3 ratios to pick winning stocks in the manufacturing space

Posts in category Value Pickr

Hitesh portfolio (08-08-2022)

Good evening Hitesh sir,

My question is regarding your techno-funda approach to investing.

- I wanted to know if all your picks in your pf have both momentum on charts and fundas always going for them?

- Do you keep a trailing SL, if not how do you deal with exits?

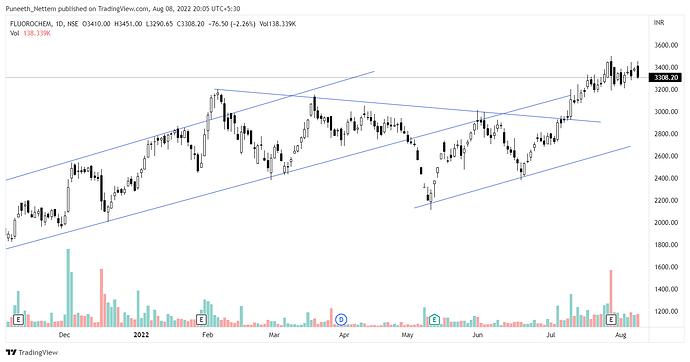

For example in Gfluoro, I pulled out my position at 2800 or so. How do you sense that it would pick up strength again?

Had made a similar mistake in FCL which corrected after I sold but regained and then some, leading me to miss out on heavy gains. Is there a systematic approach to this?

Thank you so much sir.

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (08-08-2022)

As far as I can see it , they do not do it every quarter .They do it twice a year or so …

Atleast thats whats available in screener .

Simple Investing (08-08-2022)

I was checking my thoughts and glad to see above realization right at the bottom of recent crash. It proves to me yet again that my instincts of fear, panic and urge to act and/or think/write becomes most active when the bottom is near…something I have observed over the last 2-3 significant crashes I have seen so far…

Going ahead, I think I need to trust my instincts more than any other noise around…

Recovery in IT has been swift, although most are still long way down their previous highs…however, incremental capital allocated has been rewarded decently over last few months…that is yet…

IT now forms around 7.5% of my portfolio. If I consider it as a single stock, then it would be my 5th largest holding. I think I have reached a decent allocation level now in IT. However, any new crash/wave what experts keep talking about would be welcome to increase allocation at opportune time - unless I see fundamentals deteriorating…

Apart from IT, another part of portfolio I was building but stopped midway was QSR - I had consolidated it to 3 holdings from 5 and it has least allocation as a basket - 3%. I think I am fine with this going ahead. No more action needed on QSR unless I see fundamentals deteriorating in any individual pick.

Lastly, the Consumer durables piece is what’s been hurting the medium term performance the most - This is 5% of my portfolio and I am making losses in overall basket ever since I started building it since 2020 crash. I see this as a gap in my portfolio to be eventually filled. In hindsight, I might have rushed to build allocation way early anticipating pent up demand buying when things open up (not because I wanted to play the trade but thought I might not get them at lower prices later). However, I completely missed the possible Inflation piece, but who would have anticipated that back in 2020 or early 2021…

As I see now, Inflation hurt Consumer Durables the most as they are not able to manage the huge surge in costs as well as say an FMCG or any other consumer facing business…In hindsight, few years from now, this maybe one of best times to buy such businesses…however with 5% allocation I seem appetite full at the moment and also not able to identify clear leaders in segments I like to expand allocation…Sometimes, I think it would have been better to chose more Discretionary names rather than durables - but as far as my history goes, I get such thoughts near bottom…so refraining from acting much here…

Overall recovery in portfolio has been decent. It is now 2.5% below its all time high.

Sensex is down around 4.7% and BSE Midcap Index down by 8.8% from its all time high, so I have nothing to complain here…

Although, I am aware that my stocks are always the first to recover and then I have to play a long waiting/consolidating game…but thats fine…its something I am well aware of so would wait for the Indexes to catch up…unless any top holdings give a positive surprise in performance…

Disc: Above thoughts only for academic purposes. I can be wrong in all my assessments. Not eligible for any advice or recommendations.

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (08-08-2022)

@Investor1234 yes, this does look strange. Usually they are very proactive with setting up the investor call.

Ranvir’s Portfolio (08-08-2022)

Disc: Sold JB Chemicals, Eris Lifesciences, Granules India and Aarti Drugs.

Reason : the draft policy of GoI on mandating doctors to prescribe medicines by generic names and not brand names. Although the policy is yet to be finalised, it still remains a significant source of risk.

Continue to retain Kopran Ltd due very cheap valuations and NGL Finechem as its in Animal Pharma space. Also continue to hold Divis because of its cost leadership in APIs and Syngene for its potential to convert some of its development stage molecules into commercial stage.

Bought the following -

Rushil Decor ( company looks like turning around )

KIMS, Narayan Hrudayalya ( I like the economics of Hospital business )

Greenpanel ltd

Balkrishna Industries

Axis Bank ( added to existing position )

Monte Carlo Fashions ( added to existing position )

Regards,

Ranvir Dehal

Bull therapy 101-thread for technical analysis with the fundamentals (08-08-2022)

Updates based on a couple more results

Devyani

Price is trading around previous peak post listing. A close above 200 with volumes on the weekly should take this higher. The results were quite strong with 100% topline growth YoY and bottomline from a loss of 29 Cr to 74 Cr. 70 new stores added during the quarter taking the total to 1000+ stores. KFC ADS at all time high, above pre-pandemic levels at 1.27 Cr. Also nice is the 30% SSSG in Pizza Hut. These small format delivery focused stores are firing really well. P/E dropped from 114 to 85 levels post results. The runway here is long and hopefully they can continue to execute like they have done with Varun Beverages

Manyavar

The breakout on the weekly last week is showing signs of continuation this week. 105% topline growth and a strong 123% bottomline growth with strong EBITDA margins of 51%. Store expansion as well is on track as they have expanded from 1.1 million sft to 1.28 million sft in the last few months. Here again the strong performance drops the P/E from 102 to 86 levels despite the big runup pre-results. The TAM here is huge

and unlike tech startups talking of TAM, here its actually meaningful in the hands of a business model with strong moats and a capable management. How they scale Mohey, Manthan and Twamev will tell us if their success with Manyavar is replicable.

Domestic consumption, especially discretionary consumption continues to remains strong across businesses here from VBL, Metro to Devyani and Manyavar. IDFC First’s retail loan book growth also points to the same. The wage hikes across IT are entering the economy through these discretionary spends and will very likely continue to remain strong across the festive season till end of year at least I think. So far signs are pointing to the same (1 lakh scorpio-n bookings in 30 mins for eg.). Margins should improve as well going forward with easing inflation. Let’s see.

Disc: Have positions in Devyani around 155 and Manyavar around 1100.

Borosil Limited (08-08-2022)

Great results from Borosil

25% increase in sales for Scientificware and 77% increase in sales for consumerware on YoY basis. 143% jump is PBT YoY mainly due to exceptional losses booked last year and exceptional gains booked this year (insurance claims paid). Removing exceptional items, PBT is up 25% YoY which is decent in current inflationary environment.

Selan Oil Exploration (08-08-2022)

Q1 FY22-23 Results are out - Brief Snapshot on quarterly financials

- Q-O-Q op revenue growth of 29% ; Y-O-Y op revenue growth(in respective Q1’s) by 84%

- Q-O-Q expense de-growth of -9.65% but Y-O-Y increase(in respective Q1’s) by 47.73%

- Current Quarter EPS 5.97 ; Last Quarter EPS 1.99

- In Q1 FY22-23, Cash profit of Rs.13.67 Crs

Overall Excellent set of numbers by Selan Oil

Disc:- Invested recently post excellent analysis by Pawan Kaul