How to build a resilient portfolio to achieve sustainable growth:

Posts in category Value Pickr

Biocon – The ultimate biosimilars play! (23-09-2024)

I am not very ambitious on returns. My buy price (after accounting for splits/bonuses…) is about Rs. 17. Does 20X in 15 years count for a return?

Biocon tries too many things, it appears to be aggressive at times and very defensive at times.

Aggressive: developing new drugs (though with partnerships, licensing…), trying to be an innovator

Defensive: When they enter service space (with assured margins) that affects their product business

Too active: Buys a business from its customer, sells something else…

Pretty complex to analyse. Only concern is “outsized influence of the promoter, who is past the prime, on the business”

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (23-09-2024)

Will valuations mean revert, my expectation is, most probably it will not.

Will the stock generate returns for shareholders from here, probably yes.

I feel valuations will not mean revert because if we compare valuations of the top 4 private banks, HDFC and Kotak enjoyed high valuations as compared to ICICI and Axis. The reason for that is HDFC and Kotak were consistent in growth, profitability and NPAs, while ICICI and Axis had their own issues. Now, all 4 private banks are almost on par. Hence HDFC and Kotak will not enjoy the valuation premium going forward, so no mean reversion.

Having said that, if our economy continues to do well, all 4 banks will participate, and if they are able to grow their earnings, then the share price will follow the earnings growth.

Disc: Invested

Oriental Aromatics (Earlier: Camphor & Allied Products Ltd) (23-09-2024)

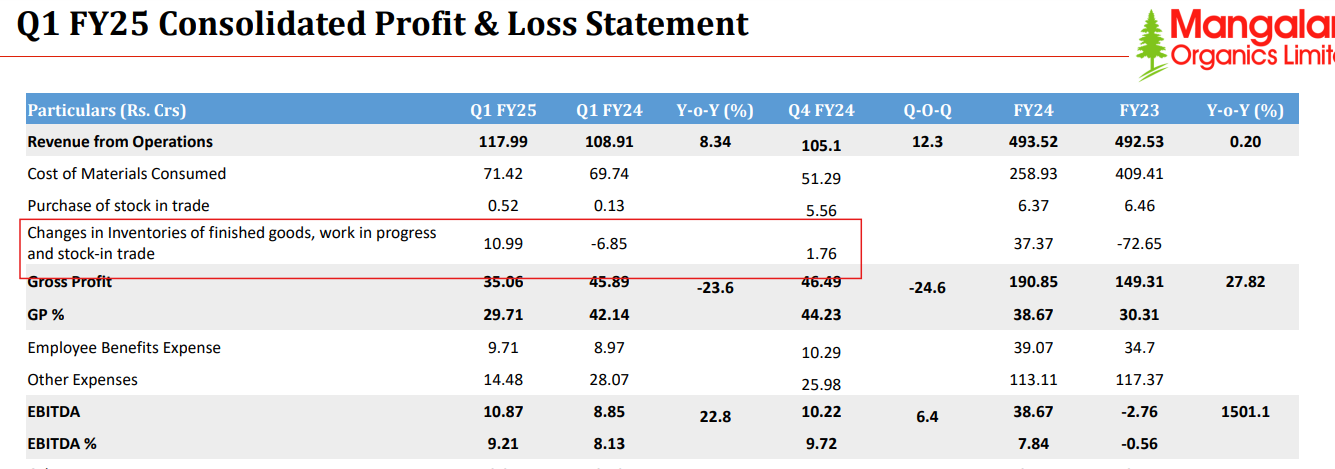

Mangalam Organics has become increasingly difficult to track as it doesn’t do con-call and is highly illiquid (made worse by SEBI ASM frameworks) as well. If i recall, it had done large capex few quarters ago. There may be lag between commodity price increase and company earning due to multiple factors e.g. low priced finished goods inventory still in the channel esp. for B2C players, existing price contracts for B2B sales wherein price hike may take few qtrs to come into effect, presence of high cost RM inventory hence subdued margins, loss of market share etc. Most of these reasons may be theoretical as lack of con-calls means these would be our best guesses. Some buying by promoters and impact of capex done in 2022, may indicate positive outlook for the company esp. if camphor prices remain firm. Q1FY25 results too indicate some increase in inventory so their liquidation at increased prices too can give EPS a leg up.

Indostar Capital Finance Limited (23-09-2024)

Indostar Capital recently last week sold its HFC business to EQT for 1750crs, this liquidity will help them focus on their core strengths of vehicle financing and small business loans. Also due to which the stock was in news and the trading activity picked up on back of huge volumes and the stock hit a 52 week high. The entire HFC and NBFC space is buzzing off late.

Fundamentally, during these 3 years management changes took place and legacy Corporate, vehicle finance and SME book was cleaned up. Funds were infused couple of times by the promoter Brookfield and other marquee investors took a pie of the shareholding.

Technically Indostar has been in correction mode since Aug 2021 and has formed a rounding bottom structure in form of a cup and it might create a low handle to the cup. If the pattern plays out the next technical target could be around 415 levels.

Disclosure : Invested as a trading bet.(Trades done in last week, this not a stock recommendation, anyone contemplating investing needs to do their own due diligence).

Tata Motors – DVR (23-09-2024)

According to this article, only Tata motors spokesperson, PWC, Citi and Axis capital, all funded by Tata motors, feel it is fair deal ![]()

The article says otherwise with these points…

-

The retail investors and mutual funds are set to get a raw deal in the proposed conversion of Tata Motors DVR (differential voting rights) to ordinary shares.

-

The public DVR holders and mutual funds will lose about ₹15,568 crore and ₹3,000 crore of economic value, while the promoters will gain 1.4 per cent economic share valued at about ₹5,000 crore, per the April 18 closing price.

-

Post conversion, the promoters holding in Tata Motors will increase to 42.62 per cent from 41.23 per cent, while that of public will slip to 57.38 per cent from 58.77 per cent.

-

Both type of shares have equal economic right and after accepting that DVRs have traded at sharp discount due to absence of proper market, the company has taken the market approach to ascertain higher weightage for ordinary shares, said Sivakumar R, a retail investor.

-

Globally, the shares with reduced or no voting rights trade at premium or about the same price to ordinary shares. For instance, the class C shares of Alphabet (Google) with no voting rights trades at a premium to ordinary shares.

Anyway it is not very intelligent to cry over spilt milk. This is just a lesson learnt that Tata group is no Saint either.

Rudra’s PF and Information attic (23-09-2024)

All these articles, and reports from Sadhan, MFIN, CBs and CRAs, are lagged. They are just extrapolating Q1 stress without any additional on ground data.

Also, lets not forget that Fusion is highly geographically concentrated in a few states which is of their own doing.

Bond Market Yields (23-09-2024)

Used India bonds (not to be mixed with bonds India) often. You make the payment directly to the India clearing corporation by RTGS and hence there is no safety concern (in the sense, there is no payment to India bonds).

India bonds gives a clear quote, deal sheet and once you approve, and make the payment, the bond will be in your Demat by End of day. (this is assuming that you did your KYC before).

The best part of the India bonds site is the portfolio view, cash flow and maturity view of all the bonds you have purchased through them (and they have a feature, wherein you can import purchases from others too). If you need any more info, please DM me.

PS – the safety of the bond itself is not subject to , where from you are purchasing from. I am NOT recommending anything but giving my experience

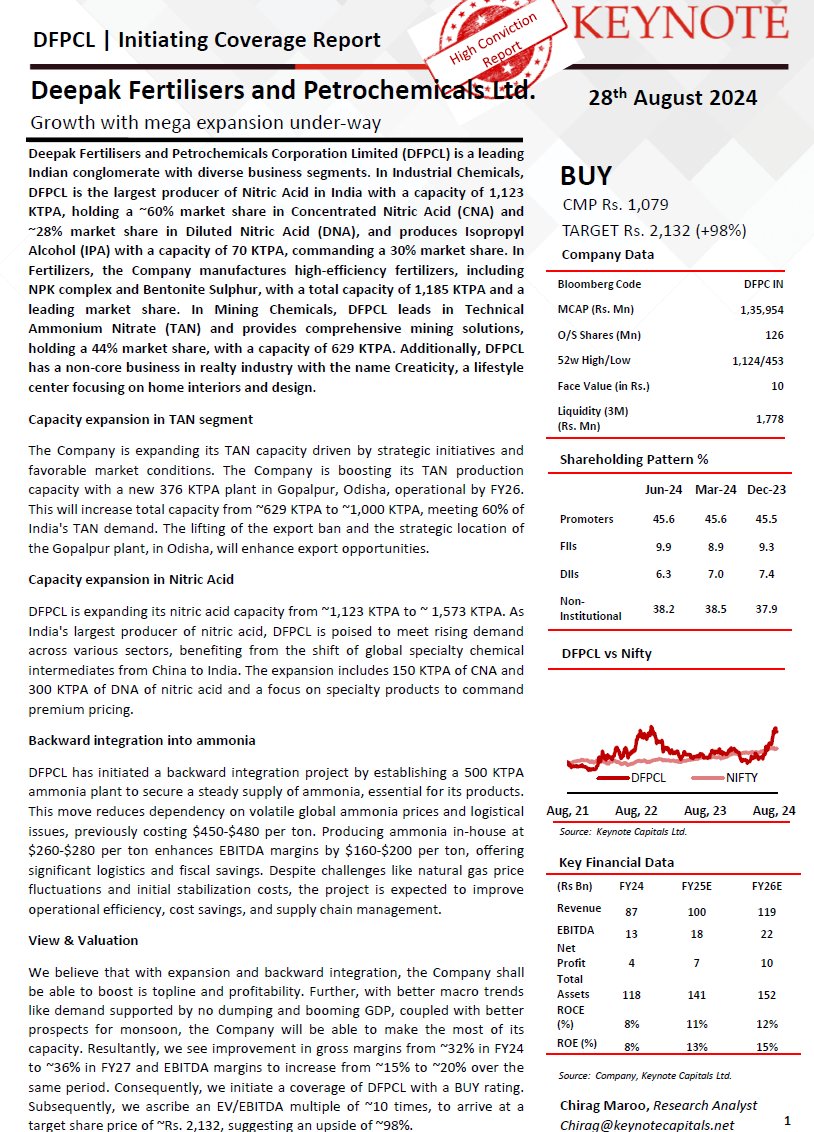

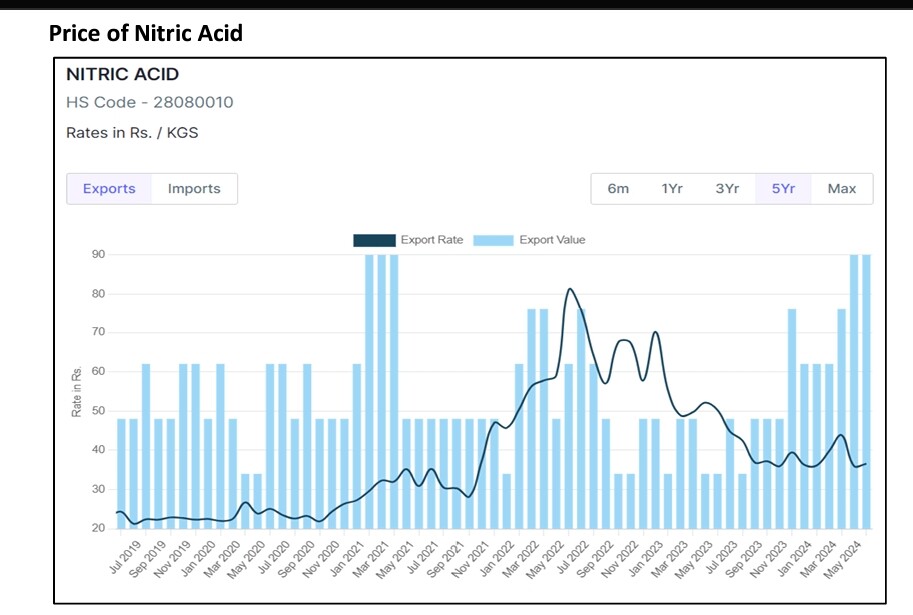

Deepak Fertilizers and Petrochemicals (23-09-2024)

Keynote has given Target of 2132 for Deepak Fertilizers, +98% Upside

Keynote_initiating_coverage_on_Deepak_Fertilisers_and_Petrochemicals.pdf (1.7 MB)

“The company is well-positioned to drive growth in both revenue and profitability. Additionally, it will capitalize on increased capacity utilization, supported by favorable macroeconomic conditions. Strong demand, bolstered by the absence of import dumping and a growing GDP, coupled with positive monsoon forecasts, will further enhance the company’s prospects.

The global ammonia and nitric acid market is currently facing significant changes due to several key factors. Strict environmental regulations and high compliance costs are leading to the closure of ammonia production facilities across Europe, reducing regional supply. At the same time, natural gas prices are rising because of higher domestic demand and LNG exports, which is driving up production costs for ammonia producers, especially in Europe.

As a result of these developments, global prices for both ammonia and nitric acid are expected to rise, benefiting producers in regions with lower raw material costs, such as India. However, industries that rely on these chemicals, such as fertilizer and explosives manufacturers, may need help with these increased costs.

disc- invested, not buy/sell reco

Oriental Aromatics (Earlier: Camphor & Allied Products Ltd) (23-09-2024)

Hi Saket, are you tracking mangalam organics? Camphor prices are on uptrend since this year and B2C is in effect since some time back but Q1FY25 nos are nothing to cheer about, why would this be? Any thoughts on this? thanks