From my understanding, BoP is a business strategy, which states a companies strategy to make profits by catering to those who are in the bottom of the pyramid, in Caplin’s case it would be providing low cost medications in economically weaker countries and lower income people.

Posts in category Value Pickr

Amararaja Batteries Limited: Powering Ahead (13-08-2023)

Hi Gaurav,

I was referring to the pollution case as vendetta politics possibility…( The promoter is a politician and part of the opposition in the state of Andhra Pradesh) …

With respect to the fire incident, getting claim is one thing, there is also production loss, time loss in rebuilding the lost capacity, government enquiry into the safety aspect which may not renew factory licence and most of all doubts on management credibility as well at times, if this repeats like a loop every few years…

As some Institutions holding large positions also exiting the company and these circumstances prevailing I was weighing the pros and cons before taking a position in this company…

As @harsh.beria93 had attended the AGM my query was directed towards getting a first hand account of whether the management spoke about it, did a shareholder question the management on the same…

Amararaja Batteries Limited: Powering Ahead (13-08-2023)

On January 30,2023, a fire broke out at one of the manufacturing facilities of the Company at Chilloor, Andhra Pradesh which caused damage to the Company’s property, plant and equipment and inventories, There was no loss of lives. The Company recognized a loss of ~ 438 56 crores arising from such incidents during the quarter and year ended March 31, 2023 . The loss is based on an evaluation of physical condition of property, plant and equipment and inventories and technical inspection by equipment manufacturers or chartered engineers and an assessment of recovery / salvage value by the designated vendors.

The Company has a valid mega all risk insurance policy covering the fire accident and has lodged a claim with the Insurance Company for losses suffered on account of the property, plant and equipment, inventories and loss of profits. The Insurance Company has admitted the claim based on an interim survey carried out by the surveyor appointed by it and the extent of final loss admissible under the policy is being evaluated by the surveyor. The Company estimated and recognised an insurance claim receivable as at March 3 I, 2023 in respect of the claim in accordance with its acco

unting policy. The aforementioned losses and the corresponding credit arising from the insurance claim receivable were presented on a net basis under Exceptional items tor the quarter and year ended March 3 1,2023.

During the quarter ended June 30, 2023, the Company has received an adhoc payment of ~ 100 crores from the Insurance Company and the Company is confident of realizing the balance amount on final determination of the loss and completion of the related activities

^^ Insurance money will come in.

And what is the vendetta wrt politics here ? can u please explain if possible.

Caplin Point Laboratories (13-08-2023)

Technically looks sound

Amararaja Batteries Limited: Powering Ahead (13-08-2023)

Hi Harsh,

Thank you for sharing the notes on the AGM, answered many queries in my head… I was going to take a position in this company, could still ignore the pollution case as vendetta politics but the Jan 2023 fire completely gutting one of their manufacturing units in Andhra Pradesh stopped me from taking a position here…

Did they not talk/no one questioned them about that incident, how it impacts them, the responsibility factor, or is it something very minor…they claimed losses of 450 odd crores with the insurance co.

I was wondering if you could share any information on that, or how you read it …

Caplin Point Laboratories (13-08-2023)

-

The company repeatedly mentions to replicate the BOTTOM OF PYRAMID (BOP) STRATEGY which they have been using in LatM markets , in USA market. Not able to get clarity on it. What is it and How will it work?

-

What is a good expectation to build in for EBITDA MARGINS of Injectables to be sold in US?

Amararaja Batteries Limited: Powering Ahead (13-08-2023)

Just putting it out there as NMC vs LFP debates have been center of couple of posts here in this Amara raja thread. Did read this back in may to get what is the latest debate around.

My portfolio updates and investment journey (13-08-2023)

Hi Girish, thanks for your comments. Definitely pledge is red flag however we should put everything in context. If promoters are honest and they use the pledge to benefit the company (for loans or borrowing) then you have to think about it. Nevertheless, I shall never keep high allocation to companies which have pledge (high for me is anything 3% or above) as not everything is in promoters control especially market movements and resulting margin calls on pledge or subsequent selling by lenders for recovery.

Now my rationale on Syrma SGS (7% of allocation, 68% profit)

Background: My first buy was in September 2022 at 292 rs. My last transaction (part sell) was in July2023 at 496 rs. My average cost is 280.

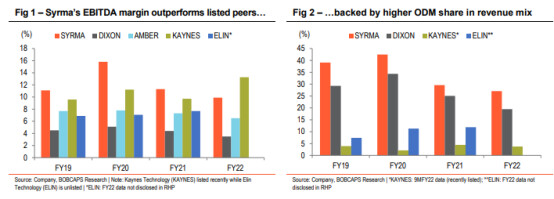

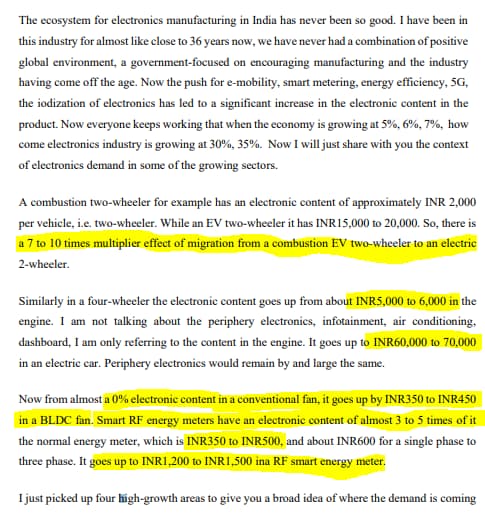

In one of the video Ishmohit (SOIC) mentioned that knowledge is cumulative and my buying in Syrma was based on cumulative learning – linked to Dixon Tech, which I bought in 2019. Dixon was making TV sets, Phones, LED lights and security cameras with leading market shares (in some cases up to 30%). For any company in India consumer business having market share of 5-10% itself is huge ask. First thing came to my mind was economies of scale with such market share. I also thought I can play consumer appliances and discretionary spend story through Dixon which was reasonably valued in 25-30PE range. So I entered Dixon for 15-20% compounding returns over next 4-5 years. In April 2020, Indian government announced the much popular PLI scheme. Suddenly my senses woken up, I did some rough calculations on the opportunity size just for mobiles. My numbers were whopping. I added Dixon aggressively. I said in my mind this company will have revenue of 1 lakh crore in next 10-15 years (4k crores in 2020). Also I thought this should trade at 50-60PE given the growth. Rest is history, everyone knows Dixon story. I sold Dixon fully in January 2023 after shocker results and weak guidance, the point was not just the results and guidance but the point was amalgamation of 100PE with it.

Now how is this linked with Dixon, I was closely following the sector given the opportunity size. With Dixon, Syrma was compared too much during its IPO. The key difference in both was EBITDA margins, Dixon was in broadly in 4-6% range while Syrma was 2x of that. Syrma’s high margin is due to its design capabilities. Its high share of ODM in overall revenue mix vs. Dixon mainly led to it.

Source: BOBCAPS, publicly available report – http://www.dsij.in/productattachment/BrokerRecommendation/SYRMA%20SGS8.12.2022.pdf

There are other areas where Syrma was better than Dixon but it traded at lower PE than Dixon. Further my confidence was boosted by the fact Mr Sumeet Nagar’s Malabar Fund invested in Syrma during IPO – https://www.youtube.com/watch?v=99T-Cta8gf8&t=1231s . My earlier successful investments like Affle, Indiamart, and Saregama were also overlapping with Malabar Fund. While in February 2023, Gautam Trivedi from Nepean Capital also talked about their investment in Syrma (he/his fund invested in Hindustan Foods long back so another alignment of thinking with good/great investors or fund managers. To stay convinced I continue to find reasons, to a certain extent it leads to confirmation bias also (but I don’t mind it). Disappointment in Dixon’s Q3 FY 2023 numbers led me to totally shift my Dixon holdings to Syrma.

Other factors which helped my rationale were, management seemed honest as they reduced IPO. Pre-IPO placement was at 290 vs. IPO price of 220. They mentioned that they wanted to reflect the market and wanted to be a long-term partners with stockholders and benefit together. When most promoters and early investors are trying to squeeze every penny from market, it was a good gesture. I found company has been guiding for very high growth (30-40%) from past several quarters and continue to do so. I have extracted below excerpt from Q4 FY 2023 concall of the company, which provides rationale for high growth:

Source: company concall transcript filing on BSE.

I note that company has been very acquisitive and they had provided good rationale for it. For their recent acquisition of medical devices company Johari Digital, they mention that getting approvals and developing products would have taken many years so they went ahead with acquisition.

Now I will end this with my final thought: whenever a industry has a tailwind we should look at the whole value chain (vendors, suppliers, distributors and customers) and as many players in it.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more , exit or partly sell the stock without any prior intimation.

WPIL Ltd – Global Water Pumps (13-08-2023)

Some notes from Q1FY24 Concall:

Reasons to Sell the Nuclear pump business:

Apart from what is already disclosed in the presentation;

(a) The industry environment is such that it will go through consolidation and a lot of M&A activity.

(b) Business needed significant capital expenditure to remain competitive

(c) Got good deal at EV/EBITDA 12x

(d) Helps increase cash reserves & strengthen the Balance sheet in current High Interest Rate environment

Note: Divestment will be completed by December this year, for now it will appear in the consolidated financials. This business makes up about 11% of top line.

Utilization of funds raised through sale: About Rs. 600Cr.

(a) Looking at inorganic opportunity in domestic or international market within Pumps

(b) Will wait till the sale goes through to decide how to utilise the funds

View: Management seems to have taken a prudent and rational decision in selling the nuclear business which will provide them with fire power to focus on growing core pumps business which has a large opportunity.

-

Management is conscious of the margins and the type of projects they want to take up to maintain healthy financials

-

Management says the challenges are on the execution side and not on Order book. Hence, focusing on project execution, orders are there to take up.

Business momentum:

- To continue

- H2 is stronger for domestic projects segment due to the on set of monsoon, about 60% higher than H1 during a year

- Australia is turning out to be a good growth area with the subsidiary being the only Oil & Gas pumps provider → Huge oder book development

On NSE listing:

- Participant requested the management to consider listing on NSE given their growing size, management responded saying “sure”, didn’t provide any concrete intention yet.

Defence products:

- New area of growth

- Co. has developed new products for the navy and is looking positive for good growth in the short-medium term. Will announce once things materialise.

Valuation:

-

One has to be conscious of the frequent upper/lower circuits due to low liquidity of stock with 70% held by the promoter.

-

Now considering 10-11% top & bottom line evaporating with the sale of Rutschi, and with the Domestic & International Products order book of Rs. 1100Cr to be executed over 1-2yrs and 2800Cr of Jal Jeevan order book to be executed over the next 3 years (from Q4 FY23 concall). It looks like this will more than compensate for this loss + inorganic acquisition is an optionality.

Time technoplast (12-08-2023)

Another good set of results, with sales growing by 14% and EPS by 27%. In the past, management used to overguide and underdeliver and this has changed significantly since Mr. Bharat Vageria has taken over as CEO. Not only are they being more measured in their capex spends, but they have been judiciously paying down debt while focusing more on value added capex. There is a good possibility that they end up delivering 20% ROCEs in next couple of years. Concall notes below.

FY24Q1

- Debt reduced by 32 cr. in Q1FY24

- Capex: 44 cr. (18 cr. towards established products + 26 cr. towards value-added products)

- Divestment discussions are at an advanced stage, talking with multiple customers to sell different parts of business geographically

- Expect 500 cr. of revenues in composite products in FY24

- US has declined by 20%, but haven’t seen that kind of pressure in other export markets

- Export breakup: 50% (South east Asia and Taiwan), 20% (USA), 30% (Middle East)

- MOX film: have capacities to do 150-160 cr. revenues. Don’t plan to add capacity

- Received PESO approval for manufacturing Carbon Fibre Reinforced Composite Cylinder (Type-III) for Medical Oxygen and Breathing air (first Indian company to get this)

- Will submit hydrogen cylinder to PESO for approval in 2024

Disclosure: Invested (position size here, no transactions in last-30 days)