Interesting article about Ajay Piramal's heir apparent, Anand Piramal who is running Piramal's realty arm :

Posts in category Value Pickr

Realtime Alerts for BSE Corporate announcements (07-11-2015)

Hi Sunil,

I am not getting alerts from couple of weeks. I checked in SPAM folder also but didn't find the alerts. It is very helpful for to track BSE alerts and I was using it from quite sometime. Can you please tell me anything wrong.

Thanks

Chetan

Shalibhadra Finance – Steady Growth NBFC (07-11-2015)

Hi,

I am a newbie and usually visit ValuePickr for reading/learning purpose quite a number of times in a month.

I was completely convinced about this story( and quite impressed at the research work done), until I saw that Manav's account has been deactivated( and read the thread about his communication with the Admin) I would like to thank Admin for bringing this to notice. Really enjoy this forum.

Regards

kartik

Need for KYC to be enforced when Forum Abuse is detected (07-11-2015)

I am a member of an auto forum in which they have a good filtering mechanism. Every new thread is vetted by the Admin before it is made visible on the forum. Ofcourse it means the Admin has to read each new thread.

Rights for creating new thread can be given only after say 6 months to a new member.

Can we implement either/both here?

Automated Stock Analyzer (07-11-2015)

If it is not an excel error, I cannot help you. I neither invest in stocks nor do I understand valuation. Only know that valuation may not work all the time and heavily depends on inputs.

Realtime Alerts for BSE Corporate announcements (07-11-2015)

Works fine now. Many thanks

MPS Ltd (07-11-2015)

(1) we need to be fair to the management and respect the fact that to turnaround MPS from a messed up situation to 35 % + EBITDA margin situation must not have been an easy task and Mr. Arora did it in a very short time which is commendable. While doing this he must have done a trade off between less lucrative and more lucrative contracts because of which topline was bound to suffer initially which is ok. Company is able to sustain its topline at this margins signifies that company has credibility in the eyes of clients and has some relative advantages because of which clients are coming to it. That's the end of one side -- positive.

If we wanted only a steady dividend earner opportunity this side was ok but what we want is a real long term wealth creator. Now for that organic growth has to start somewhere. What I expected personally is the growth to start post stabilisation which didn't happen in FY15 and there is no sign yet. Possible gaps were filled by acquiring three small entities and if now gaps are filled FY16 should at least see a double digit organic growth which we will need to check as the year progresses.

(2) Extreme Pricing pressures that Mr. Arora has talked about remain a puzzle for me frankly. So far amongst peers only SPS gives volume as well as value figures and over last many years both growths are almost similar so at least SPS is not facing pricing pressure. Even if we consider the fact that it's almost an offshoot of a big publisher then also in the reported official statements pricing variation could not be that drastic and ultimately market forces come into play. Newgen's volume figures we were able to derive in past AR which was discontinued recently and from that also pricing pressures was not that evident. Infact if such pricing pressures was there then it actually means for such a healthy value growth they recorded tremendous volume growth which seems unlikely. However, small industry players feedback suggests a definite pricing pressure from clients. So is it that from a messed up situation in which MPS was acquired when it was on verge of loosing contracts, new management had to resort to significant discounts -- if that's the thing then post stabilisation at least such pricing pressures should subside -- or is it that new management is playing a strategy to regain its top position by compromising on pricing because of the advantages Dehradun facility provides ??

(3) regarding currency risks, major threat is philippines and until both the currencies move inline there seems to be not much threat to Indian counterparts. However we need to keep a watch of that.

(4) When MPS was acquired it was at no. 3 or 4 position from which it seems to have slipped to 6 or 7......the way efficiently and in a very quick time super turnaround was made, topline growth seems to be not that easy......its high time now that organic growth needs to start and FY16 and FY17 are crucial for that. So far company's strategy has been good and even numbers that we see seems to reflect that but for this story to remain relevant over many years to turn out to be a great wealth creator that we all are searching for, organic growth has to start now that's what I believe.

Rgds.

Discl. - Invested in MPS over last ~one year. Forms ~23 % of my portfolio. No transactions done in last 30 days.

Need for KYC to be enforced when Forum Abuse is detected (07-11-2015)

IF I may be allowed to extend the suggestion by @reacher.

Yes ranking of idea is a good idea and should be available to each and every member.

Members can revise their ranking based on their gut feeling, available information, risk that are discussed on the thread.

Amol

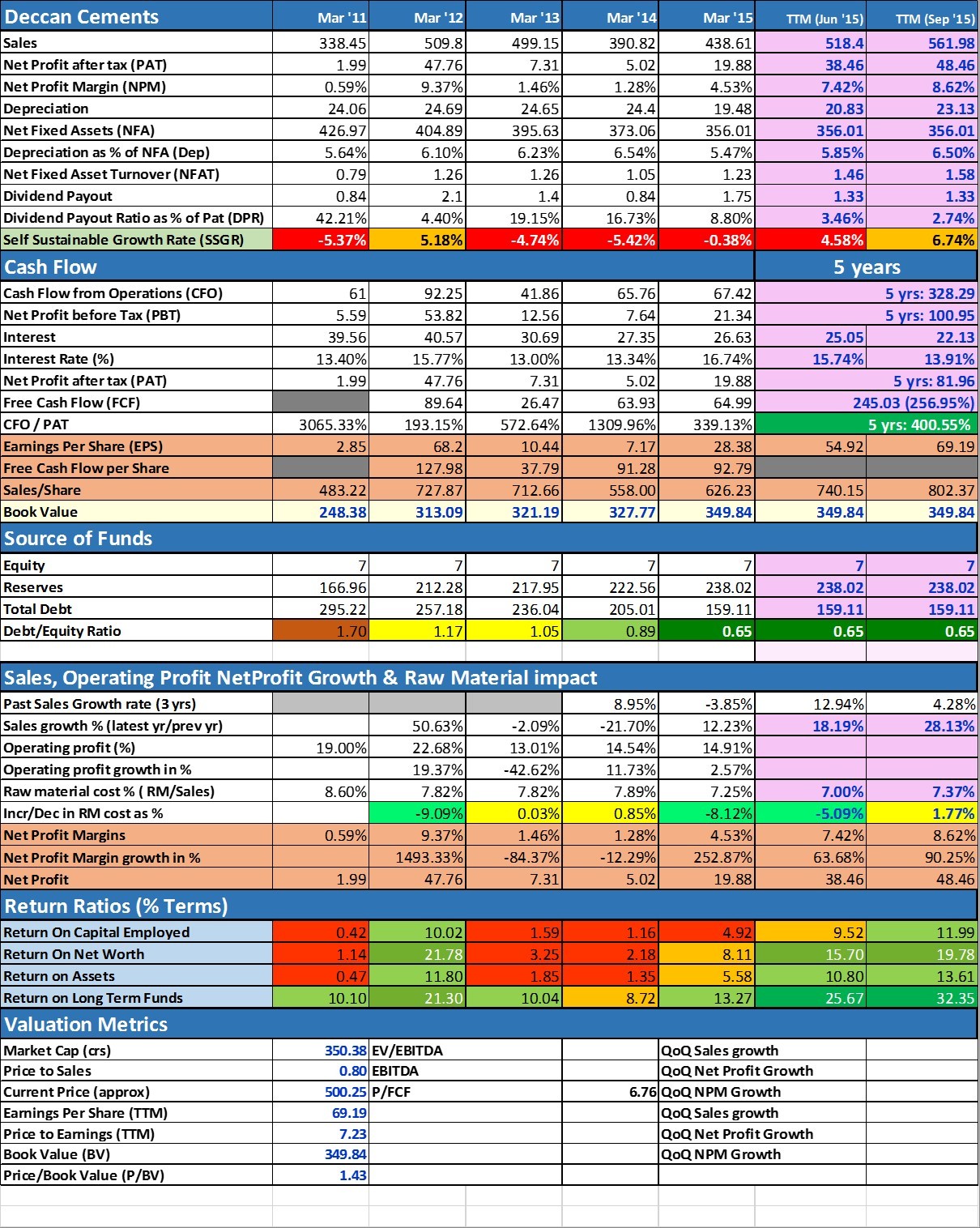

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (07-11-2015)

Seasonally this is the weakest quarter for cement companies due to rains & slow construction activity. If company can deliver such strong performance in this quarter with EPS of 22 then there is high probability of doing 25-30 EPS per quarter in the coming two quarters.

Looks very nice bet with almost negligible downside given current circumstances.

Disc. - Invested