Does it mean you need to pay tax on applicable tax slab on 40,125.42?

Posts in category Value Pickr

Indian Energy Exchange (IEX) (26-09-2024)

No update from management as of now. But intresting article is below one. You can get from Google search.

Staff Paper on Market Coupling

Prepared by Staff of

Central Electricity Regulatory Commission 3rd and 4th Floor, Chanderlok Building, 36, Janpath, New Delhi-110001 Website: www.cercind.gov.in

August 2023

Easy Trip Planners (Easemytrip) – An outlier in OTA (26-09-2024)

I think all are traders arranged by Nishant himself, as if there are no buyer for this offload then it’s very shameful for the company.

Earlier also they offloaded stake by saying that they want to start an NBFC to fund small companies…

Tata Motors – DVR (26-09-2024)

Yes, I too received similar mail with lot of details. 26AS will be available once tds is deposited.

Knowledge Marine – Positioned to Double Revenue with No CapEx (26-09-2024)

I am sharing few notes on Knowledge Marine, i feel it has good growth ahead, but as investors what we need is good price and patience.

Business

The company is engaged in the business of dredging and hiring marine craft for various essential services to the major and minor ports across the coastline of India and neighboring countries. Dredging currently contributes ~95% to the total business.

Dredging – Dredging is the process of excavating or removing sediment, debris, or other material from the bottom of bodies of water like rivers, lakes, harbors, or the ocean floor. This is typically done using specialized equipment such as dredgers, which may be floating vessels or land-based machines equipped with mechanisms like suction devices or buckets.

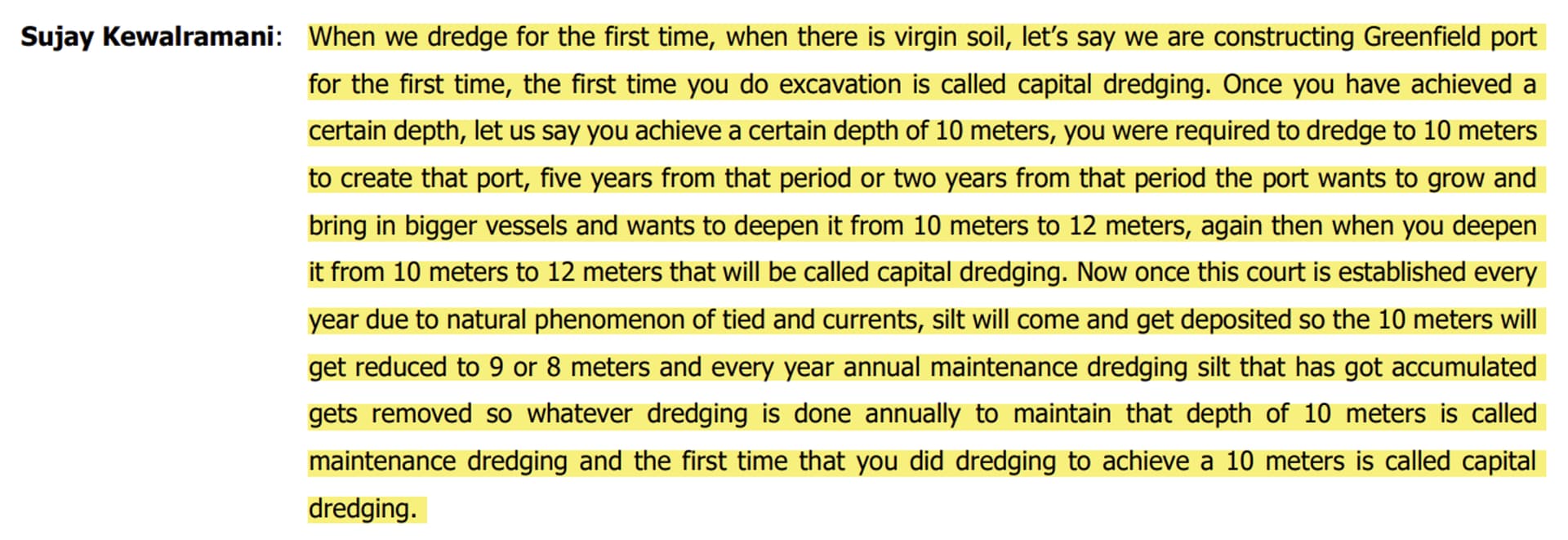

Maintenance dredging vs capital dredging

- Growth in the order book

End of Q4FY22 – ₹182 crore. H1FY23: ₹208 crore. FY23: ₹202 crore. H1FY24: ₹670 crore. H2FY24: ₹733 crore. Pipeline in ₹1,200 crore with ~40%-50% order win rate.

The company is increasing its qualification for orders as within 2 years it is now able to bid for orders worth ₹300 crore from being able to bid only for ₹100 crore orders.

- Increase in number of vessels

FY21: 4 vessels, FY22: 8 vessels. H1FY23: 10 vessels. H1FY25: 24 vessels. Aims to have 50 vessels within 10 years.

- Competition

“The job is not very easy, it requires a lot of skill. Also, you said the competition is not very high, the large players are the Government of India Dredging Corporation of India and there are players from Europe such as Van Oord, Boskalis, Dredging International, Jan de Nul; they choose to fix contracts which are easily above Rs. 100 Crores, Rs. 150 Crores so there is very minimalistic competition for the contract which are below ₹100 Crores.”

-

Competitive advantages

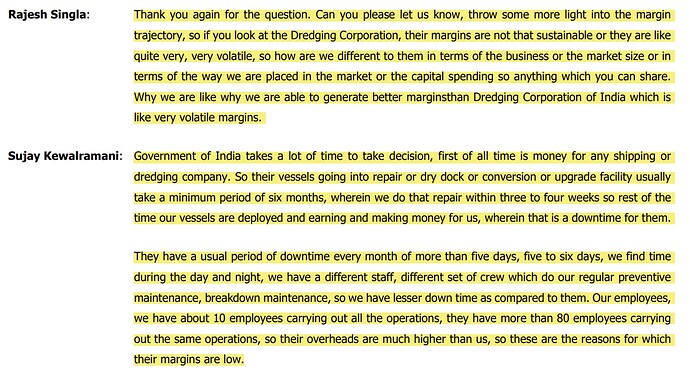

The reason the company is better than its closest competitor – Dredging Corporation of India

-

How a company manages to keep its capex low?

-

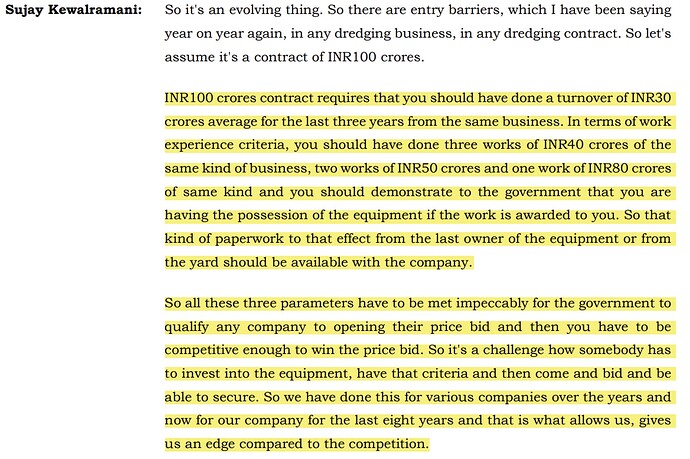

Entry barriers as per the management

-

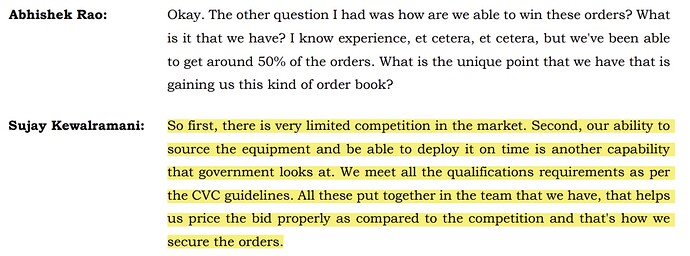

How the company manage to get 50% of its order?

-

Collection of data

-

Market size

-

Increase in debt, keeping cash to get better deals

-

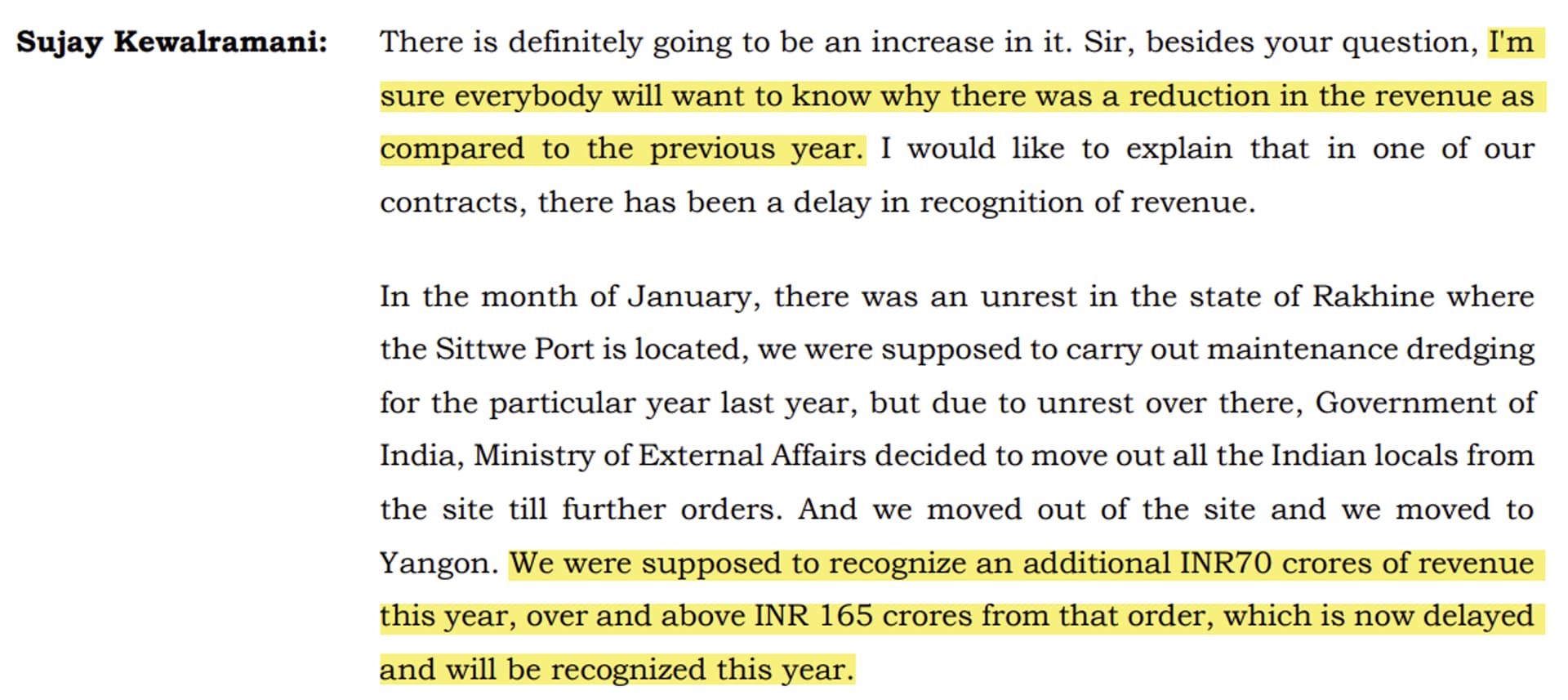

Reason for decline in revenue in FY24

-

Capital allocation

“We have chosen the joint venture route to avoid the capex that is usually required to start these ventures. We have tried to keep our capex low and we have tried to have higher margins, so what you are thinking and saying is correct.” -

Future Outlook

Will exhaust ₹300 crore of order book. Orderbook at the end of FY25 might be close to ~₹1,200 crore

Management guidance:Revenue reaching ₹275-₹300 crore orderbook. Operating profit margins to be within 30%-50%. PAT reaching ₹60 crores.

Currently has over ₹700 crore orderbook which can be executed within 2-3 years.

Risks

-

Equipment and execution: By the nature of the business, when the company receives the order, the revenue is known. The margins then completely depend on the company’s execution skills and selection of the correct equipment. These two factors can decide margins and customer satisfaction. Good execution is needed for repeat orders, new orders, and protecting & improving operating margins.

-

Management stake selling: The management has sold a significant stake which was bought by a mutual fund. Further stake selling and a decrease in management holding is a significant factor to watch out for.

-

Moderate scale of business: Though revenue has increased to Rs 201.5 crore in fiscal 2023 from Rs 61.2 crore in fiscal 2022, it continues to remain modest. Modest scale limits pricing power with suppliers and customers and limits the benefits related to economies of scale. The revenue is dependent on achieving a healthy order book and timely execution of orders.

-

Tender-based nature of business: The company operates in a tender-based industry, which has predefined criteria for track record and physical infrastructure. Business certainty depends on timely order execution, which in turn relies on various external factors such as customer clearances and any change at their end.

Few questions on first look

-

Debt – They have raised debt to increase cash on balance sheet. This cash they will be using to acquire ships from second market whenever they win the order. Having cash ready gives them a better terms on the deal.

-

Fixed assets – These are the vessels they acquire for executing their orders. Number of vessels have increased to almost 20 in FY24 as compared to 10 in FY23.

-

H2FY24 decline – They had to evacuate from Myanmar due to GOI’s orders. ₹70 crore of revenue got delayed, expected to come this year.

-

The 55% margin thing was one off. They are guiding for 30%-40% margins. They have secured a sand mining contract in Bahrain. To enter this market, they have reduced their margin for the first order. Next orders in the region will have 35% margins.

About Sagarmala

The Sagarmala Programme, a flagship initiative of the Ministry of Ports, Shipping and Waterways, represents an approach by the Government of India to transform the country’s maritime sector. With India’s extensive coastline, navigable waterways, and strategic maritime trade routes, Sagarmala aims to unlock the untapped potential of these resources for port-led development and coastal community upliftment. Approved by the Union Cabinet in March 2015, Sagarmala seeks to enhance the performance of the logistics sector by reducing logistics costs for both domestic and international trade.

Overall, currently there are 839 projects worth investment of ~Rs. 5.8 lakh Cr. for implementation under the Sagarmala Programme by 2035. These include projects being implemented through various funding arrangements including Equity, Internal Resources, Grant in Aid, PPP mode etc. Out of which, 262 projects worth ~Rs. 1.4 lakh Cr. have been completed and remaining projects are under various stages of implementation and development.

B C C Fuba India Ltd: PCB Manufacturing Nanocap (26-09-2024)

We have lot of EMS companies with huge SMT lines. SMT machines solder components on bare PCBs. So basically we have more EMS companies than bare PCB manufacturers. Recently Govt offered PLIs for laptop , tablet etc. These are pre-designed PCBs and factories already manufacturing PCBs would be much more efficient Vs new PCB manufacturer. PCB manufacturing has it own share of challenges hence it is not possible for new player to start manufacturing. PCB manufacturers want higher duty so that people buy from them, however due to less PCB manufacturing capacity they are not keeping pace with EMS demand. Most of bare PCBs are still getting imported form China. Once India PCB manufacturers have enough expertise and capacity then increasing duty makes sense until them they need to keep a balance. Please remember, bare PCBs are each gadget is different and requires different level of competence. As Govt pushes more and more value add benefits we would shift to PCB manufacturing slowly and we would see scale. Few good EMS companies has already started building capability and it would all be fine in medium term.

Shivalik Bimetal Controls Ltd (SBCL) (26-09-2024)

Shivalik FY24 AGM Notes 26 September 2024 10:30 AM at Solan

Last year was sales growth slow but business was not “unexciting”. There were many new products which are under developments

The company is focussing to make manufacturing process to meet the best in the global market. As per one client, the development of manufacturing process and quality control tools/machine used by Shivalik are superior and better then what the client has been using inhouse. Automation/Robotics usage has increased flexibility of manufacturing process (previously only one product standard could be provided to machine, now multiple dimensions can provide to manufacturing machine which can result different dimension product simultaneously from single machine. Further, the data is collected online from the final output which assist company to understand problem area. Further, the robotic machine used in manufacturing filter out all product which are not matching the final dimension without human intervention resulting reduction in rejection rate/ product recall due to defective quality.

Part of reason of slow down in FY24 could also be attributed to Geo-political development. Previously, the company was working European and US client’s China team to provide support to new development. However, most of the players have now decided to shift development of new products to other geographies in proximity to their area of operation. That resulted in new team getting involved in development and also resulted 9-12 months delayed in new project implementation.

The company is also looking at passing on management of business to new generation. Mr. Kabir and Mr. Anand inducted in Board of Directors are executive directors. Mr Anand would look at business development and marketing while Mr. Kabir would be responsible for research, production and development of manufacturing process. Mr. Sumer would also be actively involved in Finance and managing relationship with Investor community. Mr. Sandhu who has been involved with inception of the company and currently chairman is likely to move out of Board of director. Mr. Ghumman would continue to be board and provided guidance to the new team.

Research efforts: The company has created a team of specialist to guide research efforts. Currently, there are four members which is likely to expanded further. The company is also looking at filing a new patent application from past efforts of its research team. They are also evaluating forward integrating and increase value addition in existing products, specifically in shunts. While, that is likely to increase the turnover, due to higher value addition, growth in margin is expected to higher than revenue growth.

The company has implemented new line which is likely to increase automatic (robotic) quality checks of 1.5-2 million parts per month. This new line is expected to commence production from November 2024.

Innovative Clad: The JV has now turn around. During FY24, the company accumulative losses were adjusted and it is likely contributed positively for future growth of the business.

Metalor MOU: The company was in discussion with Metalor for JV to manufacture new products in silver current. However, the subsequent discussion among the JV partners resulting in differing viewpoints on technology support and market access. As per Management, proposed terms by the JV partner were not match with Shivalik Financial expectation. While, discussion is still underway, Shivalik is cautiously optimistic and carefully evaluating finalisation of JV terms.

Growth driver: US and European EV Automobile industry is stabilised and they are expecting increased order during FY25 and FY26. Although, the EV demand is likely to revive, the management feel, that it would be still lower than FY22 peak achieved by EV industry in developed market. Smart Meter, Domestic EV/Hybrid, Domestic ICE shunt supply, Increased demand form Domestic Data Centre and increased share of higher value-added products (particularly EV shunts) would be main drivers for growth in medium term. While the market dynamics can delay stated goal of Rs 1600 Cr turnover, they are putting all efforts to achieve the stated goal.

Niche Engineering along which state of art technology in electronic industry would be key industry where company intend to develop new products beside current market. That industry all ingredient for high growth and company is very well placed with required skill set to take full advantage of the opportunity, in view of management.

Disclosure: Shivalik Bimetal is among Top 3 holding for me. My view may be biased due to my investment. I am not suggesting any investment action. I am not SEBI registered advisor. I may increase/decrease/exit from my investment in the company without informing forum. There may be communication error from my side.

MSTC Ltd.: Growth through to E-Commerce (26-09-2024)

While I’m not a valuation expert, my rough estimates suggest that with a projected PAT of ₹160 crore for FY25 (₹40 crore in Q1), and applying multiples of 10-15 along with cash reserves of ₹1400 crore, the market capitalization would be in the range of ₹3000-₹3800 crore.

The current Mcap is 4800 cr with PE of 22. It might correct some more from these levels (not a expert!). Feedback welcome!

RBM Infra – a less discussed SME (26-09-2024)

@kdjolly firstly, I dont know who Sandeep Singh is.

Secondly, what you have stated is a motherhood statement without understanding the nuances of infrastructure and cosntruction contracting.

An infra company is one who owns the asset forever or owns it for a limited period time in a BOT (built own operate) project. They need to finance the project. Let us say the cost of the project is 100 (90 of hard costs and 10 of interest capitalized during construction). The infra company arranges 100 to finance (maybe 70 of debt from banks and 30 of own equity). If the economics of the project dont make sense the infra company defaults on the 70 of debt which is the NPA you are talking about.

RBM Infracon is a not an Infra company. It is an infrastructure construction company. The infra asset owner contracts out construction of the assets to people like RBM. So the loans are not on RBM’s books.

For example in the 2013-2018 period infra companies like Jaiprakash Associates, Lanco Infratech etc went belly up. The constructors like L&T etc are still around.

If you are trying to suggest ONGC, Adani, Nayara Energy and RIL who own the asset are going to go belly up and that will lead to orders given to RBM Infra getting cancelled then its different.

There are execution risks which i understand. Can such a small SME company execute such a large order backlog? Can they generate cash flow from operations? These are some of the valid concerns. Your concerns seem to random to me.

Moldtek Technologies (26-09-2024)

Is the outlook positive post US elections along with the rate cuts? If anyone attended AGM please share the management commentary on the same.