Thank you for the elaborate writeup sharing your experience in the market. It would be helpful if you can share your

1.) Current style of investment (Microcap investment, Special situations, Growth style, value, Monopoly and largecap , Contrarian etc.).

2.) Goal (%CAGR or final corpus).

3) Sectors you are interested.

4.) Portfolio or stocks which you like.

Posts in category Value Pickr

Nikhil’s Investment Journey – Past and Current (10-09-2022)

Nikhil’s Investment Journey – Past and Current (10-09-2022)

Thank you for the elaborate writeup sharing your experience in the market. It would be helpful if you can share your

1.) Current style of investment (Microcap investment, Special situations, Growth style, value, Monopoly and largecap , Contrarian etc.).

2.) Goal (%CAGR or final corpus).

3) Sectors you are interested.

4.) Portfolio or stocks which you like.

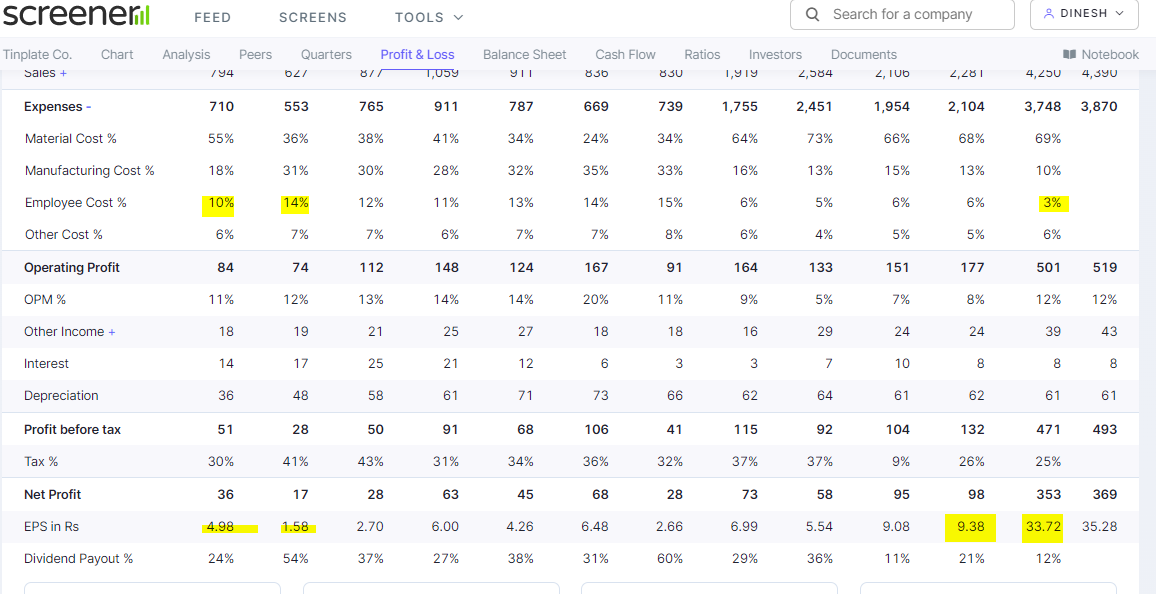

Tinplate – Blasting through volumes, cyclically (10-09-2022)

thank you everyone for input . i am also interested in buying this company .

thesis :-

1)its a TATA company

2)showing good growth in term of sales

3 )part of packaging industry specially in food segment which includes oil and canned food and non food like paint , sprays etc.

4 ) with growing consumerism chances of consumption of these items will increase so use of tinplate

5) there is almost none domestic competition , but there is risk of cheap Chinese competition if FSSAI give license to them

antithesis :-

although this company makes product focused on consumer but there is wide fluctuation in EPS , for which it behaves like a cyclical company. it may be because of rise in input cost , but it again arise a suspicion why its not able to pass the input cost to its customer.

if anyone of you have this answer i will be obliged and will make a decision to buy some part of company

Tinplate – Blasting through volumes, cyclically (10-09-2022)

thank you everyone for input . i am also interested in buying this company .

thesis :-

1)its a TATA company

2)showing good growth in term of sales

3 )part of packaging industry specially in food segment which includes oil and canned food and non food like paint , sprays etc.

4 ) with growing consumerism chances of consumption of these items will increase so use of tinplate

5) there is almost none domestic competition , but there is risk of cheap Chinese competition if FSSAI give license to them

antithesis :-

although this company makes product focused on consumer but there is wide fluctuation in EPS , for which it behaves like a cyclical company. it may be because of rise in input cost , but it again arise a suspicion why its not able to pass the input cost to its customer.

if anyone of you have this answer i will be obliged and will make a decision to buy some part of company

Laurus Labs – Can Business Transform to Next Level? (10-09-2022)

The overall borrowing as on 31st Mar 2022 was 1777 crores. The Cash Flow from Operating Activities in 2022 was 911 crores. So assuming that Laurus would be able to grow earnings at around 25% CAGR, it would take 1.5 years of earnings to repay complete borrowings provided it would not take any new debt. The thing with fast growing capex intensive companies is that you need funds to grow topline, and that fund would either be equity or debt (rarely it would be completely from internal accruals).

Cheers,

Krishna

Laurus Labs – Can Business Transform to Next Level? (10-09-2022)

The overall borrowing as on 31st Mar 2022 was 1777 crores. The Cash Flow from Operating Activities in 2022 was 911 crores. So assuming that Laurus would be able to grow earnings at around 25% CAGR, it would take 1.5 years of earnings to repay complete borrowings provided it would not take any new debt. The thing with fast growing capex intensive companies is that you need funds to grow topline, and that fund would either be equity or debt (rarely it would be completely from internal accruals).

Cheers,

Krishna

HDFC Asset Management Company (10-09-2022)

@Vinay_T_M -

The regulatory mandate dictates self-investments only for the Equity Mutual Funds (5.15% of total investments in this case i.e 5.9% of 87.3%). IMO rest may be used for M&A. Least, it would ensure a high Dividend Payout for the coming years.

You may refer Page-40 of the investor presentation for details [Link].

FYR:

HDFC Asset Management Company (10-09-2022)

@Vinay_T_M -

The regulatory mandate dictates self-investments only for the Equity Mutual Funds (5.15% of total investments in this case i.e 5.9% of 87.3%). IMO rest may be used for M&A. Least, it would ensure a high Dividend Payout for the coming years.

You may refer Page-40 of the investor presentation for details [Link].

FYR:

Great articles to read on the web (10-09-2022)

I just wanted to state that when Debashis Basu has written this article, he must have believed it to be true. I’m basing my presumption on his understanding & knowledge, nothing else.

And if you ask what I think of it independently, that I have already stated in my earlier post.

Mudit’s Portfolio (Passively Active) (10-09-2022)

Since I am from Insurance sector, one thing that I know is, all our Insurance companies whther they are LiC or private sector, they are actually not the insurance companies in th true s3nse of the word. They are actually savings banks. As the statistics goes, in case of LIC, if you check their total claims, out of that only 3% is death claims, while remaining 97% is Maturity claims, meaning, ppl are using these companies as savings banks for the investments and not for insurance. Once that is clear, then comes the financialization scheme in the picture, 10 crore Dmat accounts, ppl are investing heavily in mutual.funds, stocks, so they are less and less into savings and more and more into investments. So i see this like newspaper industry where sun is setting as far as savings aspect of life Insurance is considered. But Insurance aspect , i m not much enthusiastic as indian mentality is such that they want something in return if they invest any money. So pure term.insurance , where premium is anyway very less and it may not be a good profit making business model as it is, indians are not favourable. These are broad reasons for not investjng in life insurance companies.

For general insurance i am quite optimistic and had some exposure in ICICI lombard. I may think again about it…need to study it.