then you need to have SWP or profit booking and then pay the tax on Capital Gains. But still it will be less than nominal tax rate.

The drawback is that, the NAV may fall by 20%-30% routinely due to market volatility, and your passive income will get impacted.

If you are not investing for regular passive income, then it looks fine.

(2) For those investors looking for regular passive income, paying tax on Dividend Income should be all right. Anyway, you are paying income tax on your other regular incomes from FD, Salaries, and other sources of income which might be dependent on your tax bracket.

I think, it is more to do with the individual requirements of regular passive income and personal choices.

Going by the numbers delivered and commentary, appears that demand has resumed after two quarters of softness (in line with managment commentary last quarter).

Overall, 10% Y-o-Y and 76% Q-o-Q revenue growth. EPS has been flat Y-o-Y at~12 Rs., mostly attributed to inventory losses in this quarter and higher other expanse (management indicating about higher R&D investments – now and going ahead).

Some notes from GTBL investor presentation for Q1FY24 (link):

The current quarter witnessed normalization of the tendering process leading to strong growth on sequential basis with the topline growing by 76% quarter-on-quarter. The demand for the current products (Rifa S and Rifa O) remains strong.

New API block is expected to be commissioned by October 2023, which is an essential part of our strategy of moving up the value chain. This would increase the product portfolio of the Company.

The first phase of the new R&D center and cGMP pilot facility is also expected to be commissioned by December 2023

The R&D expense is likely to remain elevated for few more quarters.

For full year FY’23, PP&E change from 18 Crs. to 32 Crs. CWIP increased from 12Crs to 21 Crs.

Open to both Organic and Inorganic opportunities for growth in Specialty Chemical space

Some notes from recent released credit rating report (Care rating):

An increase in the quantity sold (198,313 kg in FY23 from 174,689 kg in FY22) with an increased demand of the products in FY23.

[ this despite soft demand situation in Q3 and Q4 for FY’23]

Sales realisation improved to ₹7,469 per kg sold in FY23 compared to ₹6,537 per kg sold in FY22

[this too despite soft demand situation in Q3 and Q4 for FY’23!! ]

PAT margin improved marginally to 38.91% in FY23 vis-à-vis 37.98% in FY22 on account of a decline in interest expenses.

GTBL’s operations remained working capital-intensive and the cycle elongated to 67 days in FY23 vis-à-vis 56 days in FY22, mainly on account of funds stuck in inventory and debtors

Thanks,

Tarun

Disc: Invested, no transaction in last 60 days

Results for all my portfolio stocks are out. Winners are Polycab, APL Apollo, PI industries, Ethos and Varun Beverages. Whereas Deepak Nitrite and Granules India reported terrible results. As a result I sold Deepak Nitrite with 6X gain after holding it for almost 4 yrs. I have also sold CarTrade at a 45% loss.

Meanwhile I keep on investing the proceeding in Zomato (after their first profitable quarter), CCL Products (ideal compounder), Bajaj Finance (no idea why it’s not performing, anyways I keep on buying:)), Mold-Tek packaging (typical 18-20% grower) and Vaibhav Global (my thesis is that as money is more valuable due to inflation in western economies so buyers will look for value for each dollar and here low cost producer like VGL will have upper hand). Overall I have now 24 stocks in my India portfolio with 8 multibaggers as of now.

Since the last update Polycab became 3.5X to 5X, PI industries became 5X to 6X, VGL became 3X to 4X. If everything goes well then I expect Ethos (up 57%), APL Apollo (up 70%) and Mas Financial (up 58%) to be new multibaggers (my definition of multibaggers is 2X in 3 years of initial buying) in my portfolio. Fingers crossed:)

In the India portfolio, I am experiencing NVIDIA-like euphoric gains in Polycab and other building material stocks post their result announcement. Magnitude of the earning beat for Polycab is similar to the earning beat of NVIDIA in last quarter. This is interesting. The US being a developed economy generates demand for AI chips (Pick and Shovel play in AI war) to increase productivity and hence GDP… Whereas India being an emerging economy needs more roads , constructions, infrastructures and hence generates similar demand in the building material sector (Again Picks and Shovels play in the construction segment) to make progress in its GDP. IMO, unlike the US, in India I am not trying to look for next AI winners to make money in the long term, real money is being made in the building material segment as these two economies are standing in different junctures and as a result showing Animal Spirits in completely different segments.

Portfolio 5 yrs return 19.1%

Portfolio 3 yrs return 29.7%

Portfolio 1 yr return 12.1%

Disc. This is not a buy/sell recommendation. Biased as invested in all stocks discussed above. Not a SEBI registered advisor.